A mortgage denial doesn’t always end the deal. If you’re buying a non-warrantable condo, a Non-QM loan may be an option. Depending on the lender, you may qualify using bank statements, rental income, or assets instead of traditional income documents. Common choices include DSCR loans, bank statement loans, and asset-based loans. Expect more flexible underwriting, but also higher down payments, interest rates, or stricter property reviews.

Why Your Condo Got Rejected: The Non-Warrantable Trap

Short-Term Rental Activity

A condo project may become non-warrantable if it functions more like a hotel than a residential community. Buildings that allow extensive short-term rentals, Airbnb activity, or hotel-style management are often viewed as higher risk by conventional lenders. These properties can experience fluctuating occupancy rates, increased investor involvement, and more complex legal or operational issues.

Excessive Commercial Space

Lenders may also reject a condo project if too much of the building is dedicated to commercial use. Restaurants, retail stores, offices, and other non-residential businesses can increase risk and make the project less attractive to agency-backed lenders. The higher the percentage of commercial space, the more likely the condo may fall outside standard lending guidelines.

High Ownership Concentration

Ownership concentration becomes a concern when a single investor, developer, or company owns a large percentage of the units. In these situations, the financial health of the homeowners association may depend heavily on one owner. If that owner stops paying dues or decides to sell multiple units at once, the entire community could be affected.

Financial and Legal Issues Within the HOA

Active lawsuits, inadequate reserve funds, high delinquency rates on HOA dues, incomplete construction, and insufficient insurance coverage can all contribute to a non-warrantable designation. These issues may signal financial instability and increase the likelihood of future problems for both owners and lenders.

Too Many Investor-Owned Units

Many lending programs prefer condo communities with a strong owner-occupancy rate. When a large percentage of units are owned by investors rather than residents, lenders may view the project as less stable. Investor-owned buildings can experience higher turnover rates and may be more vulnerable to market fluctuations.

Why These Factors Matter

A condo purchase involves more than evaluating a single unit. Buyers are also becoming part of a shared financial structure managed by the homeowners association. Because the health of the entire project can affect property values and loan performance, lenders carefully review these factors before approving financing.

How Non-QM Loans Unlock Real Estate Investing

Non-QM loans work differently because they don’t always judge the borrower or project through the same agency checklist. Instead, the lender may focus on whether the deal makes economic sense.

For real estate investors, the DSCR loan is often the most powerful option. DSCR means debt service coverage ratio. Instead of using your personal tax returns as the center of the approval, the lender evaluates whether the rental income from the property can cover the mortgage payment, taxes, insurance, and association dues. If the condo can generate enough rent, especially in a high demand short term rental market, a DSCR loan may open a path that conventional financing closed.

For self employed buyers, bank statement loans can help. Many business owners write off legitimate expenses, which lowers taxable income on paper. A conventional lender may see low income even when the business has strong cash flow. With a bank statement loan, the lender may review 12 to 24 months of personal or business bank deposits to estimate income more realistically.

For high asset borrowers, asset depletion or asset qualifier programs may work better. If you have strong savings, investments, or retirement assets but limited traditional income, the lender may use those assets to support the application.

These programs make non-qualified mortgage financing valuable for borrowers whose finances are solid but not simple.

