Inherent risk is the baseline level of risk that exists in a process, transaction, system, or business activity before any controls or mitigation steps are applied. In simple terms, it’s an untreated risk. If your company did nothing to prevent fraud, cyberattacks, vendor failure, reporting errors, or operational disruption, the exposure that remains is inherent risk.

In auditing, inherent risk refers to the possibility of material misstatement in financial statements before considering internal controls. In GRC, it helps risk managers understand the raw danger behind a decision before safeguards are added. You can’t manage what you haven’t measured, which is why identifying inherent risk is the first step in any serious risk assessment.

The Risk Equation: Inherent Risk vs. Residual Risk

Many teams confuse inherent risk, residual risk, and control risk. The easiest way to understand them is to think in sequence.

Inherent risk is the original exposure before action. It exists because a process is complex, valuable, sensitive, regulated, or vulnerable by nature. A company storing customer payment data has inherent cyber risk even before anyone evaluates its firewalls or access controls.

Control effectiveness refers to the strength of safeguards used to reduce that exposure. These controls may include approval workflows, encryption, segregation of duties, vendor reviews, insurance, monitoring software, or employee training.

Residual risk is the risk left after controls are applied. The basic equation is:

Residual Risk = Inherent Risk − Control Effectiveness

For example, a vendor with access to your internal network may carry high inherent risk. After security questionnaires, contract clauses, access limits, and continuous monitoring are applied, the residual risk may fall to a manageable level.

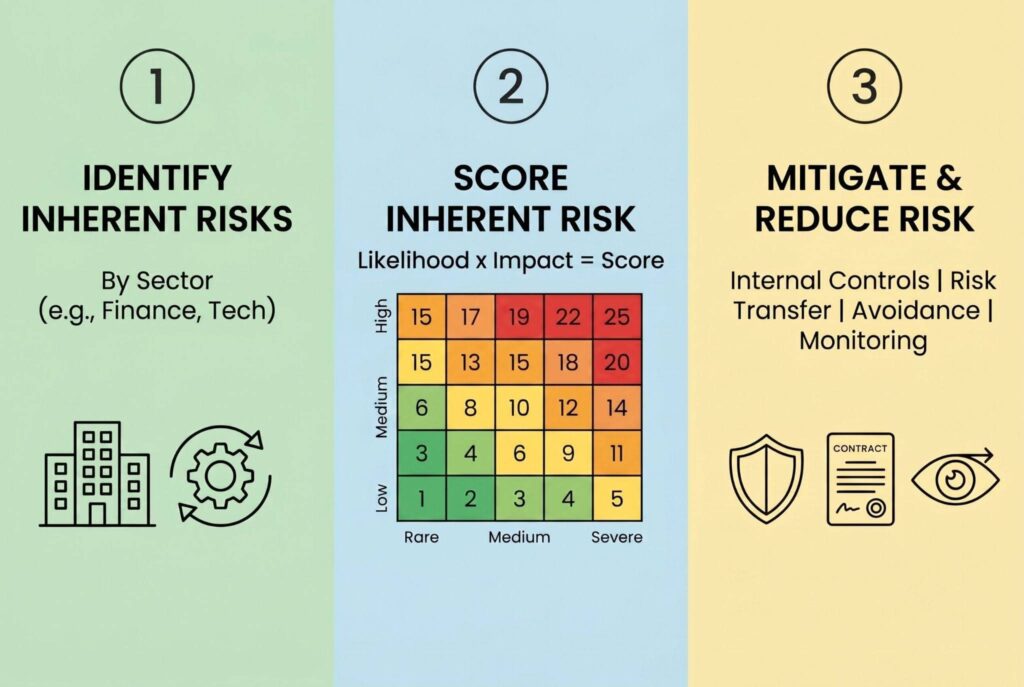

Step 1: How to Identify Inherent Risks by Sector

Inherent risk isn’t the same in every industry. The first step is to identify where the raw exposure naturally appears.

Inherent Risk in Finance and Auditing

In finance and auditing, inherent risk is often associated with complex accounting estimates, revenue recognition, mergers and acquisitions, derivatives, related-party transactions, and manual reporting processes. These activities involve significant judgment, complexity, or large financial values, increasing the likelihood of material misstatements.

Inherent Risk in Cybersecurity and Technology

In cybersecurity, inherent risk arises from assets and activities that naturally attract threats, such as cloud environments, sensitive customer data, public-facing applications, remote access systems, and privileged accounts. These areas can create significant exposure even before security controls are evaluated.

Inherent Risk in Vendor Risk Management

Third-party relationships can introduce substantial inherent risk when vendors access company data, connect to internal systems, support critical operations, or handle regulated information. Common examples include cloud providers, payroll processors, payment service providers, and outsourced IT partners.

Inherent Risk in Operations and Supply Chains

Operational inherent risk stems from factors such as supply chain dependencies, aging equipment, workplace safety hazards, product quality issues, and reliance on key suppliers. These risks are often embedded in the organization’s day-to-day operations and business model.

Step 2: How to Score It With a 5×5 Matrix

Scoring inherent risk shouldn’t be based on instinct alone. A practical risk assessment uses two core variables: likelihood and impact.

Likelihood measures how probable the event is. Impact measures how severe the damage would be if it happened. Each can be scored from 1 to 5.

A simple 5×5 risk matrix works like this:

Likelihood 1 means rare. Likelihood 5 means almost certain.

Impact 1 means minor disruption. Impact 5 means severe financial, legal, operational, or reputational damage.

The score is calculated as:

Likelihood x Impact = Inherent Risk Score

A risk with likelihood 4 and impact 5 receives a score of 20. That belongs in the red zone and needs executive attention before the project moves forward.

