When people compare pensions and annuities, they’re usually asking a deeper question than product definitions. They want to know whether their retirement income will still be there when markets fall, employers fail, or they live longer than expected. That’s why phrases like are annuities safe and are annuities a good investment matter so much. Both pensions and annuities are built around the same promise – predictable income, but they rely on different institutions, different safety nets, and different tradeoffs. If you’re trying to build retirement cash flow you can actually trust, you need to look beyond the word “guaranteed” and understand what stands behind it.

The Decline of the Pension and the Rise of the Annuity

For decades, a traditional pension gave workers something many retirees now miss: a monthly paycheck that kept arriving after work ended. But in the private sector, pensions have become far less common, which means more households now have to create their own pension-like income stream instead of receiving one automatically from an employer. That shift is one reason annuities have become much more visible in retirement planning.

An income annuity is essentially one way to buy that missing paycheck. Instead of relying on an employer-sponsored defined benefit plan, an individual uses personal savings to purchase a contract that can send monthly payments for life or for a set period. That doesn’t make pensions and annuities identical, but it does explain why they’re often mentioned together. In practical retirement planning, both are trying to solve the same fear: outliving your money.

That’s also why the topic has become more important, not less. Fewer people can count on employer-backed income, while more people are worried about longevity risk, inflation, and the pressure of turning a retirement account balance into a sustainable monthly withdrawal strategy.

Are Pensions Safe? (Understanding the PBGC)

A pension is usually only as strong as the employer and the plan structure behind it. That’s what makes the safety question so important. If a company runs into financial trouble, retirees naturally worry about whether promised pension income can still be paid.

In the U.S., one of the major safety nets for private-sector defined benefit pensions is the Pension Benefit Guaranty Corporation, or PBGC. Its role is to insure certain private-sector pension benefits when an employer can’t continue supporting the plan. That doesn’t mean every pension promise is protected in full under every circumstance, but it does mean there is an institutional backstop that helps prevent many retirees from losing the entire value of their pension income if a sponsoring employer fails.

This matters because many people assume a pension is automatically risk-free. It isn’t. It’s generally very strong, but the safety comes from a system that includes the employer, the pension plan itself, and, where applicable, the PBGC backstop. The guarantee is real, but it still exists within rules and limits.

Are Annuities Safe? (How Insurance Companies Protect Your Money)

Are annuities safe? In general, fixed annuities and other insurance-based guaranteed income products can be very safe when issued by financially strong insurers, but the source of protection is different from what many people expect.

Annuities aren’t backed by the FDIC, and that point matters. They’re insurance contracts, not bank deposits. So the safety analysis starts with the insurer’s claims-paying ability. That’s why checking an insurer’s financial strength ratings is an essential step before buying. Companies like A.M. Best and Moody’s are often used to evaluate the financial condition of insurers, and those ratings can help consumers judge whether the company behind the contract looks stable enough to trust for long-term retirement income.

There is also another layer of protection: State Guaranty Associations. These state-level systems may provide coverage up to certain limits if an insurer fails. That doesn’t make product selection irrelevant, and it doesn’t mean every contract is protected without limit. It means there is a backstop structure, but one that varies by state and should be understood before purchase. So, are annuities safe? Usually, yes, when chosen carefully and issued by strong insurers. But “safe” shouldn’t be interpreted as “no homework required.” Insurer quality still matters a lot.

Are Annuities a Good Investment? The Real Pros and Cons

The harder question isn’t only whether annuities are safe. It’s whether they’re a good use of retirement money.

