Accrued revenue and deferred revenue are easy to confuse because both deal with timing. The mistake happens when businesses treat cash flow and recognized revenue as the same thing. They aren’t. These days, this matters even more for SaaS companies, agencies, contractors, and service businesses that bill before or after work is completed. Recording revenue at the wrong time can distort taxes, profit, investor reports, and cash planning.

The Core Difference: Cash Timing vs. Service Delivery

| Concept | Cash Timing | Service Delivery | Accounting Treatment |

|---|---|---|---|

| Deferred Revenue | Cash received first | Service delivered later | Liability |

| Accrued Revenue | Service delivered first | Cash received later | Asset |

Deferred revenue means the customer pays before the business earns the money. Accrued revenue means the business earns revenue before collecting cash. The difference comes down to which happens first: payment or performance.

What Is Deferred Revenue? Unearned Revenue Explained

What is deferred revenue? Deferred revenue is money received before a company has delivered the promised product or service. The deferred revenue meaning is simple: cash has arrived, but the revenue hasn’t been earned yet. Unearned revenue is another name for deferred revenue. For example, if a customer pays $12,000 for a one-year subscription on January 1, the company can’t record all $12,000 as revenue immediately. It earns $1,000 each month as the service is delivered.

Is Deferred Revenue A Liability?

Is deferred revenue a liability? Yes. The company owes the customer a future product, service, membership, or access period. Until that promise is fulfilled, the money represents an obligation. Is unearned revenue a liability? Yes, for the same reason. The business has received cash, but it still owes performance. It isn’t an asset from a revenue standpoint because the company may need to refund the customer if it fails to deliver.

Is It A Current Or Long-Term Liability?

Is deferred revenue a current liability? Usually, yes, if the company expects to deliver the service within 12 months. A one-year software plan, prepaid maintenance plan, or annual membership normally appears as a current liability. If the obligation extends beyond 12 months, the long-term portion may be classified as a long-term liability. For example, a three-year prepaid contract may be split between current and long-term deferred revenue.

Revenue Recognition Simulator

A revenue recognition simulator helps visualize how upfront payments become earned revenue over time. Suppose a customer pays $24,000 upfront for a 12-month SaaS contract. The company receives cash immediately, but it recognizes only $2,000 per month. After month one, $2,000 becomes revenue and $22,000 remains deferred revenue. After month six, $12,000 has been earned and $12,000 remains a liability. This prevents the business from overspending cash that still belongs to future service obligations.

What Is Accrued Revenue?

Accrued revenue is revenue a business has earned but hasn’t collected yet. The work is complete, the service has been delivered, or the performance obligation has been satisfied, but the invoice or payment comes later. For example, an agency runs a quarterly advertising campaign and meets the agreed KPI before billing the client at quarter-end. The agency has earned revenue even though cash hasn’t arrived yet. Under accrual accounting, that amount should be recorded as accrued revenue.

Is Accrued Revenue An Asset Or Liability?

Accrued revenue is an asset because the business has a right to receive cash in the future. It is often connected to accounts receivable, but the timing can differ depending on whether an invoice has already been issued. Don’t confuse accrued revenue with accrued liabilities. Accrued liabilities are expenses a business has incurred but hasn’t paid yet, such as wages owed or utilities used. Accrued revenue is money coming in. Accrued liabilities are money owed out.

Real-World Business Examples

A B2B SaaS company sells a one-year software plan for $36,000 upfront. It records cash and deferred revenue on day one, then recognizes $3,000 per month. If the customer cancels in month six and qualifies for a refund, the company must adjust the remaining deferred revenue and refund liability. This is why subscription businesses need clean revenue schedules.

Now consider a marketing agency that gets paid only after hitting quarterly performance goals. It completes the campaign in March and earns $18,000, but the client pays in April. The agency records accrued revenue in March because the revenue was earned before cash was received. Both examples show the same lesson: revenue recognition follows performance, not just payment timing.