A score between 1 and 5 is usually low. A score between 6 and 14 is moderate. A score between 15 and 25 is high. High scores don’t always mean the activity must stop, but they do mean the organization needs strong controls, clear ownership, and documented risk acceptance.

Step 3: How to Mitigate and Reduce Inherent Risk

You can’t eliminate every risk, but you can reduce exposure through better design, stronger controls, and smarter decisions.

Strengthen Internal Controls

Organizations can reduce inherent risk by implementing strong internal controls such as segregation of duties, approval workflows, access restrictions, encryption, audit trails, and automated monitoring. These measures help prevent errors, fraud, and unauthorized activities.

Transfer Risk to Third Parties

Risk transfer involves shifting part of the potential financial impact to another party through mechanisms such as insurance policies, contractual indemnification, liability clauses, or service level agreements. While these measures do not eliminate risk, they can reduce its consequences.

Avoid or Redesign Risky Activities

In some situations, the most effective approach is to avoid the risk altogether. Organizations may choose alternative vendors, redesign business processes, or eliminate unnecessary exposures rather than accepting a high-risk scenario.

Continuously Monitor Risk

Because risks evolve over time, organizations should regularly review controls, vendor performance, compliance requirements, and emerging threats. Continuous monitoring helps identify changes in risk exposure and ensures mitigation strategies remain effective.

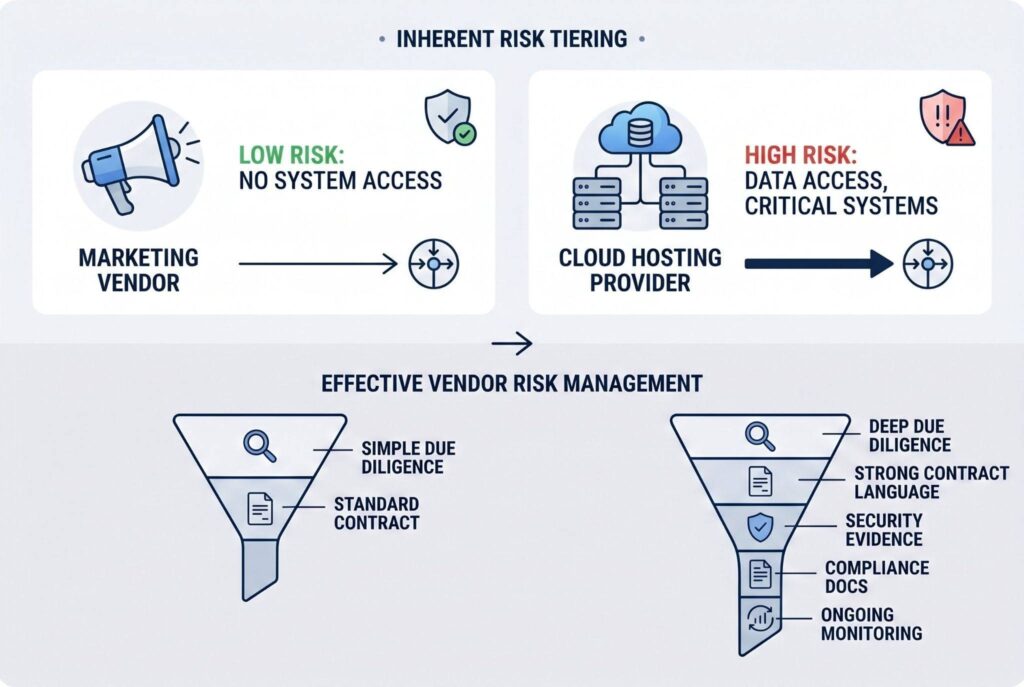

Inherent Risk Management in Third Party Relationships

Third party risk is one of the clearest examples of why inherent risk matters. Before reviewing a vendor’s controls, you should ask what damage the vendor could cause if everything went wrong.

Does the vendor access customer data? Does it connect to internal systems? Does it support a critical business function? Does it operate in a regulated environment? Does it subcontract work to other providers?

A low cost marketing vendor with no system access may have low inherent risk. A cloud hosting provider supporting customer transactions may have high inherent risk. These two vendors shouldn’t go through the same review process. Effective vendor risk management starts by tiering vendors according to inherent risk. High risk vendors need deeper due diligence, stronger contract language, security evidence, compliance documentation, and ongoing monitoring.

Common Mistakes When Assessing Inherent Risk

- The biggest mistake is scoring controls too early. Inherent risk should be measured before considering safeguards. If controls are included too soon, the score becomes closer to residual risk and the baseline is lost.

- Another mistake is using the same scoring logic for every department. Cybersecurity risk, audit risk, compliance risk, operational risk, and vendor risk may require different indicators.

- Teams also underestimate low frequency, high impact events. A ransomware attack, regulatory fine, or financial reporting failure may not happen often, but the impact can exceed millions of dollars.

- Finally, many companies document inherent risk once and then forget it. Risk profiles change as systems, vendors, markets, laws, and business models evolve.

Conclusion

Inherent risk isn’t something to fear or ignore. It’s the starting point for intelligent risk management. By identifying untreated risk first, organizations can see where they are naturally exposed before controls create a false sense of safety.

The best GRC programs use inherent risk to prioritize attention, allocate budget, design controls, and explain exposure to leadership. Once inherent risk is scored, teams can apply controls, measure residual risk, and decide whether the remaining exposure is acceptable.

In a volatile business environment, strong risk management starts with one honest question: how bad could this be if we did nothing? Answer that clearly, and every control decision becomes smarter.