? 3 Costly Mistakes to Avoid")

Running a business often means proving you have the right insurance before work can begin. Clients, landlords, vendors, and business partners may ask for documentation showing that coverage is in place before signing contracts or approving projects.

Without the proper paperwork, deals can be delayed, payments can be held up, and opportunities can be lost. That is why understanding certificates of insurance is important for businesses of all sizes. Knowing what information they provide, when they are required, and how to obtain one can help you avoid unnecessary complications and keep business moving forward.

What Is a Certificate of Insurance (COI)?

A Certificate of Insurance (COI) is a document issued by an insurance company or broker that summarizes a business’s insurance coverage. It provides proof that an active insurance policy is in place and outlines key details such as coverage types, policy limits, and effective dates. Clients, landlords, and business partners often request a COI before signing contracts or starting work. While the certificate verifies coverage, it doesn’t replace or modify the actual insurance policy.

What Is a COI in Business?

In business, a COI is used as proof of insurance before work begins. A property manager may ask a cleaning company for one. A general contractor may require every subcontractor to provide one before entering a jobsite. A landlord may request one from a tenant. A venue may ask an event vendor to prove coverage before setting up.

The purpose is risk control. If a vendor causes property damage, injures someone, or creates a liability claim, the hiring company wants confirmation that insurance exists to respond.

A COI usually includes the named insured, insurance carrier, producer or broker, policy number, coverage types, effective dates, expiration dates, limits, certificate holder, and sometimes special wording such as additional insured or waiver of subrogation.

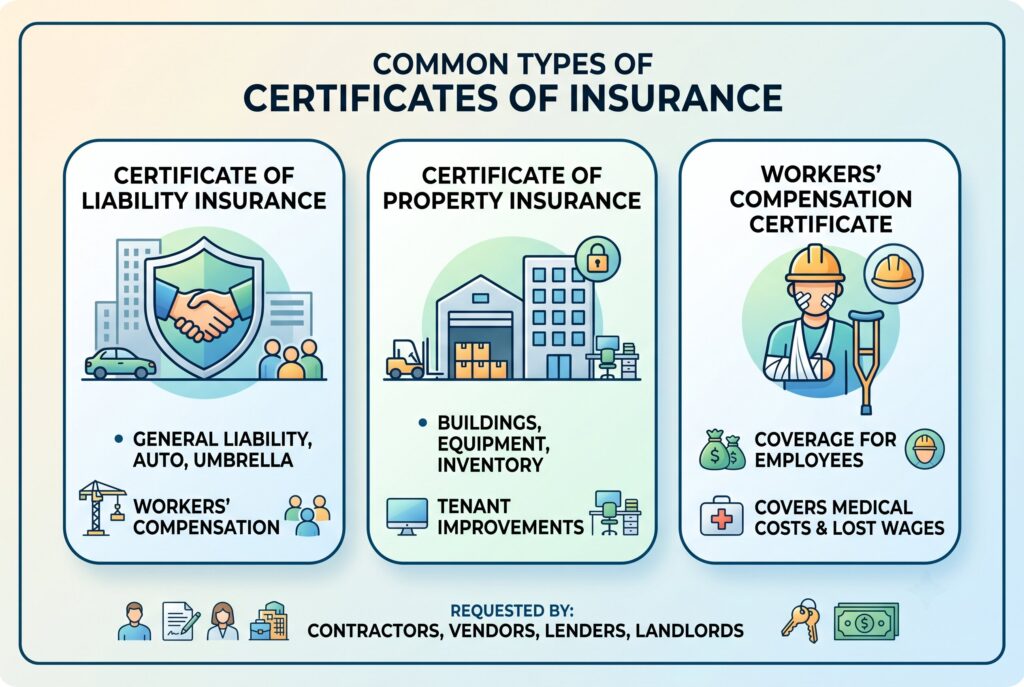

Common Types of Certificates of Insurance

1. Certificate of Liability Insurance

The certificate of liability insurance is the most common business COI. In many cases, it appears on an ACORD 25 form. It summarizes liability coverage such as general liability, auto liability, umbrella liability, and workers’ compensation. Contractors, vendors, consultants, janitorial companies, repair crews, and event providers are often asked to provide this document.

2. Certificate of Property Insurance

A certificate of property insurance proves that physical property is insured. This may include buildings, equipment, inventory, tenant improvements, or business personal property. Lenders, landlords, and investors may request it to confirm that valuable assets are protected.

3. Workers’ Compensation Certificate

This certificate shows that a business carries workers’ compensation coverage for employees. It matters because if a worker is injured on the job, the policy may cover medical costs and lost wages. Construction projects, staffing contracts, and facility services often require this proof before work begins.

How to Read a Certificate of Insurance

Start with the named insured. The legal name on the COI should match the company named in your contract. If the contract says “ABC Electrical Services LLC” but the COI says “ABC Electric,” don’t assume they’re the same entity.

Next, check policy dates. Coverage must be active during the full work period. A policy that expires next week doesn’t protect you for a six month project unless renewal is tracked.

Then check limits. If your contract requires $1 million per occurrence and $2 million aggregate general liability coverage, the COI should match or exceed those amounts.

Finally, review the certificate holder section. If you’re the party requesting proof, your correct legal name and address should appear there.

