Many people use asset and wealth management as if they mean the same thing, but choosing the wrong service can cost you thousands of dollars in unnecessary fees. The core difference between asset management and wealth management is scope. Asset management focuses on your investment portfolio. It helps grow and manage assets such as stocks, bonds, ETFs, mutual funds, and alternatives. Wealth management is broader. It includes investment management, but also retirement planning, tax strategy, estate planning, insurance, business succession, and family financial decisions. In short, asset management grows the money. Wealth management coordinates the whole financial life around that money.

Asset Management: The Investment Engine

Asset management is mainly about portfolio management. An asset manager’s job is to decide how your capital should be invested based on your goals, time horizon, and risk tolerance.

They may build a mix of equities, fixed income, cash, real estate funds, private assets, or alternative investments. They monitor performance, rebalance allocations, manage risk, and adjust the portfolio when markets change. This service can be ideal if your financial life is fairly simple. For example, you may already have stable income, simple taxes, no complex estate issues, and one main need: getting professional help with investments.

Asset management can be active or passive. Active managers try to outperform the market through research and security selection. Passive managers use index funds or ETFs to capture market returns at lower cost. Neither approach is automatically best. The right choice depends on fees, tax impact, market exposure, and your belief in the manager’s ability to add value.

Wealth Management: The Holistic Blueprint

In the debate over asset management vs wealth management, wealth management is the wider umbrella. It includes portfolio management, but it doesn’t stop there.

A wealth manager looks at your full financial life. That means investments, taxes, retirement income, estate planning, insurance, charitable giving, debt strategy, business interests, and family goals. For high-net-worth individuals, this broader planning can matter more than chasing an extra 1% of investment return. A strong portfolio won’t help much if poor estate planning creates avoidable taxes, family disputes, or liquidity problems after death.

Wealth management becomes especially valuable when your assets include multiple properties, business ownership, stock options, private equity, cross-border issues, trusts, or future inheritance planning. It isn’t just about making money grow. It’s about protecting, transferring, and coordinating wealth across decades.

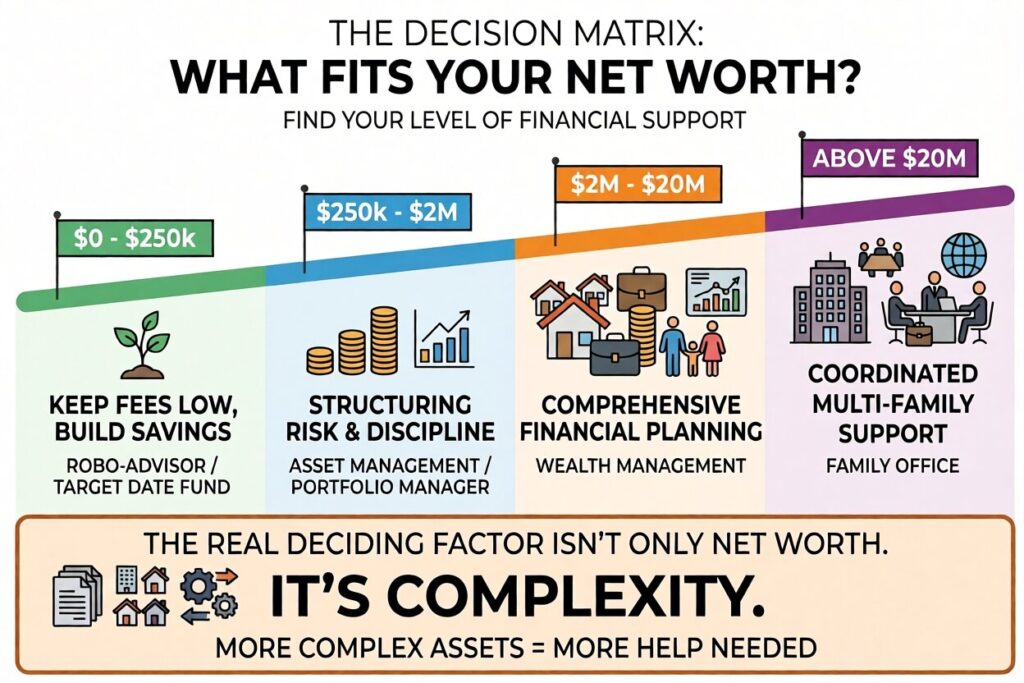

The Decision Matrix: What Fits Your Net Worth?

- Below $250,000, many investors don’t need a full wealth manager. A robo-advisor, target date fund, or low cost financial planning platform may be enough. At this stage, keeping fees low and building consistent savings often matters more than complex strategy.

- From $250,000 to $2 million, asset management may be enough. You likely have meaningful investable assets, but your tax and estate needs may still be manageable. A portfolio manager or investment advisor can help structure risk and improve discipline.

