If you’re comparing cash accounts in 2026, the first thing you probably want isn’t theory. You want numbers. That’s why a simple money market calculator can be so helpful before you decide where to park your savings. Whether you’re reviewing a money market account calculator for emergency-fund planning or trying to compare a money market account with a high-yield savings option, the goal is the same: understand how your APY, deposit size, and monthly contributions change the outcome over time.

Use this simple setup as your starting point:

- Initial Deposit

- APY %

- Monthly Contribution

For example, if you deposit $10,000 at 4.25% APY and add $250 per month, even a small rate difference can noticeably change your ending balance over a year or two. That’s why the money market vs savings decision shouldn’t start with brand names. It should start with how you plan to use the money.

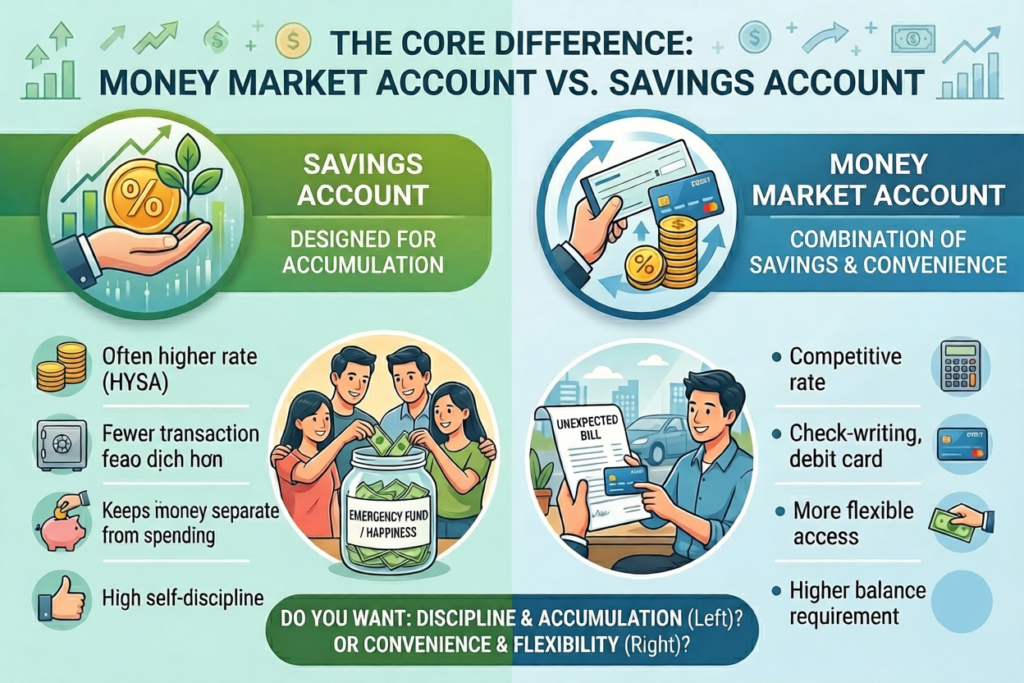

The Core Difference: Money Market Account vs Savings Account

The biggest difference in the money market account vs savings account debate is flexibility. A savings account, especially a high-yield savings account, is usually designed for parking cash and letting it grow quietly. It’s great for emergency savings, house funds, or short-term goals when you don’t want everyday spending access. In many cases, it offers a competitive APY with fewer transactional features.

A money market account, by contrast, usually adds more convenience. Many money market accounts offer debit card access, check-writing privileges, or easier transactional flexibility than a standard savings account. That doesn’t mean every account is the same, but in general, a money market account is built for savers who want both yield and easier access.

So when people search money market vs savings or money market account vs savings account, the real question is often this: do you want your cash slightly more separated from spending, or do you want a savings product that still feels more reachable when life happens? For many savers, that’s the dividing line. If you want discipline, a savings account may be better. If you want your emergency fund to stay productive but still close at hand, a money market account may fit more naturally.

