Tax-deferred investments can be one of the most effective tools for building long-term wealth. They allow your money to grow without being taxed each year on dividends, interest, or capital gains inside the account. That tax treatment can make a meaningful difference over time, especially for people focused on retirement, long-term investing, and reducing their current tax burden while staying disciplined about future goals.

What Are Tax-Deferred Investments?

Tax-deferred investments are investment accounts or financial products that let you postpone taxes on earnings until you withdraw the money later. Instead of paying taxes annually on growth inside the account, you generally pay taxes when distributions begin, often in retirement.

This structure can be valuable because taxes don’t reduce your gains along the way. When earnings remain invested year after year, your money has more room to compound. That’s why tax deferral is often associated with retirement planning and long-term wealth building.

Common examples of tax-deferred accounts include traditional 401(k) plans, traditional IRAs, 403(b) plans, 457 plans, and some annuities. Each has its own rules, but the basic idea is similar: taxes are delayed rather than paid immediately on eligible contributions or investment growth.

How Tax-Deferred Investing Works

The main principle behind tax-deferred investing is timing. You may contribute money now, invest it in assets such as mutual funds, ETFs, bonds, or other investments, and allow the earnings to grow without current taxation inside the account. Taxes are usually due only when you take withdrawals.

In many cases, contributions may also reduce your taxable income in the year you make them. For example, contributions to certain employer-sponsored retirement plans or a traditional IRA may be deductible or made on a pre-tax basis, depending on eligibility and income rules. That creates a double advantage for some investors: potential tax savings today and tax-deferred growth over time.

This doesn’t mean taxes disappear. It means they’re postponed. When you eventually withdraw funds, those distributions are often taxed as ordinary income rather than at lower long-term capital gains rates. That’s an important distinction because the future tax cost still matters.

Why Tax Deferral Can Help You Grow Wealth Faster

The biggest benefit of tax-deferred investments is the power of compounding without yearly tax drag. When taxes aren’t taken out along the way, a larger amount stays invested. Over many years, that difference can become substantial.

For example, if two people earn the same investment return but one pays annual taxes on growth while the other defers taxes, the tax-deferred account may build a larger balance over time. That advantage becomes even more meaningful over decades of consistent contributions and reinvested gains.

This is one reason retirement accounts are so important in personal finance. They don’t just encourage saving. They create a structure that can help long-term investors keep more money working for them during the accumulation years.

Another benefit is behavioral. Because these accounts are designed for long-term goals, they can help people stay invested instead of reacting to short-term market movements. In that sense, tax-deferred investing can support both financial discipline and tax efficiency.

Common Types of Tax-Deferred Investments

401(k) Plans and Workplace Retirement Accounts

A 401(k) is one of the most widely used tax-deferred vehicles for employees. Contributions are often made directly through payroll deductions, which makes saving automatic. In many workplaces, employers also offer a matching contribution, which can significantly boost long-term account growth.

Other workplace plans such as 403(b) and 457 accounts work in similar ways for eligible workers. The money grows on a tax-deferred basis, and taxes are generally paid when distributions are taken later.

These accounts are especially powerful because they combine convenience, long-term investing, and potential tax benefits in a single structure.

Traditional IRA

A traditional IRA is another common form of tax-deferred investment account. Depending on your income and whether you’re covered by a workplace retirement plan, contributions may be tax-deductible. Even when the deduction is limited, investment growth inside the account is still tax-deferred.

This makes the traditional IRA a useful option for people who want additional retirement savings beyond an employer plan or who don’t have access to one at work.

Tax-Deferred Annuities

A tax-deferred annuity is an insurance product that allows earnings to grow tax-deferred until withdrawal. These products can appeal to investors who want tax deferral outside standard retirement accounts, though fees, contract terms, surrender charges, and payout rules require careful review. Annuities can play a role in retirement planning, but they’re more complex than a standard brokerage or retirement account. They shouldn’t be chosen based only on the tax feature.

Key Benefits of Tax-Deferred Investments

One of the biggest benefits is the ability to reduce current taxes in some cases. If your contributions lower current taxable income, you may keep more of your paycheck today while also investing for the future.

Another major advantage is long-term compound growth. Because taxes aren’t deducted from annual gains inside the account, earnings can build on prior earnings more efficiently.

There’s also a planning benefit. Many people expect to be in a lower tax bracket in retirement than during peak earning years. If that happens, tax deferral may become even more valuable because the tax is paid later at a potentially lower rate. These accounts can also support consistency. Automatic contributions through payroll or scheduled transfers make it easier to invest regularly, which is often more important than trying to time the market.

Potential Downsides to Understand

Even though tax-deferred investments offer real advantages, they aren’t perfect for every situation. One issue is that taxes still have to be paid eventually. If your future tax rate ends up being higher than expected, the benefit may be smaller than you hoped.

