")

If you’re a contractor, business owner, property manager, or vendor, sooner or later someone will ask you to sign a waiver of subrogation clause. At first glance, it may seem like just another piece of legal paperwork. In reality, it’s one of the most important risk transfer provisions you’ll encounter.

What Is a Waiver of Subrogation?

In plain English, it’s an agreement that prevents your insurance company from pursuing another party for reimbursement after paying a covered claim. The waiver of subrogation meaning is essentially a prearranged peace treaty between business partners. Instead of allowing insurers to sue each other after an accident, both parties agree in advance to let insurance handle the loss without triggering costly litigation.

This approach helps preserve long term business relationships, reduces legal expenses, and prevents disputes from escalating into years of courtroom battles. However, signing a waiver without understanding how it affects your insurance policy can expose your business to significant risk in 2026.

Why Businesses Use Waiver of Subrogation Agreements

To understand why these agreements exist, it helps to first understand subrogation.

Normally, when an insurer pays a claim, it gains the right to seek reimbursement from the party responsible for the damage. This recovery process helps insurers reduce losses and keep claim costs under control. A waiver of subrogation removes that right.

Imagine a landlord and tenant operating in the same building. A fire damages part of the property. The landlord’s insurance company pays the claim. Without a waiver, the insurer may investigate and sue the tenant if the tenant contributed to the loss.

With a waiver in place, that lawsuit typically doesn’t happen. The insurer pays the claim, the business relationship survives, and both parties avoid expensive legal conflict. This is why waiver of subrogation insurance requirements appear so frequently in commercial leases, construction contracts, vendor agreements, and property management arrangements.

The Hidden Risk: Policy vs Contract Conflict

This is where many businesses make a costly mistake. They sign a contract containing a waiver of subrogation without checking whether their insurance policy allows it. Most insurance policies contain language protecting the insurer’s recovery rights. After all, subrogation helps insurers recover money when someone else caused the damage.

If you sign away those rights without insurer approval, you may create a direct conflict between your contract and your insurance policy.

Consider this example:

A contractor signs a construction agreement containing a waiver of subrogation clause. Months later, a major property loss occurs. The insurer discovers that the contractor waived recovery rights without obtaining the required endorsement. The insurer may argue that policy conditions were violated. In some situations, this can create coverage disputes, claim delays, or even claim denials. That’s why every waiver should be reviewed alongside the actual insurance policy, not just the contract.

The COI Illusion: Why a Certificate Is Never Enough

Many risk managers and compliance teams rely heavily on certificates of insurance. That creates another common trap. Suppose a subcontractor provides a certificate of insurance stating that waiver of subrogation applies. Most people assume the requirement has been satisfied. Not necessarily. A certificate of insurance is only a summary document. It doesn’t change policy language. It doesn’t create coverage. It doesn’t automatically grant endorsements. The actual authority comes from the policy endorsement issued by the insurance company.

If you’re reviewing vendor insurance requirements, always request a copy of the endorsement itself. Don’t rely exclusively on the certificate. The endorsement is the legal document proving that the insurer has agreed to waive its recovery rights. Without that endorsement, the certificate alone may provide little protection.

