What is a good APR for a credit card? A good APR is usually anything below 20%, while an excellent APR is often below 15%. That matters because credit card rates remain high, and carrying a balance can become expensive fast. Federal Reserve data showed the average APR on credit card accounts assessed interest was 21.52% as of February 2026, so shoppers should treat anything meaningfully below that level as stronger than average.

What Is a Good Credit Card APR Based on Your Credit Score?

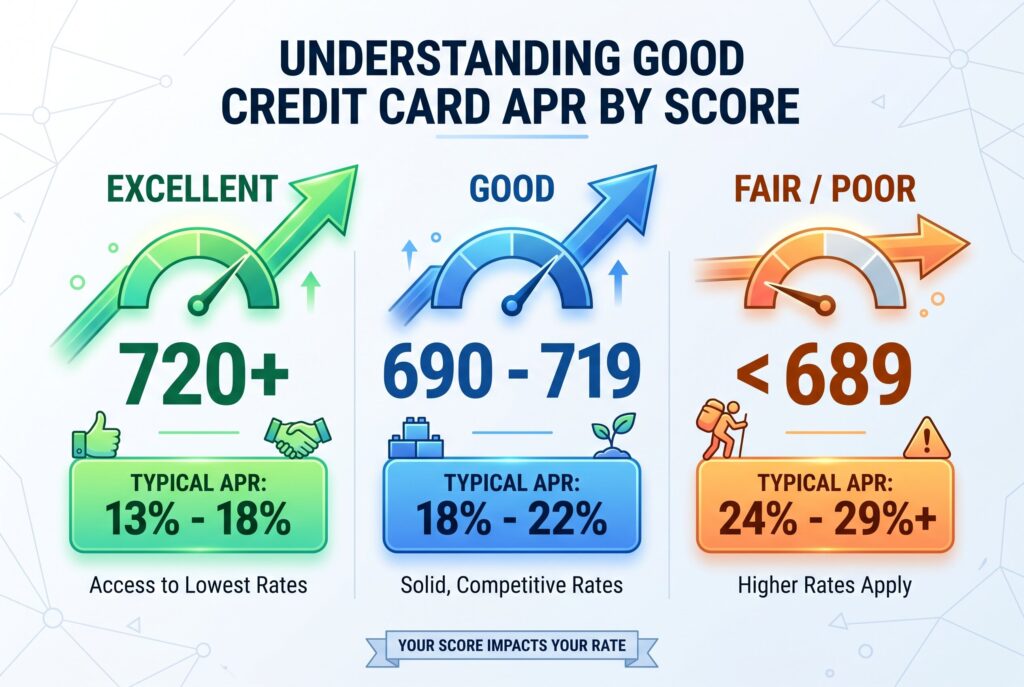

What is a good credit card APR depends heavily on your credit profile. Excellent credit usually gives you access to the lowest advertised ranges, while fair or poor credit often leads to higher rates.

For excellent credit, usually 720 or higher, a strong APR may fall around 13% to 18%. For good credit, around 690 to 719, a good range may be closer to 18% to 22%. For fair or poor credit, below 689, APRs may land around 24% to 29% or higher. So, what is a good credit card APR for one person may not be realistic for another. The better your credit score, the more negotiating power you have. If your APR is far above the national average and your payment history is strong, it may be time to look for better options.

Why Is It Important To Find a Credit Card With a Low APR?

