Navigating the complexities of taxes can be overwhelming, especially when it comes to understanding marginal tax rates. These rates play a significant role in determining how much you owe in taxes, yet many people misunderstand how they actually affect their overall tax liabilities.

Whether you’re a salaried employee, a freelancer, or a small business owner, understanding marginal tax rates can help you make smarter financial decisions, maximize your tax savings, and avoid any tax-related surprises. In this article, we’ll break down what marginal tax rates are, how they are calculated, and explore strategies you can use to optimize your tax return and minimize liabilities. Let’s dive in!

What Is a Marginal Tax Rate?

A marginal tax rate is the rate at which your last dollar of income is taxed. Unlike a flat tax rate, where all income is taxed at the same rate, the U.S. operates on a progressive tax system, which means that income is taxed at different rates as it moves through various income brackets. The higher your income, the higher your marginal tax rate will be, but importantly, only the income within a certain tax bracket is taxed at that higher rate.

How Does the Progressive Tax System Work?

In the U.S., the tax system works in a tiered structure, meaning your income is taxed at different rates based on the bracket it falls into. For example, if you’re in a 22% tax bracket, only the portion of your income that falls within that bracket is taxed at 22%, not your entire income. This progressive system is designed to ensure that individuals with higher incomes pay a greater share of taxes, but it doesn’t penalize you for earning more.

Example: How Marginal Tax Rates Apply

For instance, let’s say you’re a single filer with a taxable income of $50,000 in 2026. According to the IRS tax brackets for that year, your income will be taxed at different rates for each portion of it:

- 10% on the first $11,000

- 12% on income from $11,001 to $44,725

- 22% on income from $44,726 to $50,000

So, although your taxable income is $50,000, only the income over $44,725 is taxed at 22%. The rest is taxed at the lower rates. This makes the progressive tax system more favorable to middle-income earners.

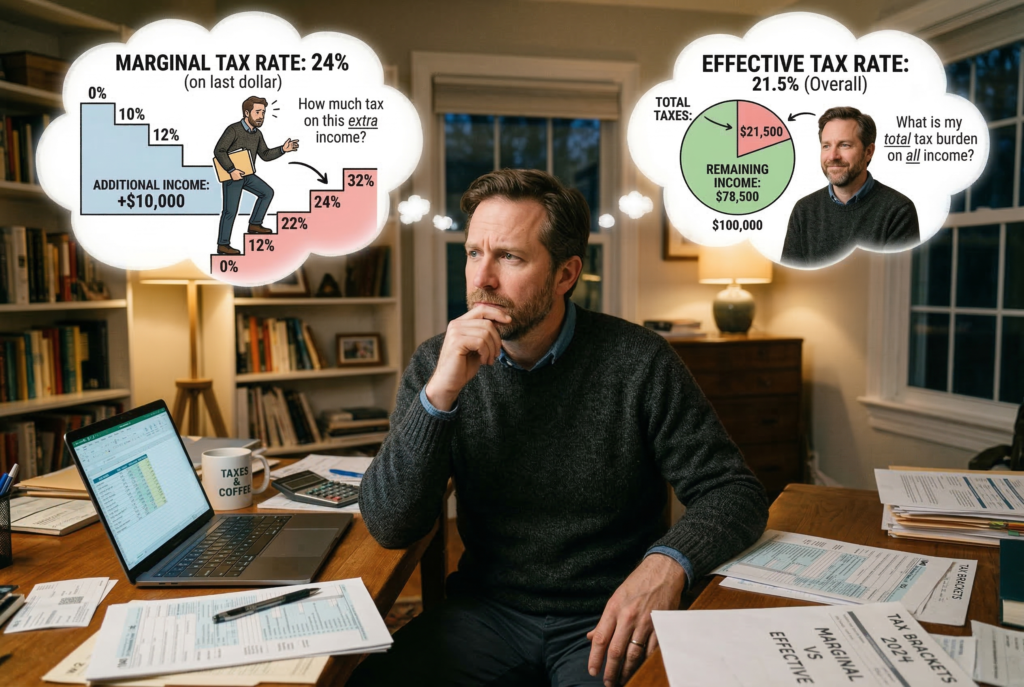

The Difference Between Marginal and Effective Tax Rates

It’s important to distinguish between marginal tax rate and effective tax rate, as they refer to two different concepts in the context of taxes. While the marginal rate is the percentage you pay on your next dollar of income, the effective tax rate represents the average rate you pay on your total income after considering all deductions, credits, and tax breaks.

For example, if your marginal tax rate is 22%, but after applying various deductions and tax credits your total tax liability is $7,500 on an income of $50,000, your effective tax rate would be only 15%. This is a crucial distinction when planning for taxes and optimizing your financial strategy.

