Farmers renters insurance is a strong choice for renters who want broad protection, useful digital tools, and optional coverage that goes beyond a basic policy. In this Farmers renters insurance review, the quick verdict is clear. Farmers earns a solid 4.4 out of 5 because it offers dependable Farmers renters insurance coverage, several Farmers renters insurance discounts, a smooth app experience, and a lower than average level of NAIC complaints. The biggest downside is price. Farmers renters insurance rates average about $202 per year, or roughly $17 per month, which is higher than the national average of about $151 per year.

That doesn’t automatically mean it’s overpriced. For many renters, paying a few extra dollars each month can be worth it if the policy includes better service, stronger add ons, easier account management, and more confidence during a claim. Still, if you’re shopping only for the lowest renters insurance cost, Farmers may not be the first quote you choose.

What Does Farmers Renters Insurance Actually Cover?

Farmers renters insurance is a policy designed to protect your personal financial life while you rent a home, apartment, condo, or shared space. Your landlord’s insurance usually protects the building itself. It doesn’t protect your laptop, sofa, clothes, jewelry, kitchen items, or liability if someone gets hurt inside your rental.

A basic Farmers renters insurance policy can help after common events such as theft, fire, smoke damage, vandalism, certain water damage, and personal liability claims. Think of it as a financial shield around the things you own and the risks that come with living in a rented space. Without it, one break in or kitchen fire could force you to replace everything with your own savings.

Coverage Deep Dive: Standard vs. Optional Add Ons

| Coverage Type | What It Does | When It Helps |

|---|---|---|

| Personal property coverage | Helps repair or replace your belongings after a covered loss. | If your apartment is burglarized and your TV, laptop, or headphones are stolen. |

| Liability protection | May help cover legal costs, settlements, or medical-related expenses if you’re responsible for injury or damage. | If a guest slips in your apartment and decides to sue. |

| Additional living expenses | May help pay for temporary housing, meals, or extra costs if your rental becomes unlivable after a covered event. | If a fire forces you to stay in a hotel while repairs are made. |

| Identity theft coverage | Optional add-on that may help with costs related to restoring your identity after fraud or online scams. | If your personal information is stolen or misused. |

| Water backup coverage | Optional add-on that may help with damage from backed-up drains or sewer lines. | If you live on a lower floor or in an older building. |

| Earthquake insurance | Optional protection for renters in higher-risk earthquake regions. | If you live on the West Coast or another earthquake-prone area. |

| Replacement cost coverage | Optional upgrade that may replace damaged items with new ones instead of paying depreciated value. | If you want stronger protection for electronics, furniture, or everyday belongings. |

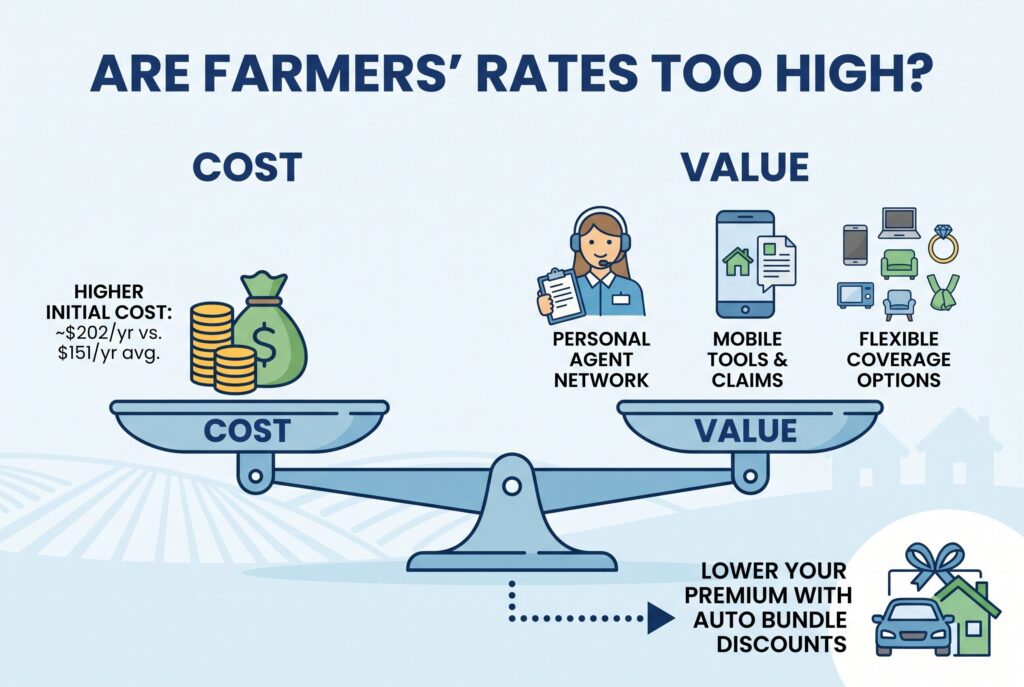

The Hidden Costs: Are Farmers’ Rates Too High?

Farmers renters insurance cost is the main concern for many shoppers. At about $202 per year, Farmers is above the national average of about $151 per year. That gap isn’t huge month to month, but it matters if you’re comparing renters insurance quotes closely.

So why might someone pay more? First, Farmers has a large agent network, which can be helpful if you want personal guidance instead of a fully automated experience. Second, the company’s mobile tools make it easier to manage a policy, view documents, and start a claim. Third, Farmers offers enough coverage options to build a policy around your real life rather than settling for the thinnest protection available.