Another downside is withdrawal rules. Many tax-deferred retirement accounts impose penalties or restrictions for early withdrawals before a certain age unless an exception applies. That means these accounts are best suited for long-term goals, not short-term cash needs.

Some investors also forget that withdrawals from traditional tax-deferred accounts are often taxed as ordinary income. That can be less favorable than long-term capital gains treatment available in a taxable brokerage account for certain investments.

Liquidity matters too. Money placed in tax-deferred accounts may be harder to access without tax consequences. That’s why it’s usually wise to balance retirement investing with emergency savings and broader financial planning.

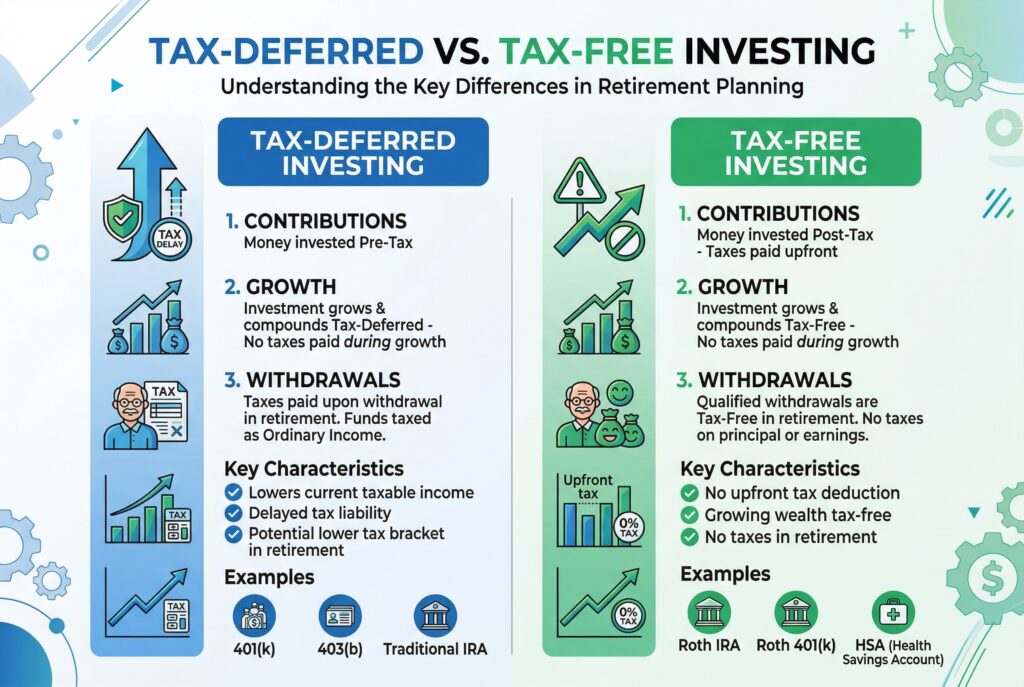

Tax-Deferred vs. Tax-Free Investing

A common misunderstanding is thinking tax-deferred and tax-free mean the same thing. They don’t. With tax-deferred investing, you postpone taxes until later. With tax-free investing, eligible withdrawals may come out without federal income tax if the account rules are met. Roth accounts are the most common example of that distinction.

This difference matters because the best option depends on your current income, expected future tax bracket, and retirement strategy. Some people benefit from a mix of both tax-deferred and tax-free accounts to create more flexibility later.

Smart Ways to Use Tax-Deferred Investments

The most effective approach is usually to treat tax-deferred investments as part of a broader plan, not as a standalone solution. Start by understanding whether you have access to a workplace retirement plan and whether employer matching is available. If there’s a match, contributing enough to receive the full match is often one of the strongest first steps you can take.

It’s also wise to review fees, investment options, and account flexibility. Tax deferral is valuable, but it shouldn’t blind you to poor fund choices or high-cost products. Diversification matters as well. A tax-deferred account still needs a sound investment strategy based on your time horizon, risk tolerance, and retirement goals. The account type helps with taxes, but investment selection still drives results.

As your income changes, your tax strategy may need to change too. In some years, prioritizing pre-tax retirement contributions may make the most sense. In others, a mix of account types may offer better long-term flexibility.

Conclusion

Tax-deferred investments can be a powerful way to build wealth more efficiently over time. By delaying taxes on investment growth, they allow more of your money to stay invested and compound for future goals. Accounts such as 401(k)s, traditional IRAs, and certain annuities can all play a role in helping investors save for retirement and improve long-term tax efficiency.

The biggest benefits come from understanding how these accounts work, using them consistently, and fitting them into a larger financial plan. When used wisely, tax-deferred investing can help you reduce current tax pressure, support disciplined long-term saving, and create a stronger path toward financial security.