If you aren’t sure what a COI is, start with this simple idea: a certificate of insurance is proof that a business has active insurance coverage. A certificate of liability insurance goes one step deeper. It shows that your business carries liability coverage, usually general liability insurance, and summarizes the key policy details a client, landlord, venue, or contractor needs before working with you.

For contractors, freelancers, consultants, vendors, and tech companies, this document can be the difference between winning a contract and losing the job. It’s commonly issued on an ACORD 25 form and shows your policy limits, coverage dates, insurer, insured business name, and certificate holder. It’s the full insurance policy, but it’s the fastest way to prove you’re protected.

What Does a Certificate of Liability Actually Cover?

When someone asks for a certificate of insurance for business, they’re usually trying to confirm that your company has general liability insurance. This coverage is designed to protect against common third party claims.

Bodily Injury Coverage

General liability insurance helps protect a business when a customer, visitor, or client suffers a physical injury due to business operations. For example, a customer may slip on a wet floor, trip over equipment, or get injured while visiting a business location. In these situations, the policy may help cover medical expenses, legal defense costs, and potential settlements.

Property Damage Coverage

General liability insurance may also cover damage caused to someone else’s property. This can occur when an employee accidentally damages a client’s equipment, breaks fixtures during installation work, or causes harm to rented premises. Coverage may help pay for repair or replacement costs as well as related legal expenses.

Personal and Advertising Injury Coverage

Another key protection involves personal and advertising injury claims. These claims can arise from business communications, marketing campaigns, or advertising activities. Examples include allegations of defamation, copyright infringement in advertisements, or reputational harm caused by published business content. General liability insurance may help cover legal defense costs and settlement expenses associated with these claims.

The certificate itself won’t pay claims. It simply proves that the policy exists and shows the coverage limits. A common requirement is $1 million per occurrence and $2 million aggregate, meaning the insurer may pay up to $1 million for one covered incident and $2 million total during the policy term.

Does a Certificate of Insurance Cost Money in 2026?

Many business owners mistakenly believe they are paying for a Certificate of Liability Insurance (COI). In reality, the certificate itself is usually provided at no additional cost. Once a business purchases a liability insurance policy, the insurer, broker, or insurance platform can typically issue certificates for free. Many providers also allow policyholders to download, email, or generate certificates instantly through an online portal.

The actual expense comes from the liability insurance policy that supports the certificate. For many low risk small businesses, general liability insurance may cost approximately $40 to $100 per month. Freelancers, consultants, and office based businesses are often on the lower end of that range. Businesses with greater liability exposure, including contractors, cleaning companies, installers, repair services, and event related businesses, generally pay higher premiums.

The cost of liability insurance depends on several factors, including the type of business, annual revenue, location, claims history, number of employees, and chosen coverage limits. The key point is simple: while a Certificate of Liability Insurance is usually free, it can only be issued when an active liability insurance policy is in place.

