Are annuities a good investment? For many pre-retirees and retirees, that question comes down to one thing: can an annuity create dependable income without introducing too much cost, complexity, or risk? The answer isn’t a simple yes or no. Annuities can be useful tools for people who want predictable retirement cash flow, tax-deferred growth, or protection from outliving their savings. But they can also come with fees, surrender restrictions, inflation risk, and insurer-specific safety concerns. If you’re evaluating annuities seriously, the smartest approach is to look at the product type, the contract terms, and your existing retirement income structure before making any decision.

What Is an Annuity and How Does It Work?

An annuity is a contract with an insurance company. In the accumulation phase, you put money into the contract, either in a lump sum or through contributions over time. In the payout phase, the annuity can begin sending money back to you as income, either for a set number of years or for life. That’s the core appeal: turning savings into a more predictable stream of retirement cash flow.

Some annuities start paying quickly, while others are deferred and designed to grow first. An income annuity is generally used when someone wants regular payouts rather than ongoing asset accumulation. That’s why annuities often appeal to retirees who worry less about maximizing growth and more about making sure monthly bills can still be paid 20 or 30 years from now.

Understanding the Fixed Annuity

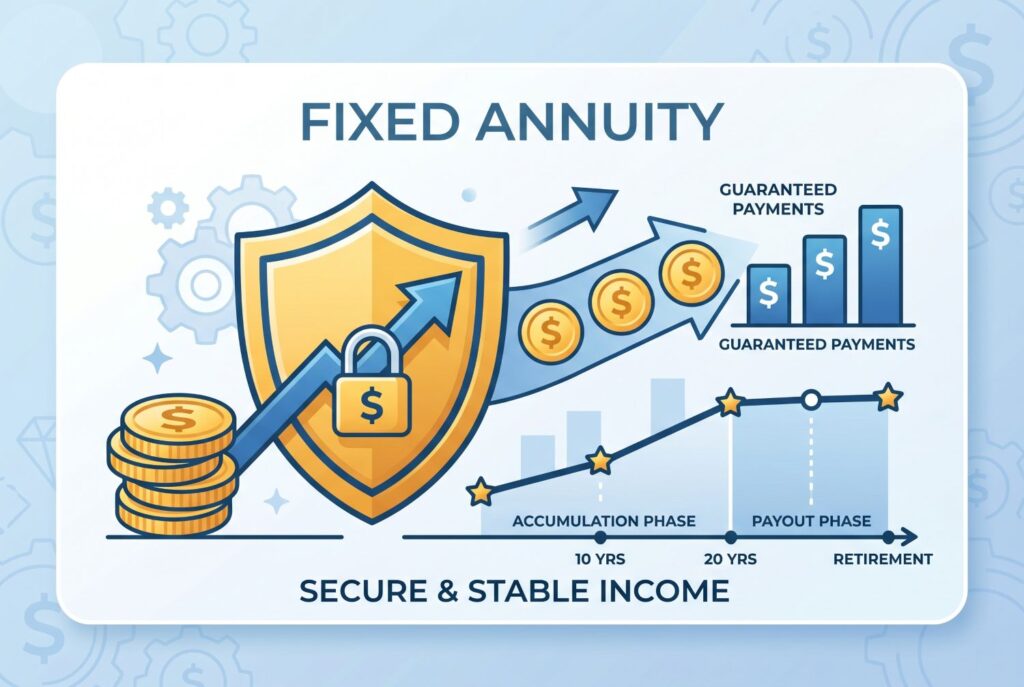

If you’re asking what is a fixed annuity, think of it as the simplest version of the product. A fixed annuity generally offers a stated rate of return or a contract-backed crediting structure that doesn’t fluctuate with the stock market. A fixed rate annuity appeals to conservative savers because the growth path is more stable and easier to understand than market-linked alternatives.