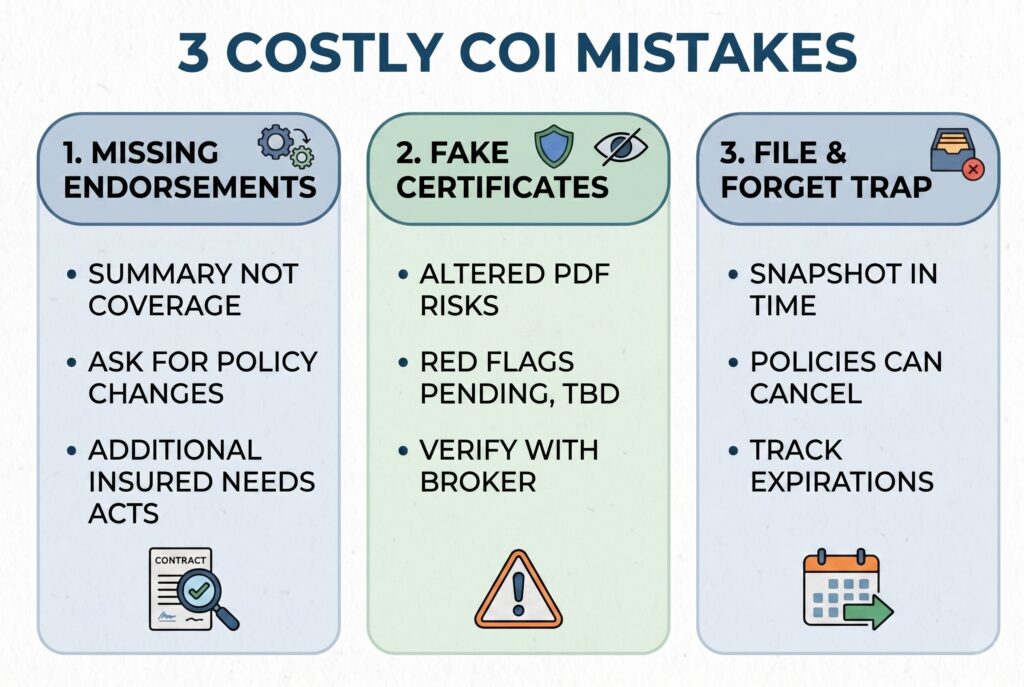

3 Costly Mistakes to Avoid When Reviewing a Certificate of Insurance for Business

Mistake 1: Accepting a COI Without Policy Endorsements

This is the mistake that creates the biggest false sense of security. A vendor may send a certificate showing you as an additional insured. You file it away and assume you’re protected. But the COI itself doesn’t amend the insurance policy. If the insurer didn’t issue the actual policy endorsement, the wording on the certificate may not give you the protection you expected.

The same issue applies to waiver of subrogation, primary and noncontributory wording, or special contract requirements. These items often require endorsements. A certificate may reference them, but you should ask for the endorsement when the contract requires real coverage changes. In short, don’t confuse a summary document with legal coverage.

Mistake 2: Falling for Fake or Altered Certificates of Insurance

Fake certificates of insurance are a real business risk. A contractor may edit a PDF to change expiration dates, raise limits, or hide a canceled policy.

Common red flags include policy numbers marked “pending,” “TBD,” or “quote.” Other warning signs include mismatched company names, blurry formatting, missing insurer details, outdated policy dates, limits below contract requirements, or certificate wording that seems unusually vague.

The safest verification method is to contact the insurance broker or carrier listed on the certificate. Don’t rely only on a forwarded PDF from the vendor. If the project is high value, verification isn’t optional. It’s part of vendor compliance.

Mistake 3: The File and Forget Trap

A COI is only a snapshot in time. It proves coverage existed when the certificate was issued, but it doesn’t guarantee the policy will remain active forever. A vendor could cancel coverage, fail to pay premiums, reduce limits, change insurers, or let the policy expire.

This is why businesses that manage many vendors need renewal tracking. If you collect certificates of insurance once and never review them again, your records may become useless within months. A proper compliance workflow should track expiration dates, request updated certificates before renewal, verify limits again, and confirm endorsements didn’t disappear.

Certificate Holder vs Additional Insured

These two terms are often confused. A certificate holder is the person or business receiving the COI. It means the document was issued to you for informational purposes. Additional insured status is different. It may extend certain policy protections to your business under another party’s policy. Being listed as a certificate holder doesn’t automatically make you an additional insured. If your contract requires additional insured status, request the endorsement, not just the COI.

Why COIs Matter for Vendor Compliance

Certificates of insurance help businesses reduce risk before it becomes a claim. They create a paper trail showing that vendors, tenants, subcontractors, and service providers carried required coverage.

For a small business, a COI can help win contracts. For a property manager, it can protect buildings and tenants. For a general contractor, it can reduce project risk. For a large company, it can support procurement, legal review, and audit readiness. But a weak COI process can be worse than no process because it creates confidence without real protection.

Conclusion

Knowing “what is a COI” is only the beginning. A certificate of insurance is useful because it gives a fast summary of active coverage, but it isn’t the policy itself. It doesn’t guarantee coverage changes, doesn’t replace endorsements, and doesn’t protect you from fraud or expired policies.

The safest approach is to request and review the COI before work begins. Make sure the names, dates, coverage limits, and contract requirements match. If anything looks questionable, verify the information directly with the insurance broker or carrier. A COI is a valuable risk management tool, but only when it is properly reviewed.