Is deferred revenue a liability? Yes. Deferred revenue is one of the most important balance sheet concepts for SaaS companies, subscription businesses, contractors, and accountants. If a business collects cash before delivering goods or services, that money can’t be treated as earned revenue yet. Misclassifying deferred revenue can overstate profit, hide obligations, and create serious financial reporting issues.

What Is Deferred Revenue? The 2026 Definition

What is deferred revenue? Deferred revenue is money a customer pays before the business has delivered the promised product or service. It is also called unearned revenue because the business has received cash but hasn’t earned it yet. For example, if a customer pays $12,000 for a one-year software subscription on January 1, the company receives all the cash upfront. However, it earns revenue month by month as it provides access to the software. The deferred revenue meaning is simple: cash comes first, performance comes later.

Why Is Deferred Revenue A Liability? The Accounting Logic

Deferred revenue is a liability because the company still owes the customer something. It may owe software access, a service period, a product shipment, a gift card redemption, or a future membership benefit. Is unearned revenue a liability? Yes. Until the company delivers what it promised, the customer has a claim on that money. If the business fails to deliver, it may need to provide a refund.

This follows the matching principle. Revenue should be recognized when the related goods or services are delivered, not simply when cash is received. That is why deferred revenue starts on the balance sheet as a liability and moves to the income statement only when earned.

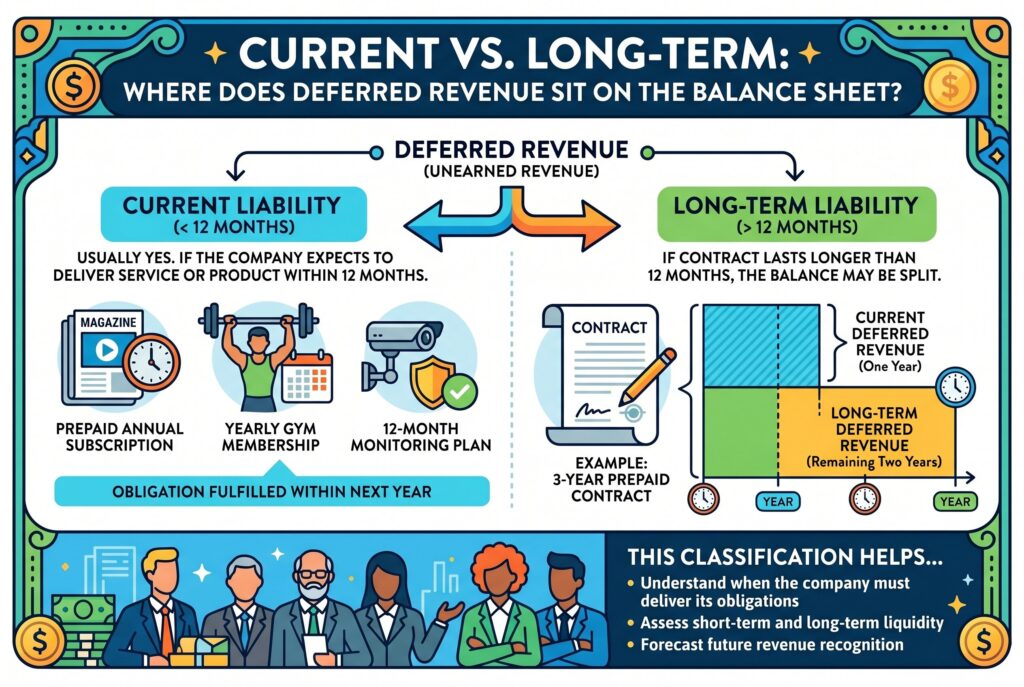

Current Vs. Long-Term: Where Does It Sit On The Balance Sheet?

Is deferred revenue a current liability? Usually, yes. If the company expects to deliver the service or product within 12 months, deferred revenue is classified as a current liability. For example, a prepaid annual subscription, yearly gym membership, or 12-month monitoring plan usually belongs in current liabilities. The obligation will be fulfilled within the next year.

If the contract lasts longer than 12 months, the company may need to split the balance. A three-year prepaid contract may have one year recorded as current deferred revenue and the remaining two years recorded as long-term deferred revenue. This classification helps investors, lenders, and managers understand when the company must deliver its obligations.

Balance Sheet Simulator

A balance sheet simulator can show how deferred revenue changes over time. Suppose a customer pays $24,000 upfront for a 12-month SaaS contract. On day one, cash increases by $24,000, and deferred revenue also increases by $24,000.

After the first month, the company recognizes $2,000 as revenue. Deferred revenue falls to $22,000. After six months, $12,000 has been recognized, and $12,000 remains as a liability. This visual flow is important because cash and revenue move differently. The business may have money in the bank, but part of that money still represents future service obligations.

