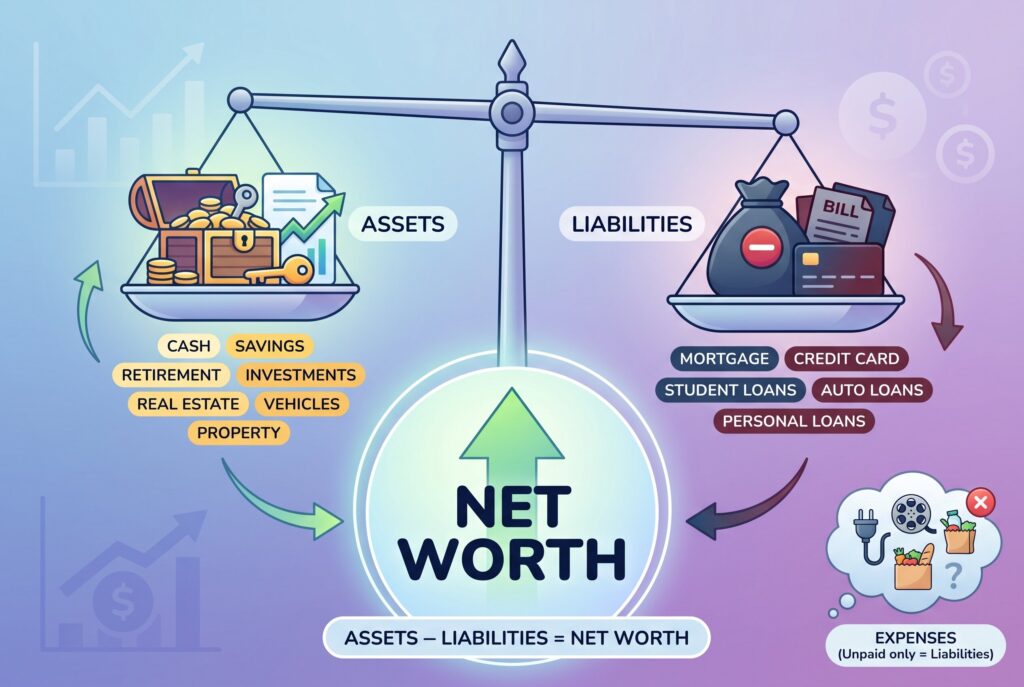

Net worth is the total value of what you own minus what you owe. In simple terms, it is your assets minus your liabilities. It isn’t your monthly income, your checking account balance, or how expensive your lifestyle looks from the outside. It is a financial snapshot that shows where you stand at one point in time.

So, what is net worth in real life? If your assets add up to $250,000 and your liabilities total $180,000, your net worth is $70,000. If your debts are higher than your assets, your net worth is negative. That may sound discouraging, but it isn’t a permanent label. It is simply a starting point. A net worth statement helps you see the full story: your savings, investments, home equity, car value, mortgage, loans, credit card debt, and other obligations in one place.

Interactive Tool: What’s My Net Worth?

What’s My Net Worth?

Use this calculator to build a simple personal balance sheet. Add what you own, subtract what you owe, and see your estimated net worth instantly.

Assets

Liabilities

Net Worth = Total Assets − Total Liabilities

Total Assets = Cash + Retirement Accounts + Brokerage Account + Car Value + Home Value + Other Assets

Total Liabilities = Mortgage + Student Loans + Credit Card Debt + Car Loan + Personal Loans + Other Liabilities

Note: Your net worth estimate does not need to be perfect down to the dollar. The goal is to create a useful personal balance sheet and update it regularly to see whether your financial life is moving in the right direction.

To calculate your net worth, use this simple formula:

Net Worth = Total Assets − Total Liabilities

A basic net worth statement has two columns. On one side, list everything you own. On the other, list everything you owe. Then subtract liabilities from assets.

Example:

- Cash and savings: $12,000

- Retirement accounts: $45,000

- Brokerage account: $8,000

- Car value: $15,000

- Home value: $300,000

Total assets: $380,000

- Mortgage: $240,000

- Student loans: $18,000

- Credit card debt: $4,000

- Car loan: $9,000

Total liabilities: $271,000

Net worth: $109,000

This number doesn’t need to be perfect down to the dollar. Your goal is to build a useful personal balance sheet, not an accounting textbook. Update your estimates regularly, and you will see whether your financial life is moving in the right direction.

How Are Assets and Liabilities Connected to Net Worth?

Assets and liabilities are connected to net worth because they are the two sides of the equation. Assets increase net worth. Liabilities reduce it.

Assets include things you own that have financial value. Common examples include cash, emergency savings, checking accounts, savings accounts, retirement accounts, investment accounts, real estate, vehicles, business ownership, and valuable personal property. Liabilities include money you owe. These may include a mortgage, credit card debt, student loans, auto loans, personal loans, medical debt, back taxes, and other unpaid obligations.

One important point: normal monthly bills aren't always liabilities. Your electric bill, streaming subscription, groceries, and rent are expenses. They only become liabilities if they are unpaid and owed. This distinction matters because confusing expenses with liabilities can make your net worth statement messy and inaccurate. The cleanest way to think about it is this: assets are what you could sell, use, or convert into value. Liabilities are what someone else has a legal claim on.