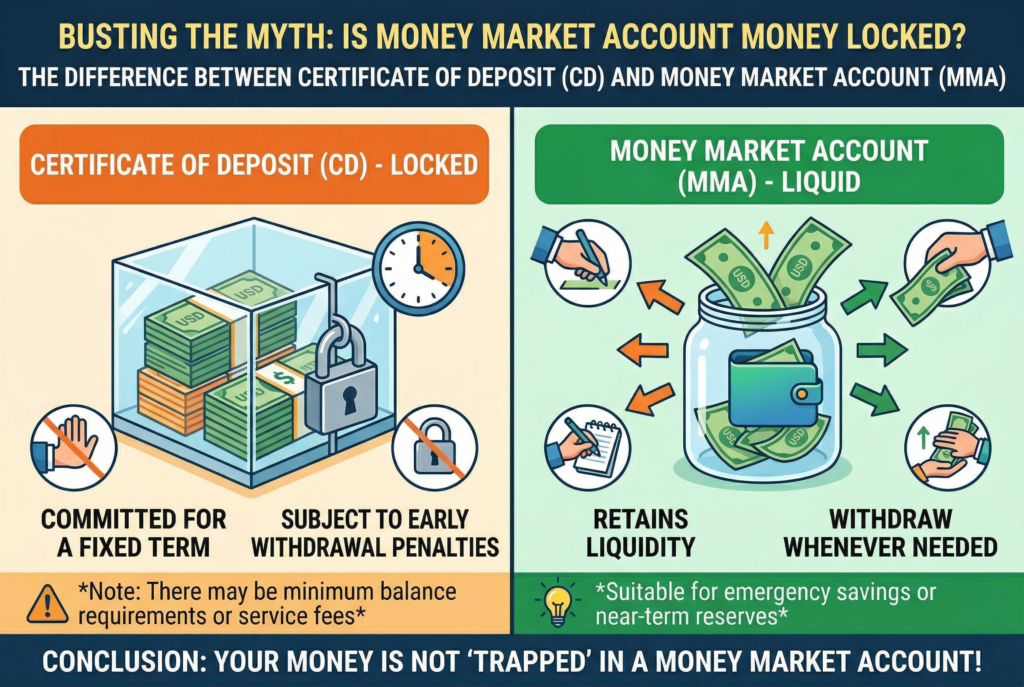

Busting the Myth: Is Money Market Account Money Stuck for a Set Time?

A lot of people still ask some version of this question: is money market account money stuck for a set time?

No, it isn’t. A money market account doesn’t lock your money away for a fixed term like a certificate of deposit. That confusion happens because the names sound similar, but the products work differently.

With a CD, your money is generally committed for a fixed period unless you pay an early withdrawal penalty. With a money market account, your money remains liquid. You can usually withdraw it whenever you need to, even if the account may have certain transaction rules or bank-specific limits.

That’s why a money market account can work well for emergency savings or near-term reserves. Your cash isn’t trapped. It’s available. The tradeoff is that some accounts may come with minimum balance requirements or fee conditions, which means you still need to read the fine print. So if you’ve been worried that money market account money stuck for a set time is part of the deal, it isn’t. The money is accessible. The real issue is usually account structure, not lock-in.

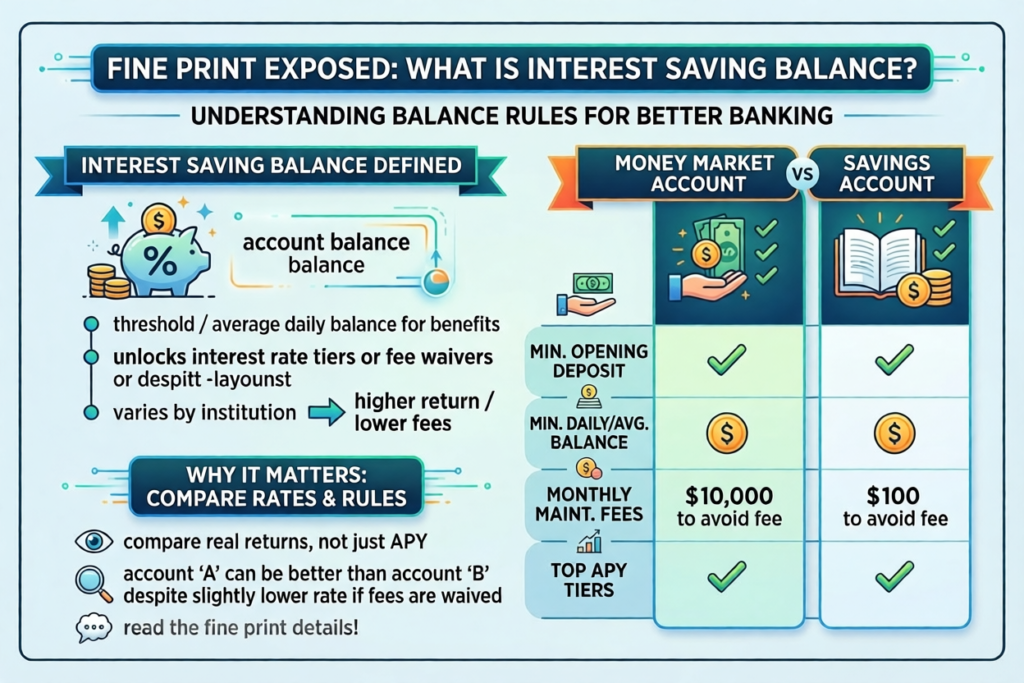

Fine Print Exposed: What Is Interest Saving Balance?

Another term that causes confusion is interest saving balance. So, what is interest saving balance? In practical banking terms, this usually refers to the balance threshold or average daily balance needed for interest benefits, fee waivers, or maintenance requirement relief. Different institutions define it differently, but the idea is similar: your balance level affects what you earn and what fees you avoid.