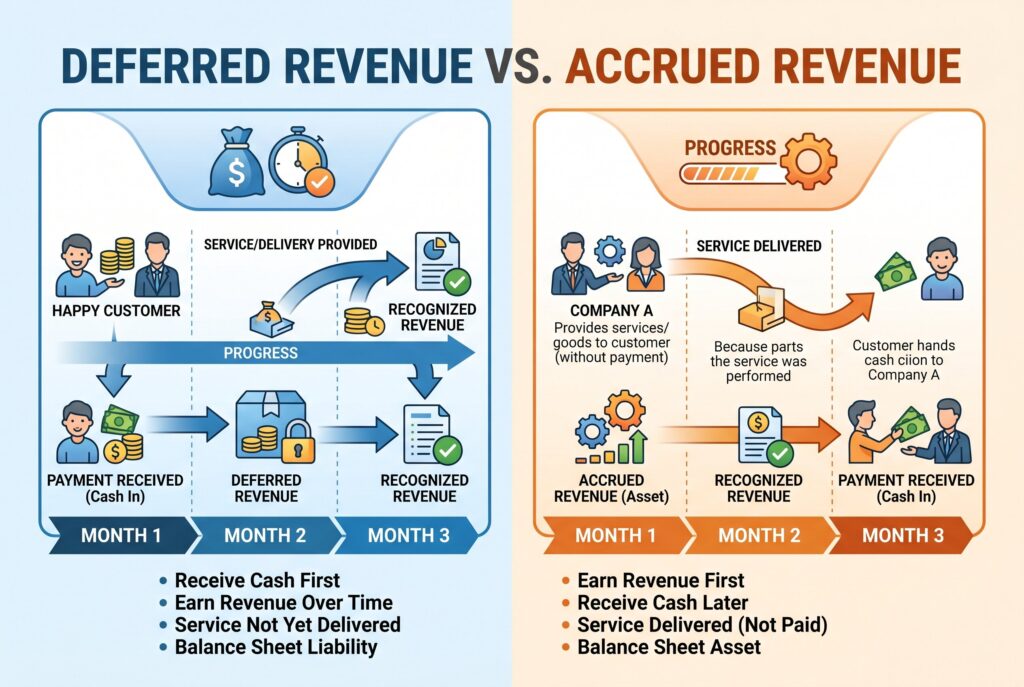

Deferred Revenue Vs. Accrued Revenue: Knowing The Difference

Deferred revenue and accrued revenue are opposites. Deferred revenue happens when cash is received before the business delivers. Accrued revenue happens when the business delivers before cash is received.

Concept | Timing | Balance Sheet Treatment |

|---|---|---|

Deferred Revenue | Cash first, work later | Liability |

Accrued Revenue | Work first, cash later | Asset or receivable |

For example, a prepaid software subscription creates deferred revenue. A consulting project completed before the invoice is paid creates accrued revenue. The key difference is cash timing. Deferred revenue improves cash flow upfront but creates an obligation. Accrued revenue shows earned income, but cash has not arrived yet.

How To Record Journal Entries: A Step-By-Step Guide

A deferred revenue journal entry has two main steps. First, record the upfront cash and liability. Second, recognize revenue as the company delivers.

When cash is received:

| Account | Debit | Credit |

|---|---|---|

| Cash | $12,000 | |

| Deferred Revenue | $12,000 |

This entry increases cash and records the obligation.

When revenue is earned monthly:

| Account | Debit | Credit |

|---|---|---|

| Deferred Revenue | $1,000 | |

| Revenue | $1,000 |

This entry reduces the liability and records earned revenue. After 12 months, the full $12,000 has moved from deferred revenue to recognized revenue. The same logic applies to annual subscriptions, retainers, maintenance plans, prepaid rent, gift cards, and membership fees.

The Impact On Your Financial Strategy

Deferred revenue can be good news, even though it appears as a liability. It shows customers are willing to pay upfront. That can strengthen cash flow and improve visibility into future demand. For SaaS companies, the difference between billings and revenue matters. Billings show the amount invoiced or collected. Revenue shows what has been earned under revenue recognition rules. A company may collect a large annual payment today, but only a portion becomes recognized revenue each month.

Investors often look at deferred revenue as a signal of customer commitment and retention potential. A growing deferred revenue balance may suggest strong prepaid demand, but it also means the company must continue delivering service. Business owners should be careful not to spend deferred revenue like free cash. If cancellations, refunds, or service failures occur, the company may need to return part of the money or continue fulfilling obligations without new cash coming in.

Conclusion

Deferred revenue is a liability because it represents money collected before the business has earned it. That may sound negative, but it often reflects healthy customer demand and strong upfront cash flow. The key is accurate tracking. Businesses should separate cash received from revenue earned, classify current and long-term obligations properly, and use clear revenue recognition schedules. Companies that manage deferred revenue well will have cleaner books, better forecasts, and stronger financial strategy.