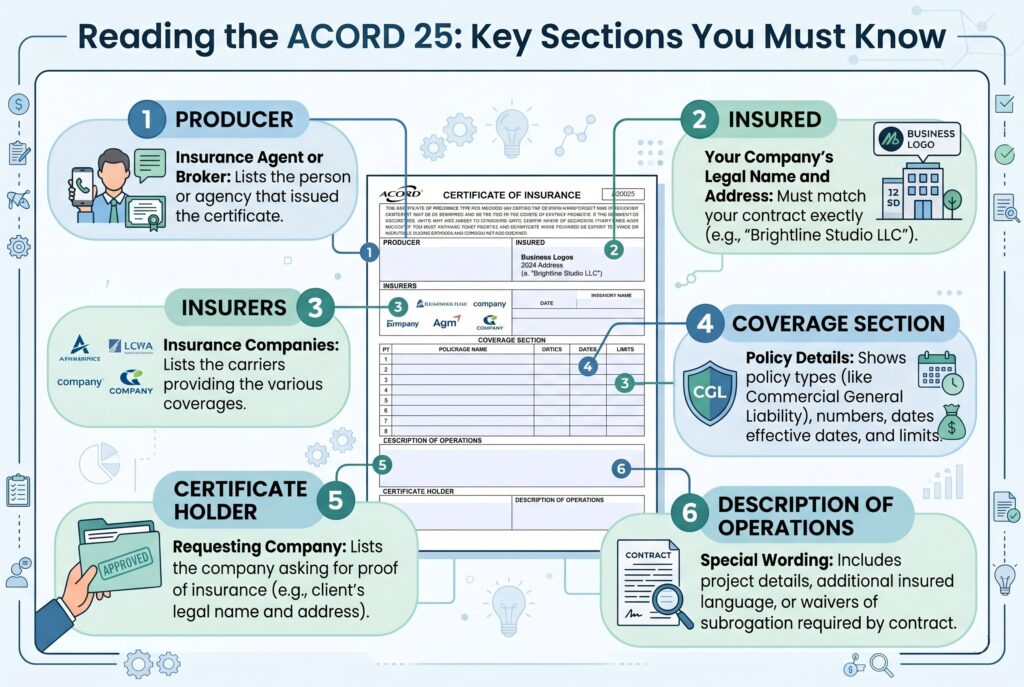

Reading the ACORD 25: Key Sections You Must Know

Most certificate of liability insurance documents are issued using the ACORD 25 form. It looks technical, but the main sections are straightforward. The producer section lists the insurance agent or broker. This is the person or agency that issued the certificate.

The insured section shows your company’s legal name and address. This must match your contract. If your contract is with “Brightline Studio LLC,” but the COI says “Brightline Design,” the client may reject it.

The insurers section lists the insurance companies providing coverage. The coverage section shows policy types, limits, effective dates, expiration dates, and policy numbers. For liability proof, the client will usually look for commercial general liability.

The certificate holder section lists the company requesting proof of insurance. If a client asks to be listed, their legal name and address must appear correctly. The description of the operations section may include special wording required by the contract, such as project location, job description, additional insured language, or waiver of subrogation wording.

Additional Insured: Why Clients Ask for It

Being named certificate holder isn’t the same as being additional insured. A certificate holder receives proof of coverage. That’s informational.

Additional insured status may extend certain protections under your liability policy to the client or project owner. For example, if a third party sues both you and your client because of your work, additional insured status may help protect the client under your policy. This request is common in construction, property management, events, commercial leases, and vendor contracts.

But there’s one critical warning: the COI alone usually doesn’t create additional insured coverage. The insurer often must issue a policy endorsement. If a client requires additional insured status, ask your broker to provide the endorsement, not just a certificate with wording typed into the description box.

Certificate of Liability Insurance vs Other COIs

A Certificate of Liability Insurance (COI) is only one type of insurance certificate. Different certificates are used to verify different types of coverage, depending on the requirements of a contract or business relationship.

| Certificate Type | What It Proves | Common Users |

| General Liability Certificate | Coverage for third party bodily injury, property damage, and personal or advertising injury claims | Most businesses, contractors, vendors, and service providers |

| Property Insurance Certificate | Coverage for physical assets such as buildings, equipment, furniture, and inventory | Property owners, retailers, manufacturers, and warehouse operators |

| Workers’ Compensation Certificate | Coverage for employee work related injuries and illnesses | Businesses with employees, especially in construction, manufacturing, and transportation |

| Professional Liability Certificate | Coverage for service errors, negligence claims, omissions, or professional mistakes | Consultants, accountants, architects, engineers, software vendors, and technology companies |

| Cyber Liability Certificate | Coverage for data breaches, cyberattacks, privacy violations, and related liability claims | Businesses that handle sensitive customer information or integrate with enterprise systems |

The right certificate depends on the specific requirements outlined in a contract. A client may request proof of professional liability or cyber liability coverage rather than general liability coverage. Always review the contract carefully and provide the certificate that matches the requested insurance type.

Common Mistakes That Delay Contracts

- The first mistake is sending an expired certificate. Clients care about active policy dates.

- The second mistake is using the wrong business name. The legal insured name must match the contract.

- The third mistake is missing the certificate holder. Many clients reject certificates that don’t list them correctly.

- The fourth mistake is showing limits below the contract requirement. If the agreement requires $2 million in coverage and your policy shows $1 million, the job may be delayed.

- The fifth mistake is assuming the COI changes the policy. It doesn’t. Endorsements control real coverage changes.

Conclusion

Understanding COI meaning is useful, but having a certificate ready is even more important. In business, clients don’t want promises. They want proof. A certificate of liability insurance shows that your company has active liability coverage and can meet basic contract requirements.

The document itself is usually free once your policy is active, but the policy behind it must be strong enough for the work you perform. Review your limits, coverage type, legal business name, certificate holder details, and endorsement requirements before sending anything to a client. A clean certificate of insurance can help you sign leases, book venues, satisfy landlords, win projects, and build trust faster. In a competitive market, the business that provides proof quickly often gets the contract first.