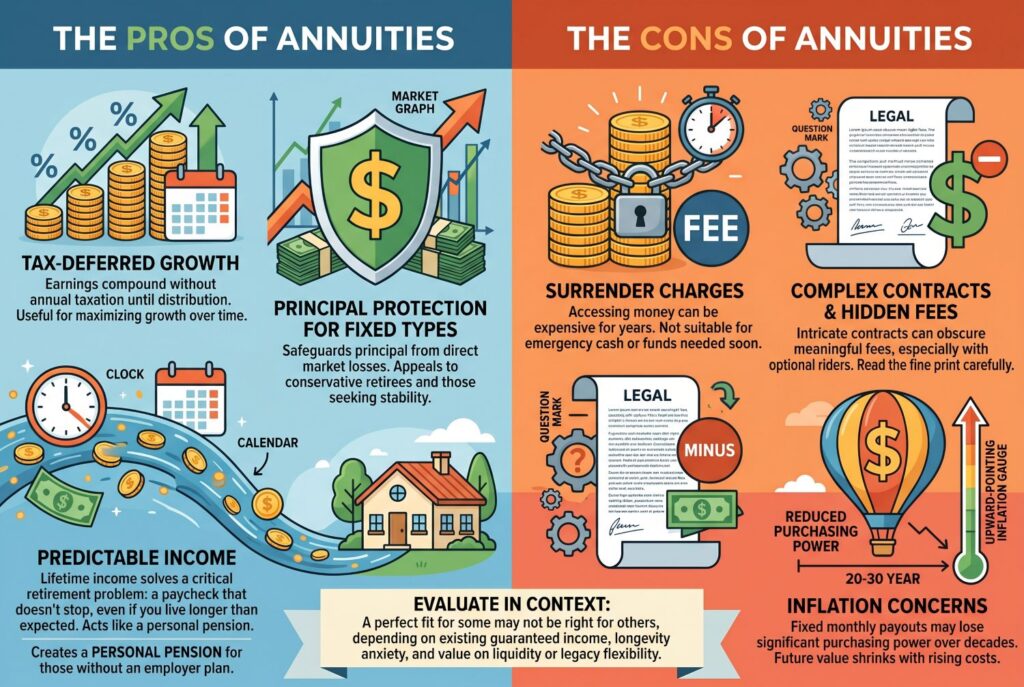

The Pros of Annuities

The biggest strengths in the annuities pros and cons debate are tax deferral, principal protection for fixed types, and predictable income. Tax-deferred growth can be useful for people who want earnings to compound without annual taxation until distribution. Fixed annuities can also protect principal from direct market losses, which is especially appealing to conservative retirees. And a lifetime income annuity can solve one of the hardest retirement problems of all: creating a paycheck that doesn’t stop simply because you live longer than expected.

For people without a pension, that can be extremely valuable. In effect, annuities can help create a personal pension where no employer one exists.

The Cons of Annuities

The cons are real too. Surrender charges can make access to your money expensive for years, which means annuities aren’t good homes for emergency cash or funds you may need soon. Complex contracts can hide meaningful fees, especially once optional riders enter the picture. And inflation is a serious long-term concern. A fixed monthly payout may feel comforting today, but after 20 or 30 years, its purchasing power can shrink much more than retirees expect.

That’s why the pros and cons of annuities have to be evaluated in context. A product that looks excellent for someone with no pension and high longevity anxiety may look far less attractive for someone who already has strong guaranteed income and values liquidity or legacy flexibility more.

Tax Traps to Avoid: IRS Withholding Rules on Payouts

Taxes are one of the easiest areas to underestimate. In general, federal income tax withholding applies to the taxable portion of pension and annuity payments. That sounds simple, but the details matter. The withholding treatment can differ depending on whether the payment is periodic, nonperiodic, or an eligible rollover distribution.

One major trap is taking an eligible rollover distribution as a lump sum rather than using a direct rollover. In many cases, if the money is paid directly to you instead of rolled over properly, mandatory 20% federal withholding may apply. That can surprise people who thought they were simply moving retirement money, not triggering an avoidable withholding event.

This is also where forms like W-4P and W-4R come in. They help determine or adjust withholding treatment for pensions and annuity payments. The rules aren’t impossible to follow, but they can easily be mishandled if you approach rollover or payout conditions too casually.

Conclusion

Pensions and annuities can both be strong foundations for retirement income, and in most cases they are generally very safe because each has institutional backstops built into the system. But safety alone doesn’t answer the whole question. The real value of either option depends on insurer or plan strength, inflation protection, tax treatment, and how the income fits with the rest of your retirement assets.

If you’re evaluating guaranteed income seriously, don’t stop at “safe or unsafe.” Review PBGC coverage if a pension is involved, check insurer ratings and State Guaranty limits if an annuity is involved, and think carefully about withholding and rollover consequences before making payout decisions. That’s how retirement income becomes not just guaranteed on paper, but genuinely dependable in real life.