Nationwide renters insurance is a solid choice for renters who want reliable coverage and useful add-ons. Its standout feature, Brand New Belongings, helps replace damaged or stolen items at their full replacement cost rather than their depreciated value. The average Nationwide renters insurance cost is around $21 per month, close to the national average. This coverage can help protect your belongings and cover temporary living expenses after a covered loss. However, Nationwide isn’t available in some states, including Florida, Hawaii, and Massachusetts, and some customers report delays during the claims process.

The 2026 Pricing Matrix: What Will You Actually Pay?

Most renters want one clear answer before reading anything else: how much will I pay? The realistic answer is that your premium depends on where you live, your building type, your deductible, your claim history, your coverage limits, and whether you qualify for discounts. Still, a pricing matrix can make the numbers easier to understand.

- For a basic policy with about $15,000 in personal property coverage, many renters may pay around $15 to $18 per month. This level can work for students, minimalists, or renters with fewer expensive belongings. It’s cheap, but it may not be enough if you own a laptop, TV, furniture, gaming system, bicycle, and a full wardrobe.

- For a mid range policy with about $30,000 in personal property insurance, the cost may fall around $20 to $25 per month. This is often the more realistic choice for a typical apartment renter because replacing everyday belongings costs more than people expect. A couch, mattress, work setup, clothes, kitchen items, and electronics can quickly pass $30,000.

- For a higher limit policy with about $50,000 in personal property coverage, the monthly cost may be around $28 to $35. This may fit renters with high value electronics, designer items, musical instruments, home office gear, or a larger apartment.

The best way to lower the price is to ask about a multi-policy discount. If you already have auto insurance or plan to buy it, bundling it with Nationwide renters insurance may reduce your total bill. Just make sure the lower price doesn’t come with weaker limits or a deductible you can’t comfortably pay.

Nationwide Renters Insurance Rates at a Glance

While Nationwide renters insurance costs vary by location, coverage limits, deductible, and claims history, the table below shows typical pricing ranges renters may encounter.

| Personal Property Coverage | Estimated Monthly Cost | Best For |

|---|---|---|

| $15,000 | $15–$18 | Students, minimalists, and renters with fewer valuables |

| $30,000 | $20–$25 | Typical apartment renters with furniture, electronics, and everyday belongings |

| $50,000 | $28–$35 | Renters with expensive electronics, home office equipment, collectibles, or larger apartments |

Keep in mind that these are estimated ranges rather than guaranteed prices. Your actual Nationwide renters insurance quote may be higher or lower depending on:

- ZIP code and local crime rates

- Building age and construction type

- Deductible selection

- Claims history

- Coverage limits and endorsements

- Available discounts

One of the easiest ways to lower your premium is through a multi-policy discount. If you already carry Nationwide auto insurance, bundling both policies may reduce your overall insurance costs while simplifying account management.

Typical Scenarios: How Nationwide Actually Pays Out

Insurance terms can sound dry until you connect them to real life. The difference between landlord vs renters insurance is a perfect example. Your landlord’s policy usually protects the building itself. It doesn’t protect your sofa, laptop, shoes, clothes, TV, or personal liability as a renter. That’s your responsibility.

1. The Stolen Laptop and the Brand New Belongings Rule

Imagine your apartment is broken into while you’re at work. Your four year old laptop, originally worth $1,200, is stolen. A standard actual cash value policy may only pay what the laptop is worth today after depreciation, maybe around $300. That’s painful because you still need a working computer, and $300 won’t buy the same quality replacement.

This is where the Brand New Belongings endorsement becomes valuable. With this upgrade, Nationwide may help you replace the stolen item with a new version instead of leaving you with only the depreciated value. For renters with laptops, tablets, phones, cameras, furniture, and work equipment, this endorsement can be the difference between partial recovery and real recovery.

2. The Burst Pipe Disaster

Now picture a pipe bursting in the apartment above yours. Water leaks through the ceiling, ruins your clothes, damages your furniture, and makes your bedroom unusable. Your landlord may repair the ceiling and plumbing, but that doesn’t mean they’ll replace your belongings. Personal property insurance can help pay for damaged items, while loss of use coverage may help with temporary living expenses if your apartment becomes unlivable after a covered event. That could mean hotel costs, extra food expenses, or short term housing while repairs happen. For renters living paycheck to paycheck, this protection isn’t just convenient. It can prevent a short term disaster from becoming a long term financial setback.

3. Identity Theft Protection

Identity theft coverage is one of the more useful renters insurance add-ons because modern renters live so much of life online. A stolen wallet, hacked account, or compromised personal information can create hours of stress and unexpected costs. This add on may help with certain expenses related to restoring your identity, such as document replacement, legal support, or recovery services depending on the policy terms. It isn’t the first coverage most renters think about, but it’s increasingly relevant. Your belongings aren’t only physical anymore. Your identity, credit, accounts, and digital life also need protection.