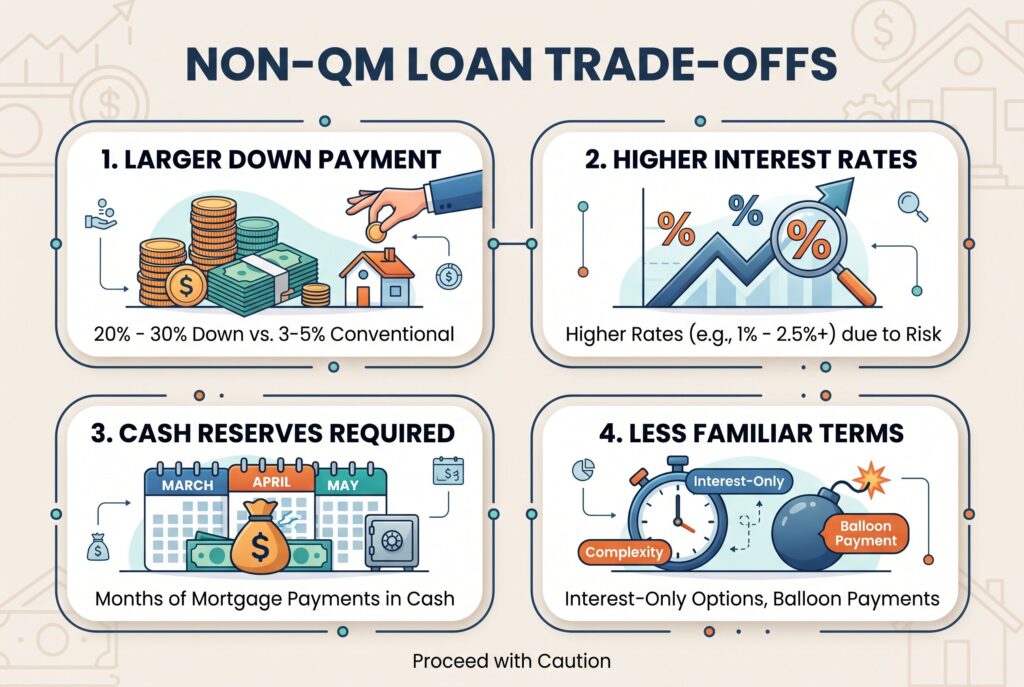

The Brutal Trade Offs: Proceed with Caution

The flexibility of non-QM loans comes at a price. You should understand that price before falling in love with the condo.

- First, the down payment is usually much larger. While some conventional loans allow 3% to 5% down, a non-QM mortgage for a non-warrantable condo may require 20% to 30% down. The lender wants more borrower equity because the property is harder to finance and may be harder to resell.

- Second, interest rates are usually higher. A Non-QM lender takes on more risk because the loan doesn’t fit standard agency rules. That risk gets priced into the rate. Even a 1% to 2.5% rate difference can change the cash flow of an investment property.

- Third, reserves may be required. The lender may want to see several months of mortgage payments available in cash or liquid assets. This is especially common for investors, short term rental properties, and high balance loans.

- Fourth, the loan terms may be less familiar. Some Non-QM products include an interest only mortgage option. Interest only payments can improve short term cash flow, but they don’t reduce principal during the interest only period. If property income drops or refinancing becomes difficult, that structure can become dangerous.

Be careful with balloon payment terms as well. A lower payment today isn’t helpful if it creates a major payment shock later.

Matching the Right Non-QM Product to the Buyer

A real estate investor buying a short term rental condo should usually start by asking about DSCR loan options. The key question is whether projected rent can support the debt.

A self-employed consultant, freelancer, or gig worker buying a vacation condo may fit better with a bank statement loan. The lender will want consistent deposits, clean business records, and a reasonable explanation of income.

A retiree or high net worth buyer may prefer an asset based loan if they have investment accounts but little monthly employment income. This can be useful when tax returns don’t reflect real purchasing power.

Foreign nationals and ITIN borrowers may also find Non-QM options, depending on the lender. These files usually require strong documentation, larger down payments, and careful identity and asset verification.

Conclusion

A Non-QM loan can make a non-warrantable condo purchase possible, but approval alone isn’t enough. Before moving forward, calculate whether the property can comfortably cover all ownership costs, including the mortgage, HOA dues, taxes, insurance, maintenance, vacancies, and the higher interest rate that often comes with Non-QM financing.

Just as importantly, review the HOA’s financial health. Ongoing lawsuits, low reserves, or inadequate insurance can create risks that strong rental demand won’t solve. The best Non-QM loan is one that supports a property with solid cash flow and long-term investment potential, not simply one that gets you to the closing table.