Deferred revenue is money received by a company before it has delivered the promised goods or services. It is also called unearned revenue because the business has been paid, but the work isn’t finished yet.

A simple example is a gym membership paid for the whole year in January. The gym receives the cash upfront, but it earns that revenue month by month as it provides access to the facility. The deferred revenue meaning is all about timing: cash came first, revenue comes later. This concept is common in SaaS subscriptions, retainers, prepaid maintenance plans, insurance, memberships, events, and long-term service contracts.

Why Is Deferred Revenue A Liability? And Not An Asset

Is deferred revenue a liability? Yes. Deferred revenue is recorded as a liability because the business still owes something to the customer. Until the product or service is delivered, the company has an obligation.

Think of it this way: if the business closed tomorrow and couldn’t deliver the service, it might need to refund the customer. That’s why the cash received is not treated as earned income right away. Is unearned revenue a liability? Yes, for the same reason. Unearned revenue means the company has collected payment but hasn’t fulfilled its obligation. It sits on the balance sheet as a liability until revenue recognition happens.

Is deferred revenue a current liability? Often, yes. If the company expects to deliver the goods or services within 12 months, it is usually classified as a current liability. If delivery extends beyond a year, part of it may be long-term.

12-Month Revenue Recognition Simulator

A 12-month revenue recognition simulator helps show how upfront cash turns into monthly revenue. Imagine a customer pays $12,000 on January 1 for a one-year software subscription. The business receives $12,000 in cash immediately, but it earns only $1,000 per month.

In January, $1,000 became recognized revenue and $11,000 remained deferred revenue. In February, another $1,000 becomes revenue and $10,000 remains deferred. By December, the full $12,000 had been earned. This kind of schedule is useful because it prevents businesses from overspending money that has not been earned yet. It also helps finance teams forecast cash flow more accurately.

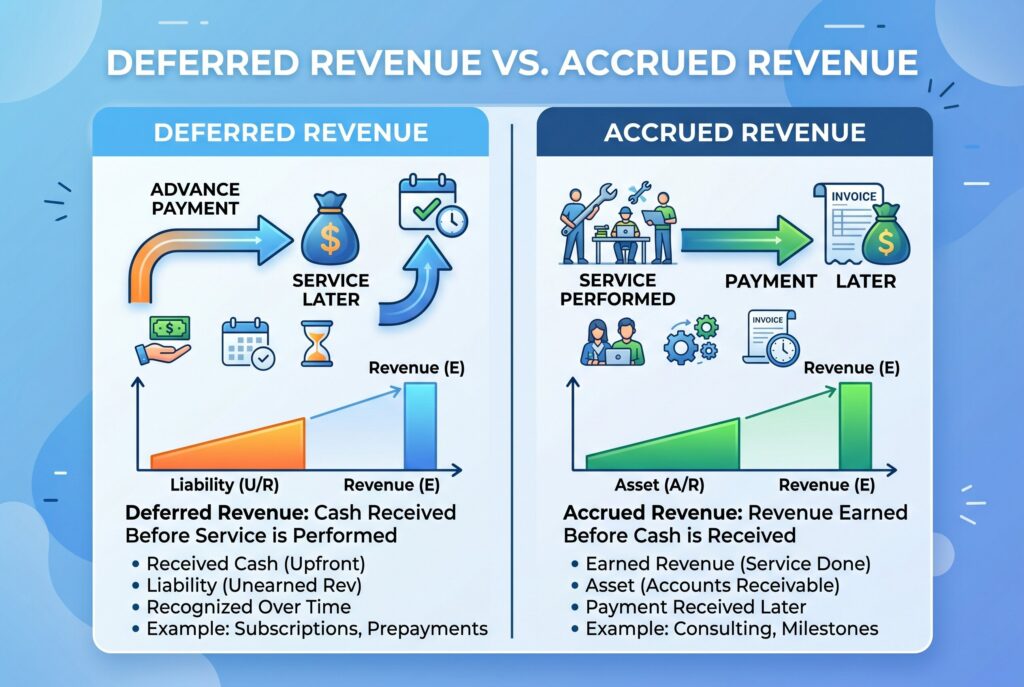

Deferred Revenue Vs. Accrued Revenue: The Timing Difference

Deferred revenue and accrued revenue are opposites in timing. Deferred revenue means cash is received first, and the service is delivered later. Accrued revenue means the service is delivered first, and cash is received later. For example, a customer pays upfront for a 12-month subscription. That is deferred revenue. The company has cash but still owes service.

Now imagine a consultant completes work in March but doesn’t bill the client until April. That is accrued revenue. The consultant has earned revenue but has not collected cash yet. This difference matters for cash flow. Deferred revenue improves cash flow upfront but creates future obligations. Accrued revenue improves reported revenue but does not create immediate cash.