That simplicity is a major strength. Fixed annuities are often easier to explain, easier to predict, and easier to compare with other conservative income tools. But even here, the decision isn’t automatic. Stability may come at the cost of lower upside, and long-term inflation can erode the purchasing power of fixed payments if the contract doesn’t include meaningful inflation protection.

Exploring the FIA Investment: Is a Fixed Index Annuity Right for You?

A fixed index annuity, often shortened to FIA investment language in marketing materials, sits between a plain fixed annuity and a variable annuity. It’s designed to protect principal from direct market losses while allowing some upside based on the performance of a market index. That’s exactly why so many people find the category appealing: it promises a safer structure than direct equity investing while still offering the chance for better growth than a plain fixed annuity.

So what is an FIA investment in practical terms? It’s an annuity where returns are linked to an index formula rather than full market participation. That distinction matters. You don’t simply get “the market return.” Instead, insurers apply rules such as caps, spreads, and participation rates.

A cap is the maximum credited return you can receive during a defined period. If the index rises above that cap, your credited gain still stops at the contract limit. A spread is the portion of the index return the insurer subtracts before crediting interest. If the index gains 8% and the spread is 3%, the credited amount may be closer to 5%. A participation rate tells you how much of the index’s gain counts toward your credited return. If the participation rate is 70% and the index gains 10%, the credited return may be 7%, subject to other contract terms.

This is why fixed index annuity products can feel confusing. The concept sounds simple, but the contract mechanics are where the real tradeoffs live. A fixed index annuity may be appropriate for a conservative investor who wants downside protection and can tolerate complexity. It may be a poor fit for someone who assumes it will behave like a direct stock-market investment.

Are Annuities a Good Investment? The Real Pros and Cons

The best way to answer whether annuities are a good investment is to stop treating them like a magic solution and look at the real pros and cons of annuities.

The Pros: Guaranteed Income and Tax-Deferred Growth

The strongest argument in favor of annuities is guaranteed income. For retirees who don’t have a pension, that promise can be extremely valuable. A well-chosen annuity can create income that feels more like a paycheck, which helps reduce longevity risk, the risk of living longer than your assets can safely support.

Tax-deferred growth is another major benefit. Gains inside the annuity generally grow without immediate annual taxation, which can be attractive for savers who want to delay taxes until withdrawal. For some households, that can complement other retirement planning tools rather than replace them.

The Cons: Fees, Inflation, and Liquidity Issues

Now the harder side. Annuities pros and cons discussions often mention fees, but many articles don’t show how seriously they can shape results. Depending on the product, costs may include mortality and expense charges, rider fees, administrative costs, and embedded pricing through spreads or participation limits. Even if the contract doesn’t show every cost in one line item, it doesn’t mean the product is cheap.

Liquidity is another issue. Surrender charges can make it expensive to access your money early. That means annuities usually aren’t ideal for funds you may need soon, or for people who haven’t yet built solid emergency reserves.

Inflation is the quieter risk. A fixed payout that looks reassuring today may feel much smaller 20 years later. If inflation averages even modestly over a long period, the real spending power of a flat monthly payment can shrink dramatically. That’s one reason annuities shouldn’t automatically absorb all of a retiree’s assets. A guaranteed payment is useful, but it isn’t immune to the long-term math of rising prices.

The Safety Check: Are Annuities Safe?

Are annuities safe? In general, annuities are safer than many market-linked products in one specific sense: they’re insurance contracts designed to deliver income and preserve certain guarantees. But “safe” doesn’t mean “risk-free.”

The biggest safety issue is the financial strength of the insurer. The guarantees are only as strong as the company behind the contract. That’s why insurer credit ratings matter. Consumers evaluating annuities should pay attention to the issuing company’s financial health, not just the product brochure.

There is also the backstop of state guaranty associations in the U.S., which can provide protection if an insurer fails, subject to state-specific limits and rules. But that protection isn’t a substitute for careful insurer selection. Annuities can be safe tools when issued by financially strong companies and used for the right purpose. They’re less safe when misunderstood, overpriced, or bought without enough liquidity elsewhere in the plan.