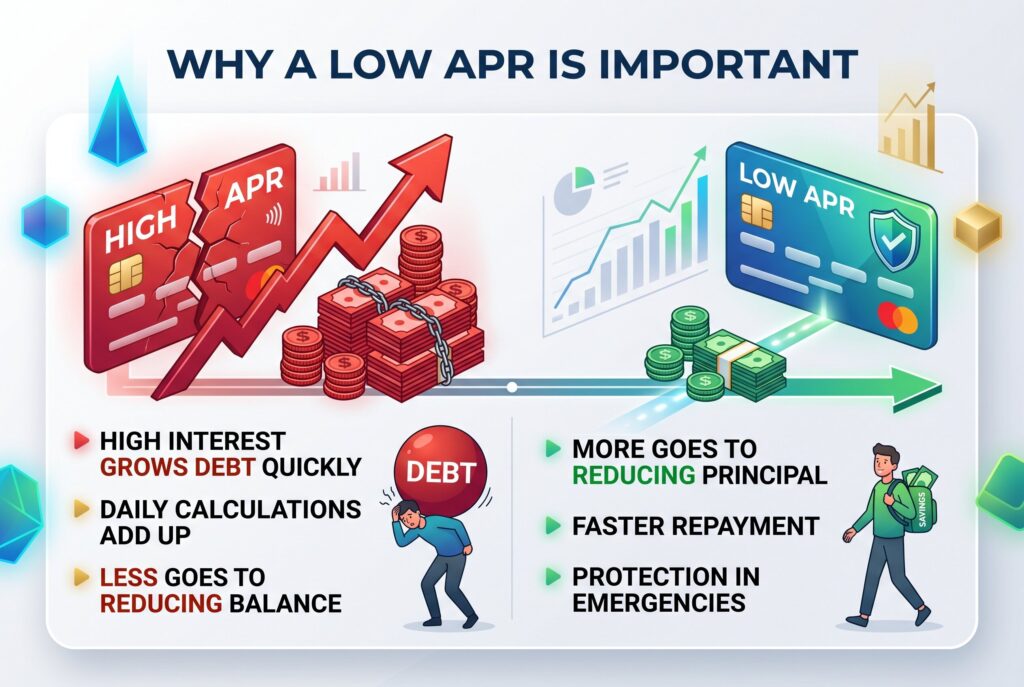

Why is it important to find a credit card with a low APR? Because credit card interest can grow quickly when you carry a balance. Most cards calculate interest daily, so debt can become harder to pay off if you only make minimum payments.

A high APR means more of your payment goes toward interest instead of reducing the balance. That can stretch repayment for years. If you borrow $3,000 at a high rate and only pay the minimum, you may end up paying far more than the original purchase amount. This is why a low APR isn’t just a nice feature. It’s protection. It gives you more room if an emergency forces you to carry a balance temporarily. Still, it isn’t a reason to carry debt casually.

The True Cost of Your APR

A credit card APR looks like a small percentage, but the real cost depends on your balance and repayment speed. A 19% APR and a 29% APR may not feel very different at first. Over time, the gap can become hundreds or even thousands of dollars. The easiest way to understand your APR is to compare payoff scenarios. Look at your current balance, monthly payment, and card rate. Then test what happens if you pay $50, $100, or $200 more per month. The faster you reduce the principal, the less power the APR has over your budget.

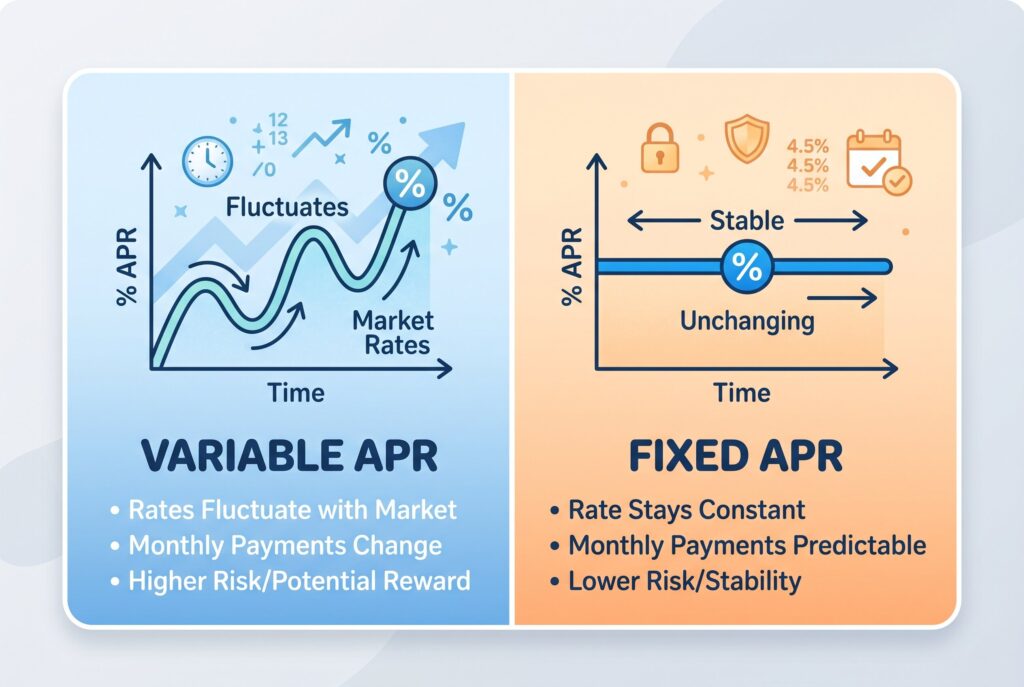

Variable vs. Fixed APRs: What To Expect

Most modern credit cards use variable APRs. That means your rate can move when benchmark rates change. Even if you receive a good APR today, it may rise later if market rates increase. Variable APRs are often tied to the prime rate, plus a margin set by the issuer. If the prime rate moves, your credit card APR can move too. That’s why you should read the pricing terms before applying. A card with a low starting APR isn’t always permanently low.