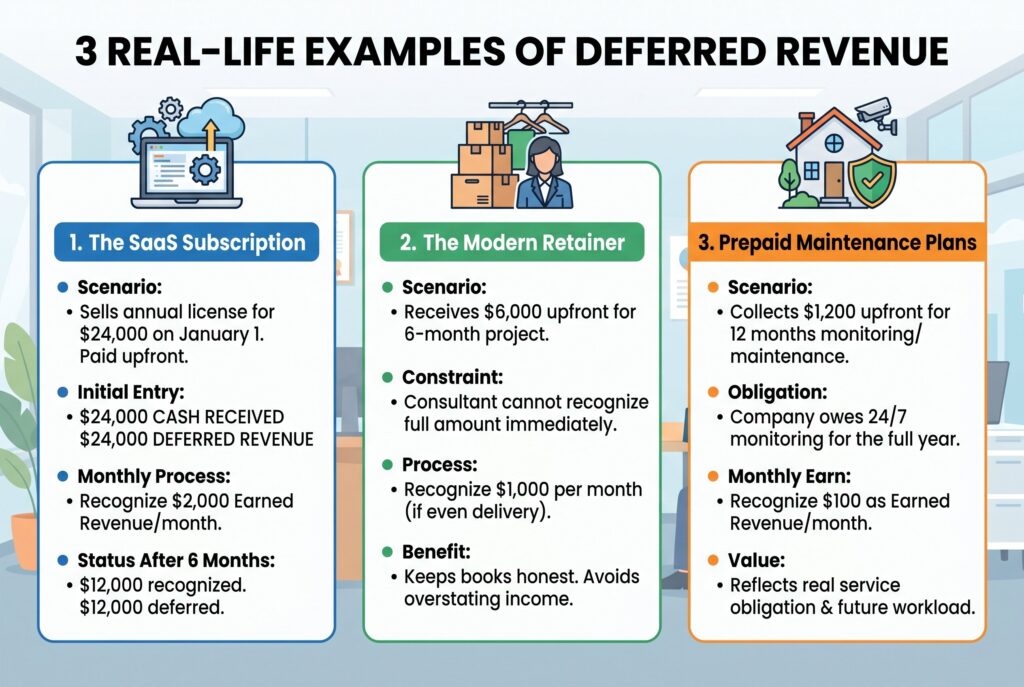

3 Real-Life Examples Of Deferred Revenue

1. The SaaS Subscription

A software company sells an annual license for $24,000 on January 1. The customer pays in full upfront. The company records $24,000 in cash and $24,000 in deferred revenue. Each month, the company recognizes $2,000 as earned revenue. After six months, $12,000 has been recognized and $12,000 remains deferred. This approach matches revenue with the period when the service is actually provided.

2. The Modern Retainer

A home organization consultant receives $6,000 upfront for a 6-month project. The client pays before the work begins, but the consultant can’t recognize the full amount immediately. If the work is delivered evenly, the consultant recognizes $1,000 per month. Until each month’s work is completed, the remaining balance stays as deferred revenue. This keeps the books honest and avoids overstating income.

3. Prepaid Maintenance Plans

A smart-home security company collects $1,200 upfront for 12 months of monitoring and maintenance. The company has cash on day one, but it owes 24/7 monitoring for the full year. Each month, $100 becomes earned revenue. The rest remains unearned revenue. This method reflects the real service obligation and gives a clearer view of future workload.

How To Record Journal Entries For Deferred Revenue

Deferred revenue accounting usually follows a two-step process. First, record the cash received and the liability. Second, recognize revenue gradually as the company delivers.

Initial entry when cash is received:

| Account | Debit | Credit |

|---|---|---|

| Cash | $12,000 | |

| Deferred Revenue | $12,000 |

This entry shows that cash increased, but revenue has not been earned yet.

Monthly adjusting entry:

| Account | Debit | Credit |

|---|---|---|

| Deferred Revenue | $1,000 | |

| Revenue | $1,000 |

This entry reduces the liability and records earned revenue. By the end of the service period, deferred revenue should be fully recognized if all obligations have been completed. Good accounting records are essential. Businesses should track contract start dates, end dates, billing terms, refund clauses, upgrades, downgrades, and cancellations. These details affect how revenue should be recognized.

Conclusion

Deferred revenue is not bad. In fact, upfront payments can strengthen cash flow and show strong customer demand. But that cash comes with responsibility. The company still has to deliver the promised product or service.

Business owners should avoid spending all upfront cash as if it were already earned profit. Tracking deferred revenue helps protect cash flow, improve financial reporting, and prevent revenue recognition mistakes. These days, any business using subscriptions, retainers, memberships, deposits, or prepaid services should build a clear recognition schedule before making spending decisions.