This matters because two accounts with the same advertised APY may not feel the same once balance rules enter the picture. One account may look attractive at first glance, but if it requires a high balance to avoid monthly fees or access the best rate tier, your real return may be lower than expected.

That’s why understanding what interest saving balance matters so much in a real money market vs savings comparison. You’re not just comparing rates. You’re comparing rates plus rules. If you’re choosing between a money market account and a savings account, always check:

- minimum opening deposit

- minimum daily or average balance

- monthly maintenance fees

- whether the top APY applies to your full balance or only a tier

Those details often matter more than a flashy headline rate.

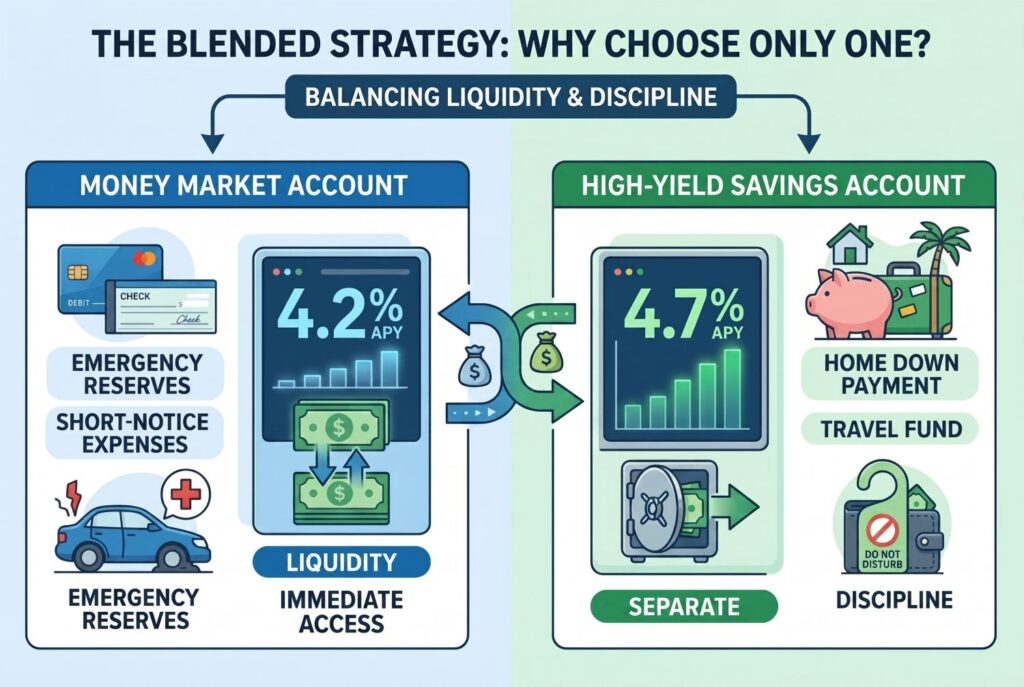

The Blended Strategy: Why Choose Only One?

One of the smartest cash-management moves is to stop treating this like an all-or-nothing decision. A blended setup often works better than forcing yourself to choose only one account. For example, you might keep your emergency fund in a money market account because you value check access, debit flexibility, or the comfort of knowing the money is readily usable during a medical bill or urgent car repair. Then you might keep your home down payment fund or travel savings in a separate high-yield savings account so the money stays a little farther from impulse spending.

This is where the money market account vs high yield comparison becomes more realistic. It isn’t always about which one wins in theory. It’s about which one fits the specific job.

A good blended strategy could look like this:

- Money market account for emergency reserves and short-notice expenses

- High-yield savings account for goal-based saving where you want stronger separation

- Optional CD or brokerage cash tools only if you truly don’t need immediate access

That kind of setup helps you balance behavior and math. One account protects liquidity. The other protects discipline.

How to Think About Yields Before You Choose

The money market calculator idea matters because rates change, but behavior matters more. A slightly higher APY won’t help much if fees eat the difference or if the account encourages easier spending than your goal allows. Likewise, a lower-friction savings account may outperform for your situation even if the rate looks a touch lower on paper.

Before making a decision, you should first plug in your own numbers: how much you’re depositing initially, how much you plan to contribute each month, the real APY after accounting for fees or balance requirements, and whether you need easy access to your money or prefer built-in separation. When you do this, a money market account calculator stops being just a curiosity and becomes a practical decision-making tool that helps you choose what truly fits your financial needs.

Conclusion

The best answer in the money market vs savings discussion depends on how you use your cash, not just which product has the flashiest rate today. A savings account is often better for focused long-term saving with fewer temptations. A money market account can be better when flexibility matters and you still want your money earning interest. And if you want the smartest overall setup, using both may be even better than forcing a single choice. Before opening anything, go back to the money market calculator, test a few APY scenarios, and compare the result against your real goals. Once you do that, the right account usually becomes much clearer.

Related Articles

CD vs. Money Market Calculator: Which Account Earns You More?