For an independent RIA, wealth management software isn’t just a back office tool. It’s the operating system that determines how fast your firm can grow, how clean your data remains, and how polished the client experience feels. The mistake many advisors make when searching for the best wealth management software is treating every platform as if it solves the same problem. In reality, a modern wealth management platform includes several layers: CRM, portfolio accounting, client reporting, billing, compliance workflows, asset aggregation, and custodian integration. In 2026, the winning tech stack is the one that connects these layers without forcing your team into endless manual cleanup.

Map the Stack: Wealth Management CRM vs. Portfolio Engines

The first step is understanding the difference between a wealth management CRM and a portfolio engine.

A wealth management CRM manages people, relationships, tasks, and workflows. It’s where your team tracks prospect conversations, client notes, onboarding steps, meeting follow ups, document requests, service tickets, compliance tasks, and referral pipelines. For example, if a new client signs an advisory agreement, the CRM should trigger the onboarding checklist, assign internal tasks, request missing documents, and track every communication.

A portfolio accounting and reporting engine does something different. It manages investment data. It’s responsible for performance calculation, account reconciliation, billing, rebalancing support, tax lots, model portfolios, and custodian data feeds.

In simple terms, CRM answers: who is the client and what needs to happen next? Portfolio software answers: what does the client own, how is it performing, and what needs to change? A firm that confuses these two layers often ends up with duplicate data, frustrated advisors, and messy client reports.

The Core Modules Every RIA Should Evaluate

A serious financial advisor software stack should include several core modules.

- First, client onboarding. The system should collect documents, manage e signatures, track account openings, and reduce back and forth emails.

- Second, portfolio reporting. Clients expect clean performance reports, household level summaries, allocation breakdowns, benchmark comparisons, and fee transparency.

- Third, billing. Advisory fees should calculate accurately based on your billing schedule, AUM tiers, household rules, exclusions, and account level details.

- Fourth, rebalancing. Even if your firm doesn’t trade daily, you need tools that identify drift, support tax aware decisions, and reduce manual spreadsheet work.

- Fifth, compliance documentation. Your system should preserve notes, approvals, correspondence, and required records so audits don’t become chaos.

The best wealth management software doesn’t only store information. It removes operational friction.