How To Record Journal Entries Step By Step

For deferred revenue, the first entry happens when cash is received.

| Account | Debit | Credit |

|---|---|---|

| Cash | $12,000 | |

| Deferred Revenue | $12,000 |

Then, as the business earns revenue monthly:

| Account | Debit | Credit |

|---|---|---|

| Deferred Revenue | $1,000 | |

| Revenue | $1,000 |

For accrued revenue, the first entry happens when the business earns revenue before cash arrives.

| Account | Debit | Credit |

|---|---|---|

| Accrued Revenue | $5,000 | |

| Revenue | $5,000 |

When the customer pays:

| Account | Debit | Credit |

|---|---|---|

| Cash | $5,000 | |

| Accrued Revenue | $5,000 |

These entries keep the balance sheet and income statement aligned with the actual timing of service delivery.

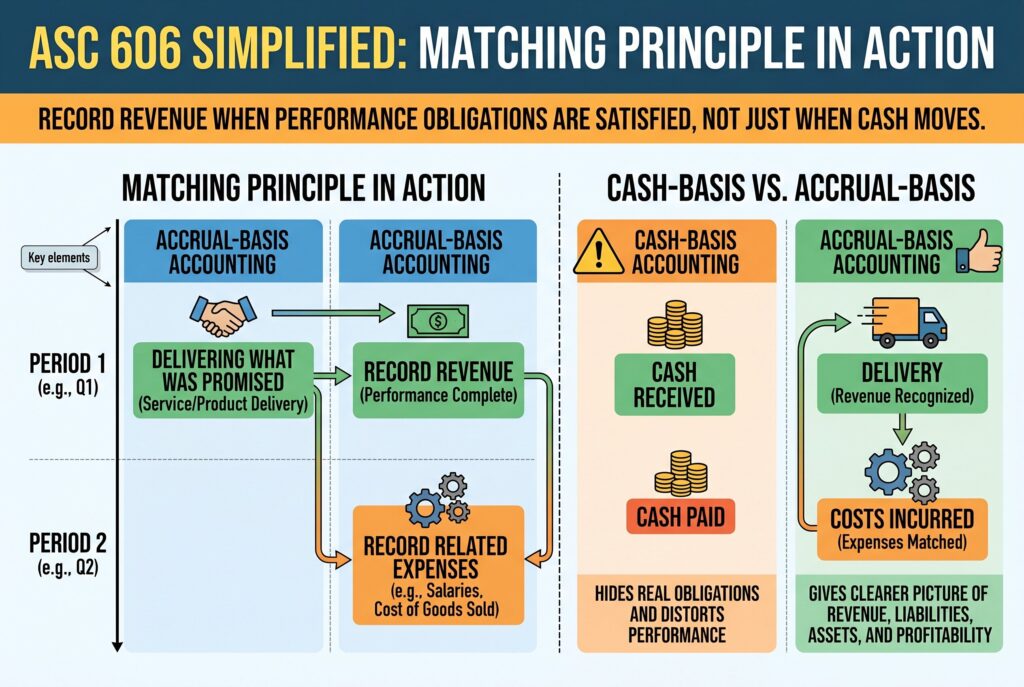

ASC 606 Simplified: Matching Principle In Action

ASC 606 focuses on recognizing revenue when performance obligations are satisfied. In plain English, a business should record revenue when it delivers what it promised, not simply when cash moves. This connects to the matching principle, which says revenue and related expenses should be recorded in the correct period. Cash-basis accounting may feel simpler, but it can hide real obligations and distort performance. Accrual-basis accounting gives a clearer picture of revenue, liabilities, assets, and profitability.

Conclusion

Accrued revenue and deferred revenue are opposites. Deferred revenue means cash comes first and service comes later. Accrued revenue means service comes first and cash comes later. Small businesses, SaaS companies, agencies, and service providers should move beyond simple cash tracking if they want accurate financial reports. Accrual-basis accounting gives a more reliable view of revenue, obligations, cash flow, and future performance, especially when preparing for funding, audits, or growth.