- From $2 million to $20 million, wealth management often becomes more useful. At this level, tax planning, estate documents, insurance coverage, charitable planning, and retirement income strategy can affect your net worth as much as investment returns.

- Above $20 million, family office wealth management may become appropriate. Families at this level often need coordinated support from investment professionals, tax advisors, attorneys, estate planners, business succession experts, and sometimes family governance specialists.

The real deciding factor isn’t only net worth. It’s complexity. A person with $1 million, a simple job, and a retirement account may need less help than a business owner with $800,000 spread across company equity, real estate, loans, and tax exposure.

The Hidden Trap: Fiduciary Duty and Compensation Models

The biggest risk isn’t choosing asset management or wealth management. It’s choosing an advisor whose incentives don’t match yours. Compensation models matter.

A commission based advisor may earn money when they sell certain products. That doesn’t automatically make them dishonest, but it can create conflicts of interest. They may be paid more to recommend one fund, annuity, or insurance product over another.

A fee-based advisor may charge fees and also receive commissions. This can be confusing because the phrase sounds similar to fee-only. A fee-only advisor is paid directly by clients, often through a flat fee, hourly fee, subscription fee, or percentage of assets under management. This model can reduce product sales conflicts, though it doesn’t eliminate every incentive issue.

The gold standard is fiduciary duty. A fiduciary is legally required to put your interests first. Before hiring anyone, ask whether they act as a fiduciary at all times, how they’re paid, what conflicts exist, and whether they can explain fees in writing.

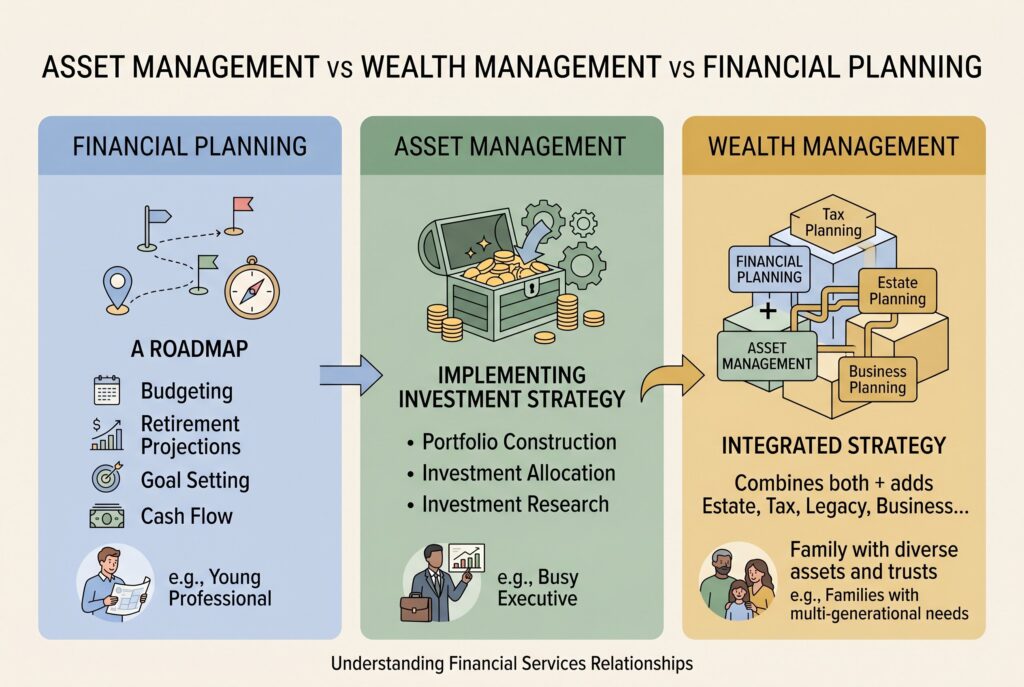

Asset Management vs Wealth Management vs Financial Planning

Financial planning is another term that often gets mixed into this conversation.

- Financial planning usually focuses on creating a roadmap. It may include budgeting, retirement projections, insurance review, college planning, cash flow, and goal setting.

- Asset management implements the investment side of that roadmap.

- Wealth management combines both, then adds tax, estate, legacy, business, and family strategy when needed.

A young professional may need financial planning first. A busy executive may need asset management. A family with business assets, trusts, and inheritance concerns may need wealth management.

Final Thoughts

The choice between asset management vs wealth management isn’t about which service sounds more prestigious. It’s about how complicated your financial life has become.

Asset management is the investment engine. It helps grow and manage your portfolio. Wealth management is the full blueprint. It coordinates investments with taxes, retirement, estate planning, insurance, business succession, and family goals.

If your needs are simple, don’t overpay for complexity. If your wealth is complex, don’t rely on portfolio management alone. The right advisor should match your net worth, your risks, your goals, and your need for coordination. Most importantly, they should explain exactly how they’re paid and whether they truly owe you fiduciary duty.