")

For many parents, college planning feels less like a spreadsheet exercise and more like preparing for an uncertain future. A 529 calculator helps estimate how your savings can grow based on your starting balance, monthly contributions, investment returns, and time until college. It also shows the value of tax-free growth and qualified withdrawals, helping you understand whether saving $100, $300, or $500 per month can build enough momentum to cover future education costs.

Interactive Tool: The 2026 Tax Free 529 Estimator

2026 Tax Free 529 Estimator

Estimate how a 529 plan may grow over time. Enter your child’s current age, current savings, monthly contribution, expected annual return, and expected college cost.

Future Value = Current Savings × (1 + Annual Return)Years + Monthly Contributions Future Value

Monthly Contributions Future Value = Monthly Contribution × [((1 + Monthly Return)Months − 1) ÷ Monthly Return]

Gap or Surplus = Projected 529 Balance − Expected College Cost

Use a 529 plan calculator by starting with four inputs: your child’s current age, your current savings, your planned monthly contribution, and your estimated annual return. Then compare the result against your expected college cost. The goal isn’t to predict the future perfectly. It’s to create a monthly savings target that feels realistic and adjustable.

For example, a parent who invests $300 per month for 18 years may contribute $64,800 before investment growth. If the account earns a steady long term return, the final balance may be far higher because each year’s gains can create future gains. A 529 savings calculator makes that compounding visible, which is powerful because the hardest part of college planning is often starting early enough.

What If My Child Doesn’t Go to College?

This is the biggest fear many parents have before funding a 529 plan. What if your child skips college, chooses trade school, starts a business, joins the workforce, or simply takes a different path? For years, parents worried that unused 529 money could become trapped, and non-qualified withdrawals could trigger taxes and penalties on investment gains.

But the 2026 rulebook gives families a powerful legal escape hatch.

Under the SECURE 2.0 Act, unused 529 funds may be rolled into a Roth IRA for the beneficiary, tax-free and penalty-free, as long as certain requirements are met. The lifetime rollover limit is $35,000 per beneficiary.

That means overfunding a 529 is no longer the same scary problem it used to be. If your child doesn’t need all the money for college, part of that leftover balance may become the foundation of their retirement savings instead.

Key requirements include: the 529 account must generally be open for at least 15 years, rollovers are subject to annual Roth IRA contribution limits, and the Roth IRA must belong to the 529 beneficiary.

For parents, this changes the psychology of college savings. A 529 plan is no longer just a “college-or-penalty” account. It can also become a backup retirement starter fund for your child if their education path costs less than expected.

The Reality Slap Chart: 529 vs. Taxable Savings

A 529 savings calculator becomes much more powerful when it does more than show a final balance. The real value appears when families can compare two paths side by side: saving in a regular taxable account versus saving inside a 529 plan.

Step 1: Start With the Same Assumptions

Assume a family contributes $300 per month for 18 years and earns an average annual return of 7%.

The total contribution would be:

$300 × 12 months × 18 years = $64,800

At this point, both strategies start from the same place. The difference comes from how taxes affect investment growth.

Step 2: Show the Taxable Account Result

In a regular taxable investment account, dividends and capital gains may be taxed along the way. That tax drag reduces the amount of money left to compound each year. Even if the account earns solid returns, part of the growth may be lost to taxes before the money is ever used for college.

Step 3: Show the 529 Plan Result

In a 529 plan, qualified education withdrawals are federally tax free. That means investment gains can keep compounding without the same annual tax drag, as long as the money is used for eligible education expenses. Over 18 years, this tax advantage can create a meaningful gap.

Step 4: Put the Results Side by Side

| Savings Strategy | Monthly Contribution | Time Period | Key Tax Treatment | Estimated Outcome |

| Taxable Investment Account | $300 | 18 years | Investment growth may be reduced by taxes | Lower after tax college savings |

| 529 Plan | $300 | 18 years | Qualified withdrawals are tax free | Higher after tax college savings |

Step 5: Explain the Real Takeaway

The point isn’t just that a 529 plan may produce a larger final balance. The deeper lesson is that taxes can quietly weaken compound growth over time. A taxable account may look flexible, but every year of tax drag can reduce the power of compounding. A 529 plan, by contrast, allows more of the investment growth to remain inside the account and continue working for the family.

That is why the best 529 savings calculators should not only answer, “How much will I have?” They should also show, “How much more could I keep by using a tax advantaged account?” For families saving over 10, 15, or 18 years, the difference can become large enough to affect how much debt a student needs, how much parents must pay out of pocket, and how prepared the family feels when tuition bills arrive.

| Factor | Traditional Taxable Investment Account | 529 College Savings Plan |

| Monthly Contribution | $300 | $300 |

| Investment Period | 18 years | 18 years |

| Average Annual Return | 7% | 7% |

| Taxes on Dividends | Yes | No |

| Taxes on Capital Gains | Yes | No (when used for qualified education expenses) |

| Impact on Compound Growth | Reduced over time by annual taxes | Uninterrupted tax-free compounding |

| Long-Term Wealth Accumulation | Lower | Higher |

| Potential Difference After 18 Years | Loses part of the returns to taxes | May accumulate tens of thousands of dollars more |

| Primary Advantage | Greater flexibility in how funds are used | Tax-free growth for education expenses |

| Key Takeaway | Taxes create a drag on long-term growth | Time and tax efficiency maximize the power of compounding |

State Specific Tax Hacks: You Don’t Have to Buy Local

Many investors assume they must use their own state’s 529 program. That’s not always true. While some states provide valuable state tax deductions or credits for contributions to their own plans, others provide little or no tax benefit. This creates an opportunity many families overlook.

