")

If you’ve opened your card statement and suddenly seen a number called what is interest saving balance, you aren’t alone. A lot of cardholders, especially Chase users, see this line and immediately wonder whether they should pay that amount, the full statement balance, or just the minimum. The confusion gets even bigger with interest saving balance Chase statements, because installment features like My Chase Plan change how your bill is displayed. The good news is that this number usually exists to help you avoid extra credit card interest on new purchases without forcing you to pay off an entire eligible installment balance all at once.

What is an Interest Saving Balance?

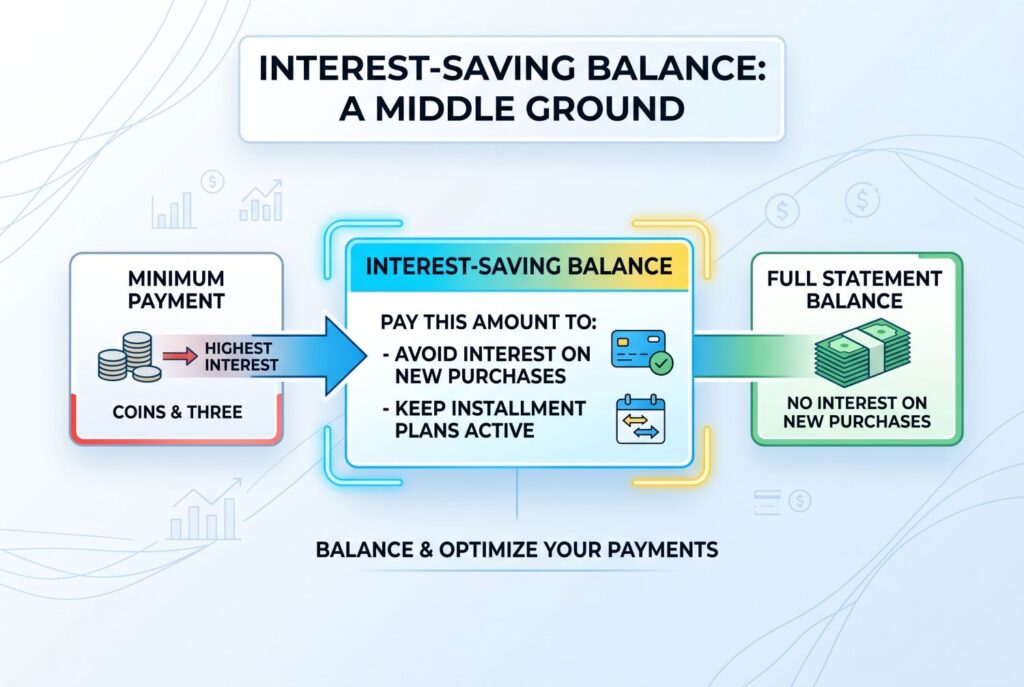

The short answer is simple: an interest saving balance is the amount you need to pay to avoid interest charges on new purchases while still keeping certain installment-plan balances active. In practical terms, it acts like a middle ground between paying only the minimum payment and paying the full statement balance.

This usually becomes relevant when a flexible payment feature is active on the card, such as a Chase installment plan. Instead of forcing you to pay the entire statement balance to avoid new purchase interest, the statement may show an interest saving balance that reflects your regular monthly charges plus the required installment payment amount. That way, you can avoid interest charges on current purchases without wiping out the full amount sitting inside the plan.

This is exactly why the term feels unfamiliar. It’s not a standard line that every cardholder sees all the time. It tends to appear in a more specific context, which is why so many users search for it only after they notice it on a statement and panic.

The “Big Three” Explained: Statement Balance vs. Minimum Payment vs. Interest Saving Balance