Average vs. Median: Understanding Net Worth by Age

After people calculate their number, the next question is usually: “Is my net worth good?” That is where average net worth by age, median net worth by age, and net worth by age percentile become useful. But before comparing yourself, you need to understand median vs average.

Average net worth is calculated by adding everyone’s net worth together and dividing by the number of people. The problem is that a small number of very wealthy households can pull the average much higher. Median net worth is different. It shows the middle point. Half of households have more, and half have less. For most people, median net worth by age is a more realistic comparison than average net worth by age. For example, the average net worth of people in their 30s may look impressive because high earners, business owners, and early investors raise the number. But the median may show a more normal picture for someone still paying off student loans, building emergency savings, or saving for a first home.

That is why average vs median matters. Average tells you what the math looks like when wealth is spread across everyone. Median tells you what the typical household looks like. A person in their 20s often has a low or negative net worth because they are early in their career and may still carry student debt. Someone in their 30s may begin building retirement savings, home equity, and investment accounts. By the 40s and 50s, net worth often grows faster because income is higher, debt may fall, and compound growth has had more time to work. Still, net worth by age percentile should be used carefully. Your city, income, family obligations, health, career path, and debt history all affect your number. The goal is to understand your trajectory.

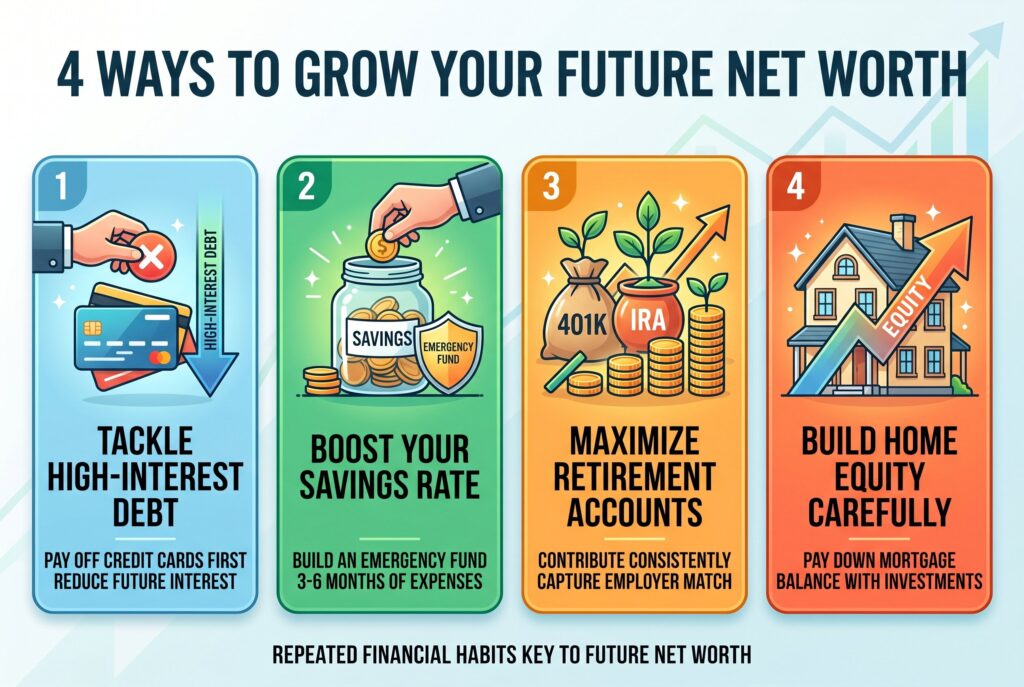

4 Ways to Grow Your Future Net Worth

Your future net worth depends less on one lucky move and more on repeated financial habits. Here are four practical ways to improve it.

Tackle High-Interest Debt First

Credit card debt can quietly destroy progress because interest grows faster than most safe investments. Paying down high-interest debt gives you a guaranteed return by reducing future interest.

Boost Your Savings Rate

If you wonder how much you should have in savings, start with an emergency fund of three to six months of essential expenses. This gives you breathing room when life breaks your budget.

Maximize Retirement Accounts

Contribute consistently, capture any employer match, and increase your contribution rate when your income rises.

Build Home Equity Carefully

Home equity can increase net worth over time as you pay down your mortgage and your property value changes. But a home isn't automatically wealthy if the payment leaves you cash-poor. Balance homeownership with savings, investments, and liquidity.

Conclusion

Your net worth isn’t a reflection of your personal value. It doesn’t determine whether you are successful or unsuccessful. Instead, it is simply a snapshot of where you stand financially today. The key isn’t whether your net worth is positive right now. What matters most is whether it is moving in the right direction over time. Are you building assets, reducing debt, saving more, and making better financial decisions than you were a year ago?

Rather than focusing on short-term market fluctuations, review your net worth periodically, such as once a quarter or once a year. Looking at long-term trends will give you a much clearer picture of your financial progress. Understanding your net worth can help you make smarter decisions about budgeting, debt repayment, saving, investing, and retirement planning. Think of your net worth statement as a map that shows where you’re today. The financial habits you practice every day will determine where that map leads you in the future.