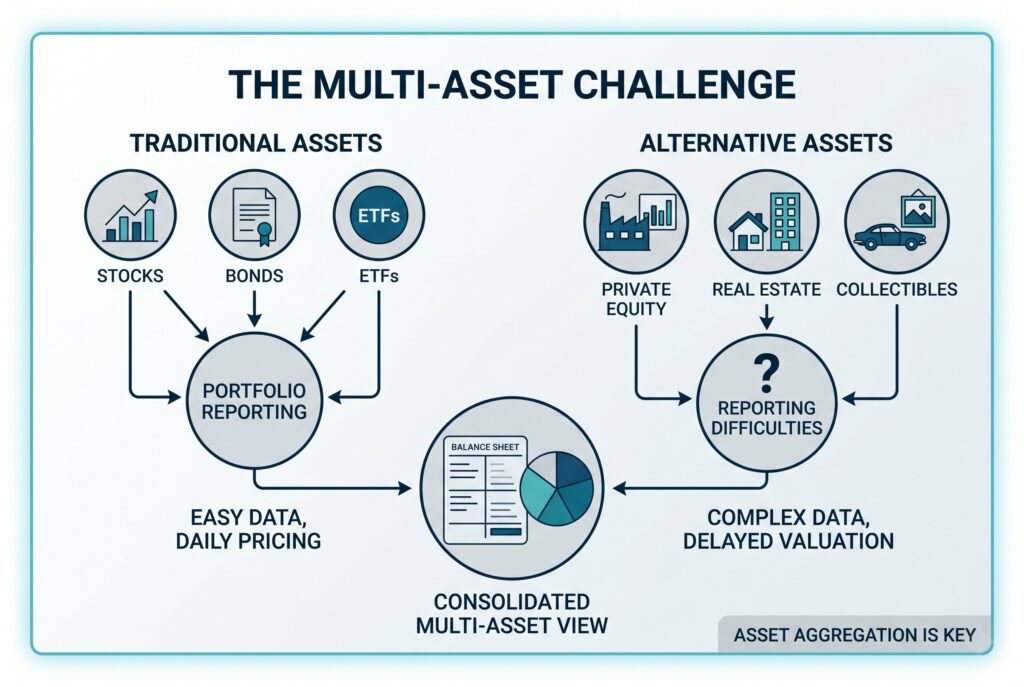

The Multi Asset Challenge: Going Beyond Public Equities

Wealth management software 2026 must handle more than stocks, bonds, mutual funds, and ETFs.

High net worth clients increasingly hold private equity, real estate, private credit, hedge funds, concentrated stock, business interests, crypto exposure, collectibles, and other alternatives. That creates a reporting challenge.

Traditional portfolio systems were designed for liquid marketable securities. Alternative assets don’t always have daily pricing, clean data feeds, or standardized cash flow reporting. Capital calls, distributions, delayed valuations, K 1 tax documents, and complex ownership structures make reporting difficult.

This is where asset aggregation becomes essential. A strong platform should consolidate public market accounts, held away assets, private investments, real estate holdings, and liabilities into one coherent balance sheet. For family office software, this multi asset view isn’t optional. It’s the core value proposition. If your team still enters private investment values manually every month, the software isn’t truly scaling with your clients.

Custodian Integration: The Sourcing Pipeline

Custodian integration is one of the most important parts of any asset management solutions stack. An RIA’s portfolio engine should connect cleanly with major custodians through reliable data feeds or APIs. Daily transaction data, dividends, holdings, cash balances, market values, and cost basis information should flow automatically into the reporting system.

The goal is overnight reconciliation. When advisors open the platform in the morning, client portfolios should already reflect the latest available data. Poor integrations create hidden costs. Your operations team spends hours correcting missing trades, duplicate transactions, stale prices, broken tax lots, and mismatched household values.

Before choosing software, ask vendors exactly how they connect to your custodians. Native integration is usually better than a fragile workaround. Also ask how exceptions are flagged and resolved. Clean data isn’t a luxury. It’s the foundation of trustworthy advice.

Client Portal Experience: The Digital Front Door

Clients judge your firm partly through your portal. A strong wealth management platform should give clients secure access to net worth, performance, documents, messages, financial plans, and reports.

The portal should feel simple, not overwhelming. Clients don’t want to decode institutional software. They want a clean dashboard that answers basic questions quickly:

- How much do I have?

- How am I doing?

- Where is my money invested?

- What documents need my attention?

Security matters too. Look for two factor authentication, role based access, encryption, audit trails, and strong permission controls. A beautiful portal that isn’t secure isn’t acceptable in modern advisory work.

Buy the Stack, Not the Logo

It’s tempting to choose the most famous software name in the market. That can be a mistake.

The right wealth management software depends on firm size, client complexity, asset mix, service model, compliance burden, and growth plan. A solo advisor may need a simple CRM, reporting tool, and planning platform. A multi advisor RIA may need stronger workflow automation, billing, model management, and custodian reconciliation.

A family office may need deep asset aggregation, entity reporting, private investment tracking, document management, and multi generational reporting. Don’t buy features you won’t use. But don’t underbuy if your clients are becoming more complex.

Conclusion

In 2026, technology isn’t an administrative expense for independent RIAs. It’s a strategic asset. The right wealth management software reduces manual work, improves data quality, strengthens compliance, and creates a better client experience. The wrong platform creates operational drag that becomes harder to fix as AUM grows.

Start by mapping your stack. Separate CRM from portfolio accounting. Evaluate asset aggregation honestly. Test custodian integrations carefully. Review portal security. Ask hard questions about migration, pricing, and support. The best platform isn’t the one with the longest feature list. It’s the one that fits your firm’s workflow, your clients’ complexity, and your long term growth plan.