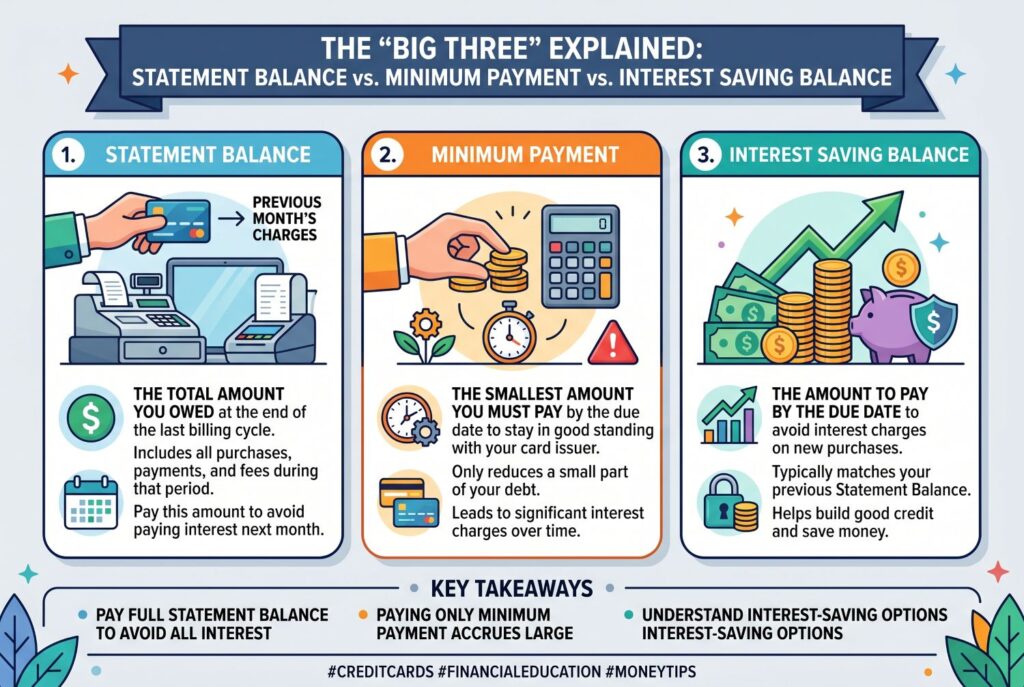

Most confusion comes from mixing up three different numbers on the same bill. Once you separate them, the statement becomes much easier to understand.

The Statement Balance

The statement balance is the total amount you owed at the end of the billing cycle. It includes purchases, fees, carried balances, and any other eligible statement activity. In a traditional credit card setup without installment features, paying the full statement balance is usually the standard way to avoid interest on new purchases.

The Minimum Payment

The minimum payment is the smallest amount you’re required to pay to keep the account in good standing and avoid a late-payment problem. But paying only the minimum payment usually means interest continues to accrue on the unpaid balance. So while it protects you from delinquency, it doesn’t protect you from ongoing credit card interest.

The Interest Saving Balance

The interest saving balance sits in between. It’s the number designed to help you avoid interest charges on new purchases while still preserving an active installment arrangement. In other words, it can let you avoid interest without forcing full payoff of the entire plan-related balance immediately. That’s what makes it so useful, and also what makes it confusing at first glance.

The Chase Example: How “My Chase Plan” Changes Your Bill

This is where Chase examples become especially helpful. A lot of search demand around this term comes from Chase customers using My Chase Plan or a similar feature. When you move a large eligible purchase into a structured plan, the bill no longer behaves like a standard all-or-nothing revolving balance. Instead, the statement may separate the installment portion from the everyday purchase portion in a way that affects what you need to pay to avoid interest.

Let’s say your statement balance is $2,000. Inside that amount, $1,500 is part of a Chase plan, and the rest reflects regular purchases and other non-plan activity. In that case, the interest saving balance chase amount may be lower than the full statement balance because it includes the amount needed to cover new purchases and the required monthly installment plan charge, not the full remaining installment principal.

That’s why this line exists in the first place. It tells you how much to pay if your goal is to avoid interest charges on fresh spending while still following the approved installment structure.

Scenario: Should You Pay the Interest Saving Balance or the Full Balance?

This depends on what kind of debt sits on your statement. If you’re using an active installment feature with favorable terms, paying the interest saving balance is often the smarter strategy. It lets you avoid interest charges on new purchases without paying off the entire planned balance earlier than necessary. In that scenario, paying the full balance may not actually be the most efficient move, because it could push extra money toward a balance that was already structured for more manageable repayment.

On the other hand, if you aren’t using a plan and your card is simply carrying normal revolving debt, the statement balance may still be the stronger target if your goal is to eliminate debt quickly and minimize interest long term. So the real question isn’t just “Should I pay more?” It’s “What kind of balance am I paying?” Once you know whether an installment feature is involved, the right choice becomes much clearer.

How is the Interest Saving Balance Calculated?

At a simplified level, you can think of the formula like this:

Interest Saving Balance = Statement Balance – Remaining plan-related balance not required this month + Required monthly plan amount

That isn’t always how issuers display it internally, but it helps explain the logic. The bank is basically isolating the amount you need to pay now to avoid new purchase interest, while excluding the portion of the installment balance that isn’t due yet.

Another simpler way to think about it is:

Current statement activity outside the plan

- this month’s required plan payment = interest saving balance

The exact number is generated by the issuer’s billing system, which is why the statement line itself matters more than trying to recreate it perfectly from memory. But conceptually, that’s what’s happening.

Conclusion

The golden rule is this: if your statement shows an interest saving balance and you’re using a Chase-style installment feature, that number is usually there to help you avoid interest charges on new purchases without unnecessarily paying off the full structured balance. That’s why understanding what interest saving balance matters so much. It isn’t just another random number on the bill. It’s a payment target with a very specific purpose.

If your bank or app allows it, setting autopay at the right level can make this much easier. And if you’re ever unsure, compare the statement balance, minimum payment, and interest saving balance side by side before paying. Once you understand those three numbers, your statement stops looking like a trap and starts looking like a tool.

Related Articles

Money Market vs Savings: Compare Yields with Our Money Market Calculator