: Costs, How It Works, and Ways to Lower or Remove It")

If you’re using an FHA loan, mortgage insurance premium (MIP) is one of the most important costs to understand before buying a home. While it helps borrowers qualify with a lower down payment, it also increases both upfront expenses and monthly payments. Knowing how MIP works and how to reduce or remove it can help you make a smarter mortgage decision.

What Is Mortgage Insurance Premium (MIP) and Why FHA Loans Require It

Mortgage insurance premium (MIP) is required on all FHA loans. It protects the lender, not the borrower, in case of default. That’s why you’re paying for coverage that benefits the lender’s risk, not your personal financial protection.

Unlike conventional loans where insurance may be avoidable with a larger down payment, FHA loans require MIP regardless of credit score or financial strength. This makes it a built-in cost of choosing FHA financing.

How FHA MIP Works: Upfront and Annual Costs Explained

FHA mortgage insurance comes in two parts:

- Upfront MIP: Typically 1.75% of the loan amount, paid at closing or rolled into the loan

- Annual MIP: Charged yearly but paid monthly as part of your mortgage payment

The annual rate varies depending on your loan term, loan size, and loan-to-value ratio (LTV). For many common FHA loans, the rate is around 0.55% annually, though it can be higher or lower depending on your situation. Because the upfront fee can be financed, many borrowers underestimate the total cost. Financing it increases both your loan balance and long-term interest paid.

How Much MIP Adds to Your Monthly Mortgage Payment

MIP directly increases your monthly housing cost. Even if it seems small at first, it can add up to hundreds of dollars per year and thousands over time. This impacts your monthly affordability, your ability to qualify for a loan, and your total cost of ownership. The higher your loan amount, the more noticeable the effect becomes, which is why comparing loans without factoring in MIP can lead to misleading conclusions.

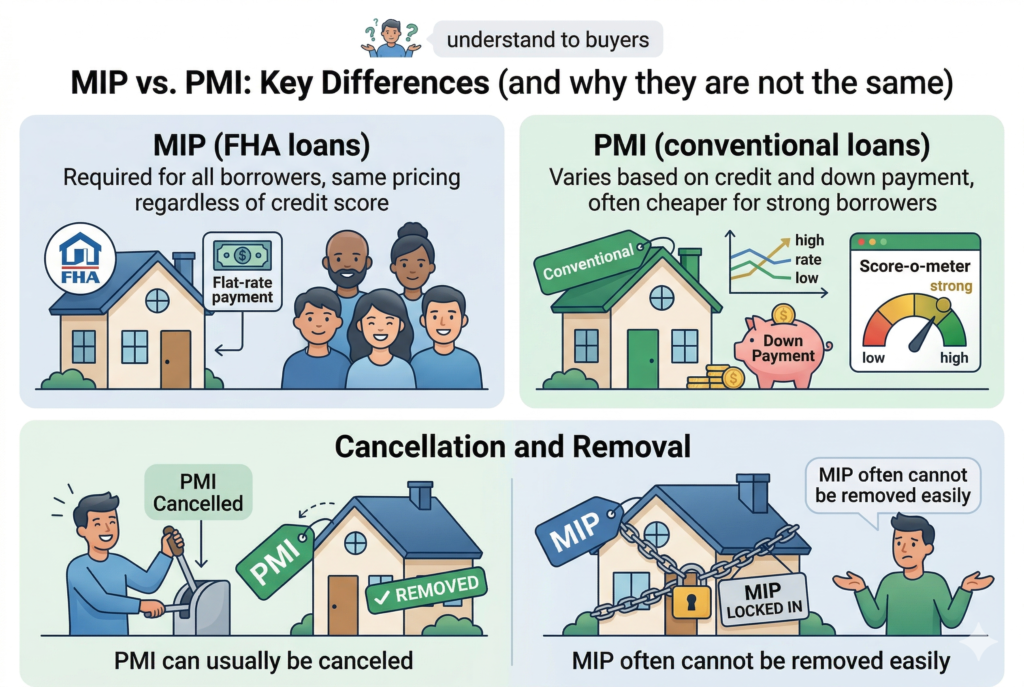

Key Differences Between MIP vs PMI You Should Understand

Many buyers confuse MIP with PMI, but they work differently:

- MIP (FHA loans): Required for all borrowers, same pricing regardless of credit score

- PMI (conventional loans): Varies based on credit and down payment, often cheaper for strong borrowers

- PMI can usually be canceled, while MIP often cannot be removed easily

This difference is critical. A conventional loan may look harder to qualify for upfront but can be cheaper long term.

How Long You Pay MIP on an FHA Loan

The duration of MIP payments depends largely on your loan details. For many newer FHA loans, MIP lasts for the life of the loan, meaning it won’t automatically go away even as you build equity. In contrast, some older FHA loans allowed MIP to be removed after reaching certain equity thresholds. It’s also important to understand that paying down your loan faster doesn’t necessarily eliminate MIP on its own. This is one of the biggest drawbacks of FHA loans, since unlike PMI, you often can’t simply wait for the insurance cost to disappear over time.

When and How You Can Remove MIP

In most modern FHA loans, the primary way to remove MIP is by refinancing into a conventional loan. This typically becomes possible once you’ve built enough home equity, improved your credit score, and can qualify for better loan terms. Refinancing allows you to replace FHA MIP with potentially lower-cost private mortgage insurance (PMI), or eliminate mortgage insurance entirely if you’ve reached at least 20% equity in your home. While some older FHA loans issued before certain rule changes may allow MIP cancellation under specific conditions, this option doesn’t apply to most recent borrowers.

Smart Strategies to Lower MIP Costs Over Time

Even if you can’t eliminate MIP immediately, there are several ways to reduce its overall impact.Making a larger down payment can help you qualify for lower annual MIP rates, while avoiding financing the upfront MIP keeps your total loan balance and interest costs lower. It’s also smart to work on improving your credit profile so you can position yourself for a future refinance into a more favorable loan. In addition, choosing your loan terms carefully can make a difference, as shorter loan terms may come with lower MIP rates.

When an FHA Loan With MIP Still Makes Sense

Despite the extra cost, FHA loans still serve an important role in helping many buyers access homeownership. They can be a practical option if you have a lower credit score, don’t have a large down payment saved, or need more flexible qualification standards than conventional loans typically offer. In these situations, MIP becomes the tradeoff for getting approved and securing a home. The key is to go in with a clear long-term plan so you can reduce or remove that added cost over time.

How to Compare FHA Loans With Other Mortgage Options

Before choosing an FHA loan, it’s important to look beyond the surface and evaluate the full financial picture. Compare the total monthly payment, including mortgage insurance premiums (MIP), and focus on the APR rather than just the interest rate to understand the true cost of borrowing. You should also consider how much the loan will cost over the next 5 to 10 years and whether you’ll have the option to remove mortgage insurance later. FHA loans can be a helpful entry point for buyers with limited credit or savings, but they aren’t always the most cost-effective long-term solution.

Conclusion

Mortgage insurance premium (MIP) is a required cost of FHA loans that can significantly affect both your monthly payment and total loan cost. While it allows buyers to purchase a home with a lower down payment, it often stays longer and costs more than conventional PMI. The smartest approach is to understand how MIP works from the start, compare it carefully with other loan options, and create a plan to reduce or remove it over time through equity growth or refinancing.

Related Articles

Mortgage Insurance Explained: Costs, Types, and How to Avoid or Reduce Extra Monthly Payments