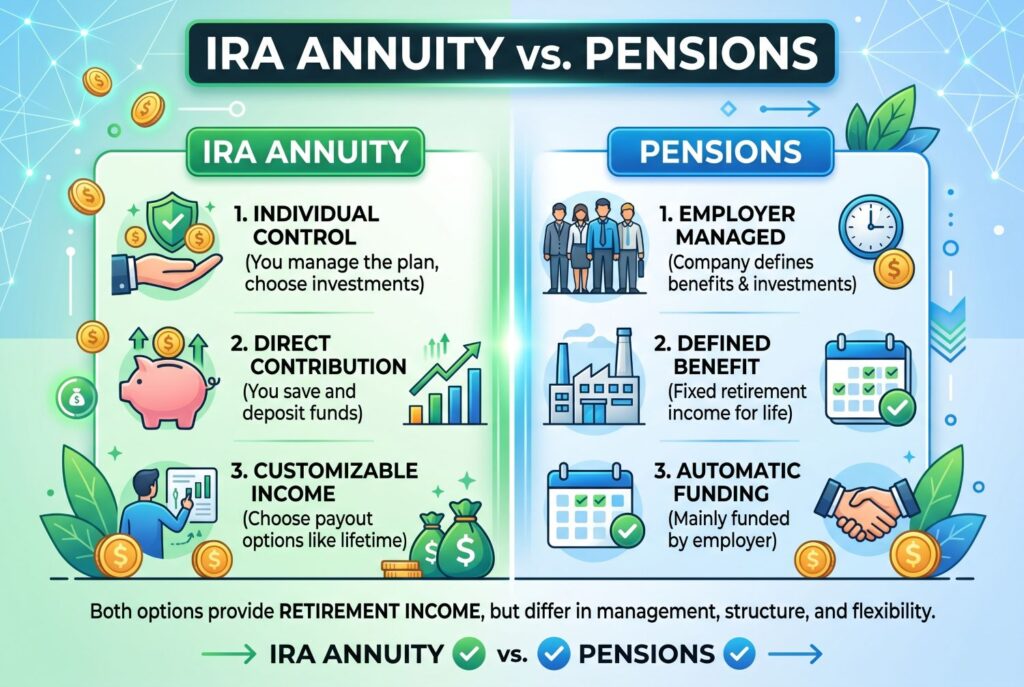

Tying It All Together: IRA Annuity vs. Pensions

An IRA annuity can make sense for someone who wants a portion of retirement assets converted into future income inside an existing retirement framework. But it’s important to remember that annuities inside IRAs don’t create a new tax shelter on top of the IRA. The decision should be based on income planning, not a mistaken idea of getting double tax advantages.

The bigger question is how annuities fit alongside pensions and annuities already in the household income mix. If someone already has a strong traditional pension, Social Security, and stable retirement assets, the need for additional guaranteed income may be lower. If someone has no pension at all, the value of annuitizing part of the portfolio may be much higher.

Decision Matrix: Should You Invest in an Annuity?

Persona A: A single retiree with no pension and a strong fear of running out of money may benefit the most from an annuity, especially one designed to support lifetime income.

Persona B: A couple with stable pensions, strong retirement savings, and a desire to leave a legacy may be less enthusiastic about locking up too much capital in an annuity.

Persona C: A freelancer or self-employed saver without employer pension benefits may use an annuity strategically to create a personal pension-like income stream later in life.

Conclusion

So, are annuities a good investment? They can be, but only when matched to the right person, the right contract, and the right retirement problem. They aren’t universal solutions, and they aren’t automatically bad either. Used thoughtfully, annuities can be strong risk-management tools for people who value guaranteed income, tax deferral, and protection against longevity risk. Used carelessly, they can become expensive, illiquid, and poorly understood commitments.

Before signing anything, review the contract carefully, understand the fees, ask how inflation affects the payout, and evaluate the insurer’s financial strength. That’s how you turn a confusing product category into a more informed retirement decision.