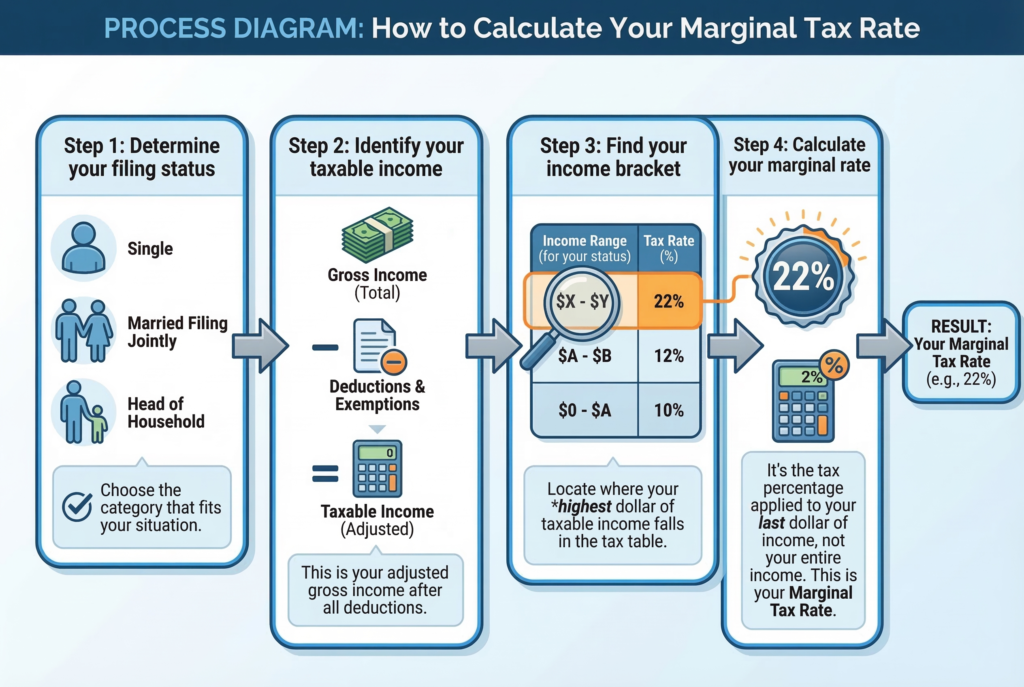

How to Calculate Your Marginal Tax Rate

Calculating your marginal tax rate may seem complicated, but it can be broken down into clear steps. Here’s a simplified approach to determining your marginal tax rate:

- Determine your filing status: Are you filing as single, married filing jointly, or head of household? Your filing status affects the income thresholds for each tax bracket.

- Identify your taxable income: Your taxable income is your total income minus deductions (such as standard or itemized deductions) and other tax-exempt income.

- Find your income bracket: Refer to the IRS tax brackets for the year (such as for 2026) to determine which bracket your taxable income falls into.

- Calculate your marginal rate: The highest tax bracket that your income reaches is your marginal tax rate.

Example of Calculating Marginal Tax Rate

Let’s say you’re a single filer in 2026 with a taxable income of $85,000. Based on the 2026 IRS tax brackets, your income would fall into the 24% tax bracket, so your marginal tax rate would be 24%. This means that any additional income you earn above $85,000 will be taxed at 24%.

Tax Planning Strategies to Maximize Savings

1. Contribute to Retirement Accounts (401(k), IRA, Roth IRA)

One of the best ways to reduce your taxable income is by contributing to retirement accounts like a 401(k) or IRA. Contributions to these accounts are tax-deferred, meaning the money you put in is not taxed until you withdraw it in retirement. This lowers your taxable income in the current year and can help you reduce your marginal tax rate.

For 2026, you can contribute up to $23,000 to a 401(k) and $6,500 to an IRA, with additional catch-up contributions available for those over 50.

2. Take Advantage of Tax-Advantaged Accounts

Besides retirement accounts, consider contributing to other tax-advantaged accounts like Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs). Contributions to these accounts are made with pre-tax dollars, lowering your taxable income. Additionally, HSAs allow your contributions to grow tax-free, and withdrawals for medical expenses are tax-free as well.

3. Maximize Tax Deductions and Credits

Be proactive in utilizing all available tax deductions and tax credits. Common deductions include mortgage interest, student loan interest, and medical expenses. Some tax credits, like the Child Tax Credit, can directly reduce your tax liability. For 2026, the Child Tax Credit allows you to claim up to $2,000 per qualifying child.

4. Use Tax-Loss Harvesting to Offset Gains

If you have investments in taxable accounts, consider tax-loss harvesting, which involves selling losing investments to offset taxable gains. This strategy can help lower your overall taxable income by reducing the taxes owed on capital gains.

5. Consider Filing Jointly if Married

If you’re married, filing jointly can often provide significant tax savings compared to filing separately. Filing jointly allows you to take advantage of higher income thresholds for tax brackets, making it easier to stay in a lower tax bracket.

Conclusion: Take Control of Your Taxes and Maximize Your Savings

Understanding how marginal tax rates work and applying effective tax planning strategies can significantly reduce your tax liabilities and maximize your savings. Whether you’re contributing to retirement accounts, utilizing tax deductions, or leveraging tax-loss harvesting, there are many ways to optimize your financial situation.

Don’t wait until tax season to think about your tax strategy. By taking proactive steps now, you can ensure that you’re minimizing your tax burden and positioning yourself for long-term financial success. With the right planning, you can keep more of your hard-earned money and ensure you’re fully prepared for whatever the future brings.