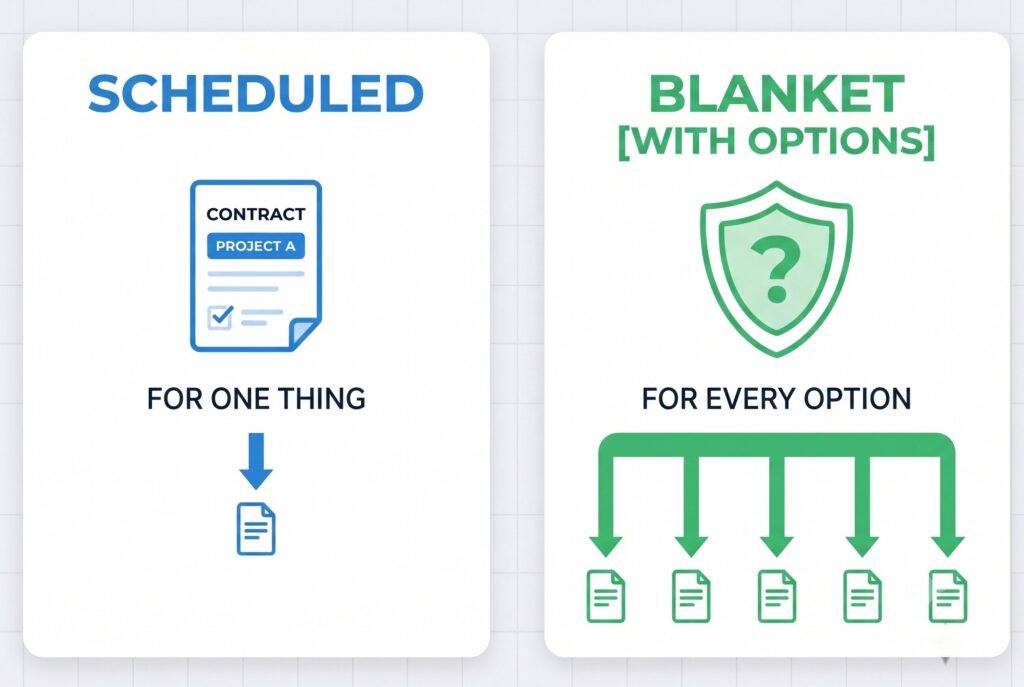

Blanket vs Scheduled Waivers: Which Option Makes Sense?

Insurance companies often offer two types of waiver arrangements.

Scheduled Waiver

A scheduled waiver applies only to a specifically identified person, company, project, or contract. For example, a contractor working on a single office building project may request a waiver that applies only to that project owner. This approach works well when waiver requests are infrequent.

Blanket Waiver

A blanket waiver automatically applies whenever a written contract requires it. Instead of requesting individual endorsements repeatedly, the waiver extends across multiple projects and business relationships. For companies operating in construction, maintenance, logistics, staffing, or commercial services, a blanket waiver can save substantial administrative time. It also reduces the risk of accidentally forgetting to request a new endorsement for each contract.

Workers Compensation Waiver of Subrogation

One of the most frequently requested endorsements involves workers compensation waiver of subrogation coverage. Construction projects provide a perfect example. Suppose a subcontractor’s employee suffers an injury while working on a job site. The subcontractor’s workers’ compensation insurance pays medical costs and wage replacement benefits.

Without a waiver, the workers’ compensation insurer may later pursue the project owner, developer, or general contractor if they contributed to the accident. With a workers compensation waiver of subrogation endorsement in place, that recovery action generally can’t occur.

Project owners often require this protection because it helps prevent lawsuits among project participants. Everyone can focus on completing the project instead of fighting over reimbursement claims. This is one reason workers compensation waiver of subrogation requirements are extremely common throughout the construction industry.

Is a Waiver Always a Good Idea?

Not necessarily. A waiver provides benefits, but it also involves tradeoffs. The party receiving the waiver gains protection because the insurer can’t pursue reimbursement. The party granting the waiver gives up potential recovery rights. Some insurers charge additional premium for these endorsements. Others include certain waivers automatically within policy forms.

The decision should depend on the value of the contract, the nature of the relationship, the insurance requirements involved, and the level of risk being transferred. It’s also important to remember that waiver of subrogation isn’t the same thing as additional insured status. These terms frequently appear together, but they serve different purposes. Additional insured coverage extends certain liability protections. A waiver of subrogation limits post claim recovery rights. Both may be required in the same contract, but they accomplish different goals.

Conclusion

Understanding waiver of subrogation insurance isn’t simply about learning a legal definition. It’s about protecting cash flow, preserving insurance coverage, and managing business risk intelligently. The purpose of a waiver is straightforward. It allows business partners to avoid litigation and maintain productive relationships after a covered loss. But the endorsement must be handled properly.

Never assume a contract requirement automatically aligns with your insurance policy. Never assume a certificate of insurance is enough. And never sign away insurer recovery rights without confirming that the proper endorsement exists.

The smartest businesses treat waiver of subrogation review as part of every contract negotiation. A few minutes of verification today can prevent expensive disputes, coverage problems, and unexpected liabilities tomorrow.

Related Articles

What Is Subrogation in Insurance? (Claim Examples & Your Deductible)