")

If you’ve just had an accident that wasn’t your fault, you may be wondering what is subrogation in insurance. In plain English, subrogation means your insurance company steps into your shoes. Your insurer pays your covered loss first so you don’t have to wait for the at fault party to pay. Then your insurer uses your legal right to recover that money from the person who caused the damage or from that person’s insurance company. This process can help you get repairs, medical care, and claim payments faster. It can also help you recover your deductible.

The #1 Consumer Question: Will I Get My Deductible Back?

For most policyholders, the biggest practical question isn’t legal theory. It’s this: will I get my deductible back?

The answer depends on whether your insurer successfully recovers money from the at fault party.

If recovery is complete, many insurers reimburse the deductible. If recovery is partial, reimbursement may also be partial. If the other driver is uninsured, unreachable, judgment proof, or fault is disputed, recovery may take longer or may not happen. The best move is to stay organized. Keep copies of repair estimates, photos, police reports, medical bills, claim numbers, and all insurer messages. Ask your claims adjuster when subrogation began, whether the other insurer accepted fault, and how deductible recovery will be handled.

What Can Delay Subrogation?

Subrogation isn’t always quick. Several issues can slow the process. Fault may be disputed. If both drivers share blame, insurers may negotiate percentages of responsibility. The at fault party may have no insurance. In that case, recovery becomes harder. The other insurer may deny coverage. This can happen if the policy lapsed, the driver was excluded, or the incident falls outside the policy. Documents may be missing. Without proof of damage, bills, fault, and payment, recovery becomes slower. A signed release can also create problems. If you settle directly with the at fault party and sign away claims without telling your insurer, you may damage your insurer’s subrogation rights.

The B2B Angle: What Is a Waiver of Subrogation?

A waiver of subrogation is a contractual agreement that prevents an insurer from seeking reimbursement from another party after paying a covered claim. These waivers are commonly used in leases, construction contracts, and business agreements to reduce disputes and preserve business relationships. For example, if a landlord’s insurer pays for fire damage, it may not be able to sue the tenant for reimbursement when a valid waiver applies. Because some insurance policies require insurer approval, businesses should review their coverage before agreeing to a waiver of subrogation.

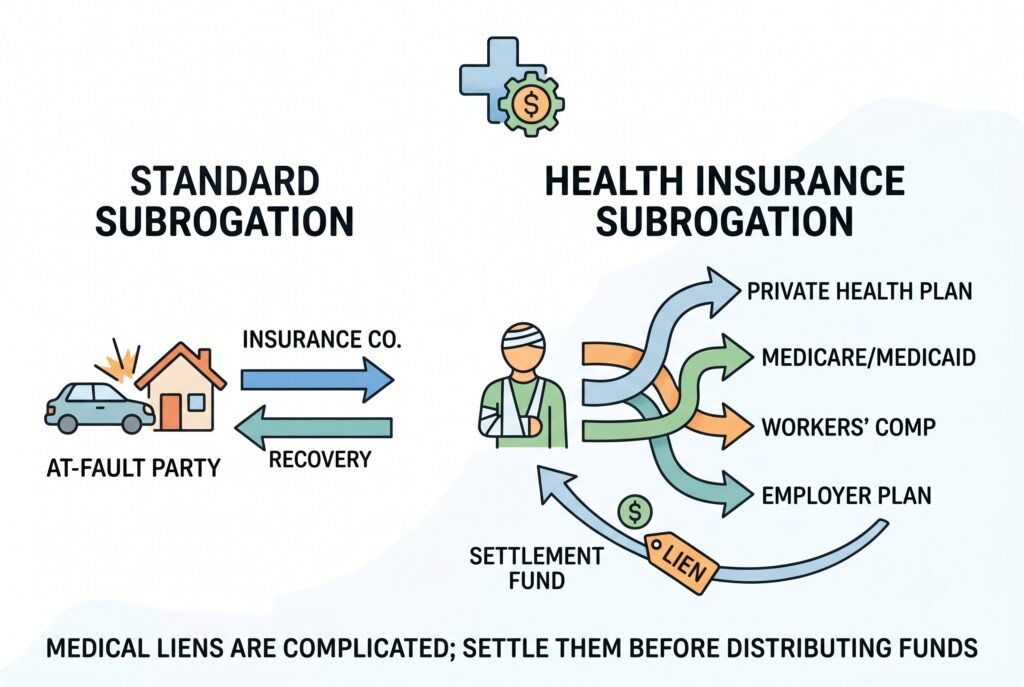

Health Insurance Subrogation: Why It’s Different

Health insurance subrogation can be more complicated than auto or property claims because medical bills may overlap with personal injury settlements.

Different payers have different rules. Private health plans, Medicare, Medicaid, workers’ compensation, and employer sponsored plans may each have separate reimbursement rights.

Some cases may involve doctrines or rules that limit reimbursement if the injured person hasn’t been fully compensated. Other cases may give the health plan stronger recovery rights. That is why injury settlements should account for medical liens before money is distributed. Ignoring a reimbursement claim can lead to collection efforts later.

Action Plan: What to Do If You Receive a Subrogation Letter

- First, don’t ignore it. A subrogation letter usually means an insurer is preserving its reimbursement rights.

- Second, don’t sign a release with the at fault party without understanding the effect. A release may prevent your insurer from recovering money and may create problems with your own claim.

- Third, ask for details. If a health insurer claims reimbursement, request an itemized lien showing what was paid, when it was paid, and how each charge relates to the accident.

- Fourth, keep communication open. Give your insurer accident reports, photos, invoices, and contact details for the other party.

- Fifth, track your deductible. Ask your adjuster whether deductible reimbursement will be automatic or whether you need to submit a request.

Conclusion

Subrogation allows your insurance company to pay a covered claim on your behalf and then seek reimbursement from the party responsible for the loss. This process often benefits policyholders by speeding up claim payments, placing financial responsibility on the at-fault party, and potentially helping recover some or all of a deductible.

Still, subrogation isn’t always simple. Auto claims, health insurance liens, business waivers, partial fault, and settlement releases can all change the outcome. The safest approach is to communicate with your insurer, preserve evidence, avoid signing releases too quickly, and confirm how deductible reimbursement will be handled before the claim closes.