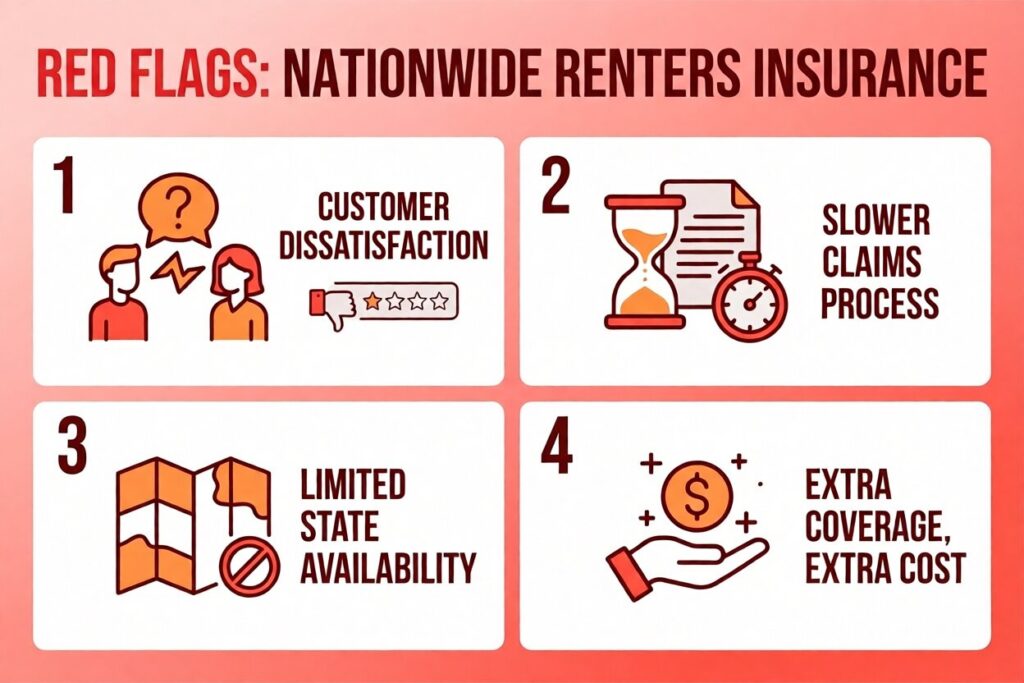

The Red Flags: Hidden Costs and Customer Complaints

Customer Satisfaction Concerns

The biggest red flag is customer satisfaction. Some Nationwide customer reviews mention frustration with communication, claim delays, and service issues. A low Trustpilot score, reported around 1.5 out of 5, doesn’t automatically mean every renter will have a bad experience, but it’s a signal worth taking seriously.

Claims May Require More Patience

The Nationwide claims process may also feel slow if you expect instant digital service. Insurance claims require documentation, review, and approval. That means you should keep receipts, take photos of valuable belongings, record serial numbers when possible, and create a home inventory before anything happens. A claim is much easier when you can prove what you owned and what it was worth.

Limited Availability in Some States

Geographic availability is another issue. Nationwide renters insurance isn’t available everywhere, and renters in excluded states such as Florida, Hawaii, and Massachusetts may need to look elsewhere. Before comparing add-ons or discounts, first confirm that coverage is available in your ZIP code.

Optional Coverage Can Increase Costs

There may also be hidden costs if you choose extra endorsements, lower deductibles, higher limits, or special protection for valuables. These upgrades can be worth it, but they’ll raise the premium. The key is to pay for protection you actually need, not every optional feature available.

Is Nationwide Renters Insurance Worth It?

Use this checklist to see whether Nationwide is a strong match for your situation:

| Question | If Yes | If No |

|---|---|---|

| Do you own expensive belongings such as laptops, cameras, jewelry, or gaming equipment? | Nationwide may be worth considering because Brand New Belongings coverage can help replace items at replacement cost. | Basic renters insurance from another provider may be sufficient. |

| Do you already have Nationwide auto insurance? | Bundling may unlock additional multi-policy discounts. | Compare standalone renters insurance quotes from multiple insurers. |

| Do you prefer managing multiple policies with one company? | Nationwide’s bundle options may simplify billing and account management. | The convenience advantage may be less important to you. |

| Is replacement cost coverage a priority? | Nationwide’s optional endorsement is one of its strongest features. | You may find cheaper policies focused on basic protection. |

| Are you comfortable handling some claims and account tasks online? | Nationwide can be a practical fit. | Consider comparing providers known for stronger digital customer experiences. |

| Is Nationwide renters insurance available in your state? | You can move forward with a quote comparison. | You’ll need to consider alternative insurers. |

Conclusion

Nationwide renters insurance offers solid value, affordable pricing, and stronger-than-average protection for personal belongings. While it has some limitations, its replacement-cost coverage and practical add-ons make it a strong choice for renters seeking reliable financial protection and peace of mind.

Related Articles

Farmers Renters Insurance Review: Is the 2026 Policy Worth It?