A 529 plan calculator should evaluate not only projected growth but also state specific tax advantages, investment choices, administrative costs, and long term performance. Sometimes staying local makes sense because of tax deductions.

Sometimes another state’s plan offers lower fees, stronger investment options, or better long term value. Sophisticated investors often compare multiple programs before committing. They focus on net results rather than geographic loyalty. Low fees matter enormously over eighteen years of compounding. Even seemingly small differences can significantly affect final account balances. That’s why a comprehensive 529 calculator analysis should always include expense ratios and state tax considerations.

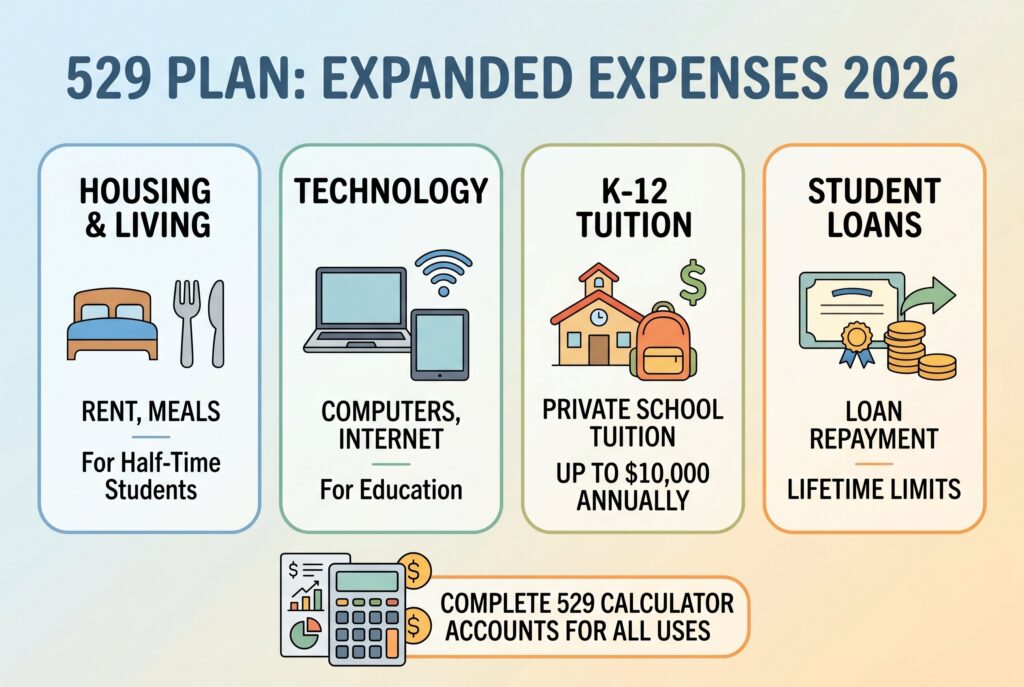

Beyond Tuition: Surprising Qualified Expenses in 2026

Many parents assume 529 plans cover only college tuition. That’s no longer accurate. Today’s qualified expense rules are much broader than most families realize.

Housing and Living Expenses

If the student attends school at least half time, certain housing expenses may qualify. This can include off campus housing, rent, and meal costs within approved limits established by the institution.

Technology and Internet

Modern education depends on technology. Computers, laptops, educational software, and internet access often qualify when required for educational purposes. These costs can add up quickly throughout a college career.

K Through 12 Education

Many families don’t realize that 529 funds can be used for certain private elementary and secondary school tuition expenses. Current rules allow qualified distributions of up to $10,000 annually per student for eligible K through 12 tuition expenses.

Student Loan Repayment

Another valuable benefit involves student loans. Under current regulations, certain 529 assets may be used toward student loan repayment. Lifetime limits apply, but this flexibility creates another option for families managing educational debt. A complete 529 college savings plan calculator should account for these expanded uses because they can influence how much families choose to save.

The Hidden Superpower: Starting Early Beats Saving More

Parents often focus entirely on contribution size. The bigger factor is usually time. Consider two families. Family A begins contributing $200 per month when their child is one year old. Family B waits until the child turns ten and contributes $400 per month. Despite contributing less money each month, Family A may achieve similar or even better results because compound growth had additional years to work. This is where a 529 calculator growth projection becomes so powerful.

It visually demonstrates that time is often the most valuable asset in education planning. The earlier contributions begin, the harder compound interest works on your behalf. Waiting for the perfect financial situation often costs more than starting with a smaller contribution today.

Conclusion

When you look at projections from a 529 calculator, the biggest lesson isn’t how much college may cost. It’s how powerful time can be. The combination of tax free growth, tax free qualified withdrawals, expanded qualified expenses, and the new Roth IRA rollover opportunity makes the modern 529 plan more flexible than ever before.

The question isn’t whether college costs will continue rising. The question is whether your money will have enough time to compound before those bills arrive. A 529 savings calculator can provide the numbers, but the decision belongs to you. The families that benefit most aren’t necessarily the wealthiest. They’re the ones who start early, remain consistent, and allow compounding to do the heavy lifting over time.