These days, this matters because credit card interest rates remain elevated by historical standards. The Federal Reserve’s G.19 data tracks credit card rates, including accounts assessed interest, which helps show what many borrowers actually pay when they revolve balances.

The 0% Intro APR Exception And How To Use It

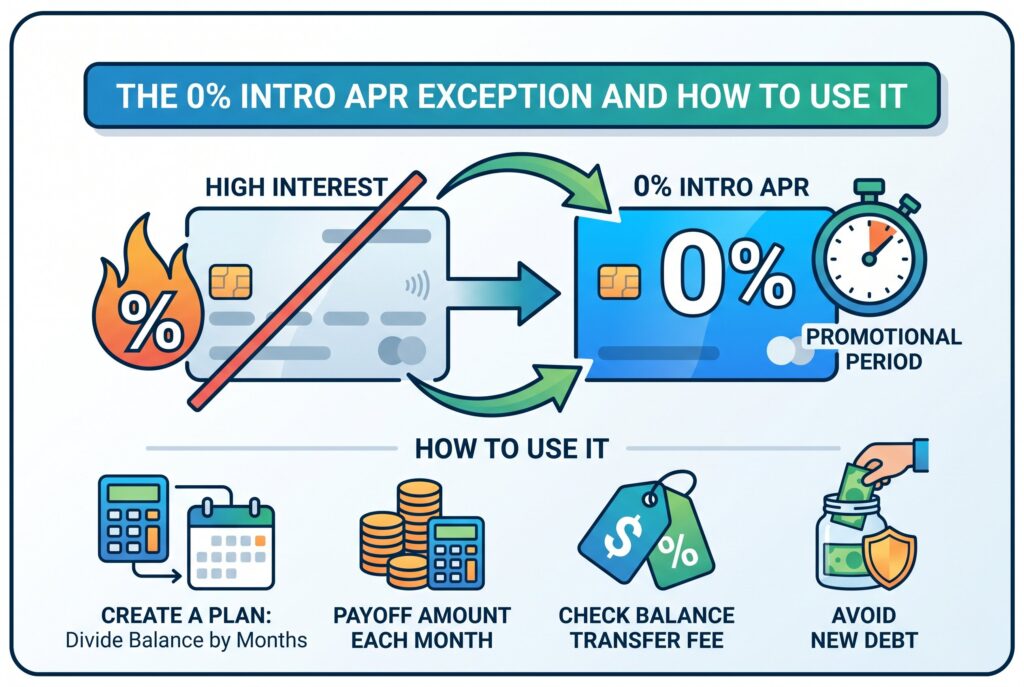

A 0% intro APR can be useful if you’re trying to pay down existing credit card debt. Balance transfer cards often offer 0% APR for a promotional period, commonly 12 to 18 months. During that window, more of your payment can go toward principal instead of interest.

This strategy only works if you have a clear payoff plan. You should divide the transferred balance by the number of promotional months and pay at least that amount each month. Also check the balance transfer fee, because many cards charge a percentage of the amount moved. Don’t use a 0% APR offer as permission to spend more. Use it as a temporary tool to escape high interest debt.

3 Ways To Lower Your Current Credit Card APR

Ask Your Issuer For A Lower APR

First, call your issuer and ask for a lower APR. This works best if you have a strong payment history, such as consistently paying on time and maintaining your account in good standing. It also helps if you can point to better offers from competing cards, as issuers may be willing to adjust your rate to keep you as a customer. They might not always agree, but in many cases, simply asking can lead to a reduced rate or at least a temporary promotional APR.

Improve Your Credit Utilization

Second, improve your credit utilization. This means lowering the percentage of your available credit that you’re using. Paying down existing balances is the most direct way to do this. Over time, lower utilization can improve your credit score, which in turn may qualify you for better credit card offers with lower APR ranges. Even small, consistent reductions in balance can make a difference when reported to credit bureaus.

Consider Debt Consolidation

Third, consider debt consolidation. This involves combining multiple credit card balances into a single loan, often a personal loan with a fixed and potentially lower APR. The main advantage is predictability, since fixed payments make it easier to budget and plan repayment. However, this strategy works best if you avoid adding new debt after consolidating. Without disciplined spending, it’s possible to end up with both the loan and new credit card balances, which can worsen your financial situation.

Conclusion

What’s a good APR for a credit card is a smart question, but the better goal is avoiding interest altogether. A good APR can reduce damage when you carry a balance, but paying in full every month turns your APR into a number that doesn’t matter. A good APR is generally below 20%, and an excellent APR is below 15%. Still, the ultimate financial hack is treating your credit card like a debit card. Use it for convenience, rewards, and protection, then pay the statement balance in full before interest starts.