The best way to reduce the price is to ask about a multi policy discount. If you bundle renters and auto insurance, Farmers may lower your total premium. This can be especially useful for renters who already need renters and auto insurance from the same household. A good auto and renters insurance bundle can make Farmers more competitive and easier to manage because your bills, policy documents, and service experience may stay in one place.

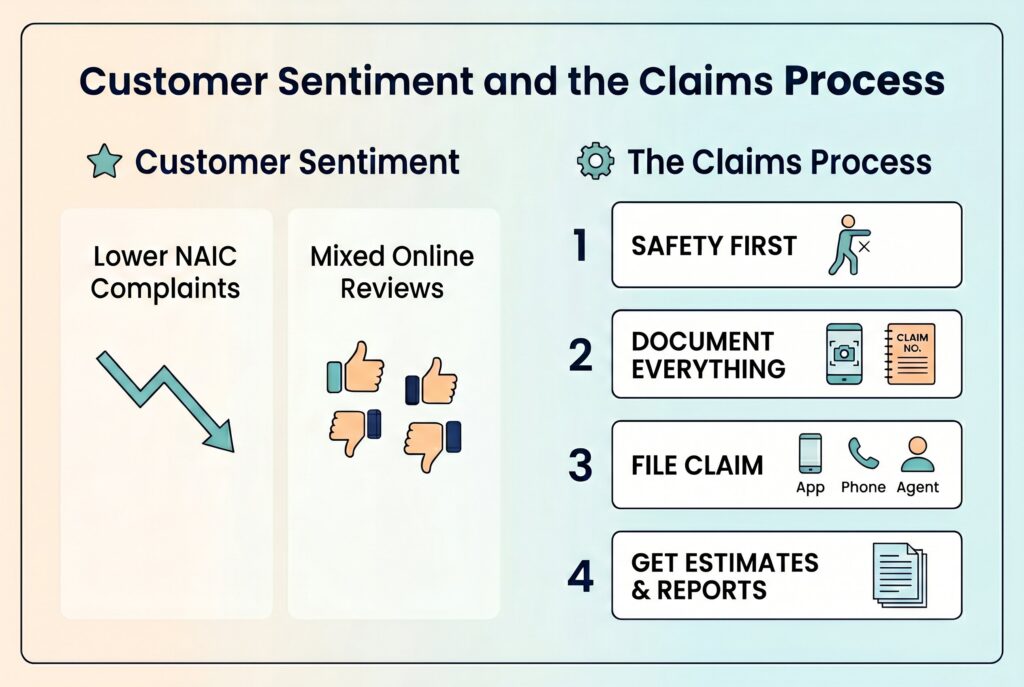

Customer Sentiment and the Claims Process

Farmers have a strong sign in its favor when it comes to NAIC complaints. A lower than average complaint level suggests that customers don’t complain to regulators as often as they do with many other insurers. That doesn’t guarantee every claim will go smoothly, but it’s a useful signal when reviewing an insurance company.

Public review sites can tell a more mixed story. Trustpilot Farmers reviews and BBB feedback often include complaints about slow responses, renewal price increases, or frustration during service interactions. This isn’t unusual for large insurance companies, but it’s still worth considering. A low online review score doesn’t mean Farmers won’t pay claims, but it does mean you should document everything carefully and stay organized.

To file a renters insurance claim, start by making sure everyone is safe and preventing further damage if possible. Then take photos or videos of the damage, list the missing or damaged items, gather receipts if you have them, and contact Farmers through the app, website, phone line, or your agent. Keep your claim number, write down every conversation, and save repair estimates or police reports when relevant. The better your documentation is, the easier the claims process usually becomes.

So, Is Farmers Renters Insurance Worth It?

Use this quick checklist to see whether Farmers renters insurance is likely to be a good fit for your needs.

| Question | If Yes | If No |

|---|---|---|

| Do you own valuable electronics, furniture, or home office equipment? | Farmers’ optional replacement cost coverage may provide stronger protection. | A basic renters policy from a lower-cost insurer may be enough. |

| Do you want access to local agents for advice and support? | Farmers’ large agent network can be a major advantage. | A digital-first insurer may offer similar coverage at a lower price. |

| Are you interested in bundling renters and auto insurance? | Multi-policy discounts may help offset Farmers’ above-average rates. | The pricing may be less competitive compared to some standalone renters policies. |

| Do you want optional coverages such as identity theft, water backup, or earthquake protection? | Farmers offers several add-ons that can help customize your policy. | You may not benefit from paying for a carrier known for broader coverage options. |

| Is customer service and claims support more important than finding the absolute cheapest premium? | Farmers may deliver better overall value despite the higher cost. | Comparing lower-priced insurers could make more sense. |

| Are you shopping primarily for the lowest renters insurance rate? | Farmers may still be worth a quote, especially if discounts apply. | Another insurer may offer a cheaper policy with adequate protection. |

Conclusion

Farmers renters insurance is best for renters who want solid coverage, flexible add ons, and the convenience of bundling car and renters insurance. It’s a good fit for people with valuable electronics, home office equipment, identity theft concerns, or a preference for working with an established insurer and agent network. It isn’t ideal for students, minimalists, or renters on a very tight budget who only want the cheapest possible policy. If price is your only priority, you should compare multiple renters insurance quotes before choosing.

Overall, Farmers renters insurance is worth considering in 2026 if you want a policy that balances coverage depth, digital convenience, and discount potential. It may cost more than average, but for renters who value stronger protection and practical support, that extra cost can be a smart trade.

Related Articles

Nationwide Renters Insurance 2026 Review: Rates & Hidden Costs