If you’ve been asking what is an FIA investment, the short answer is this: it’s a fixed index annuity designed to protect your principal while giving you some opportunity to grow based on a market index. That mix of downside protection and limited upside is exactly why the fixed index annuity category has attracted so much attention from retirement-focused investors. But the product isn’t as simple as the sales pitch often makes it sound. To understand whether an FIA belongs in your plan, you need to know how the crediting formula works, where the limits are, and which tradeoffs hide behind the promise of safety.

Decoding the FIA: What is a Fixed Indexed Annuity?

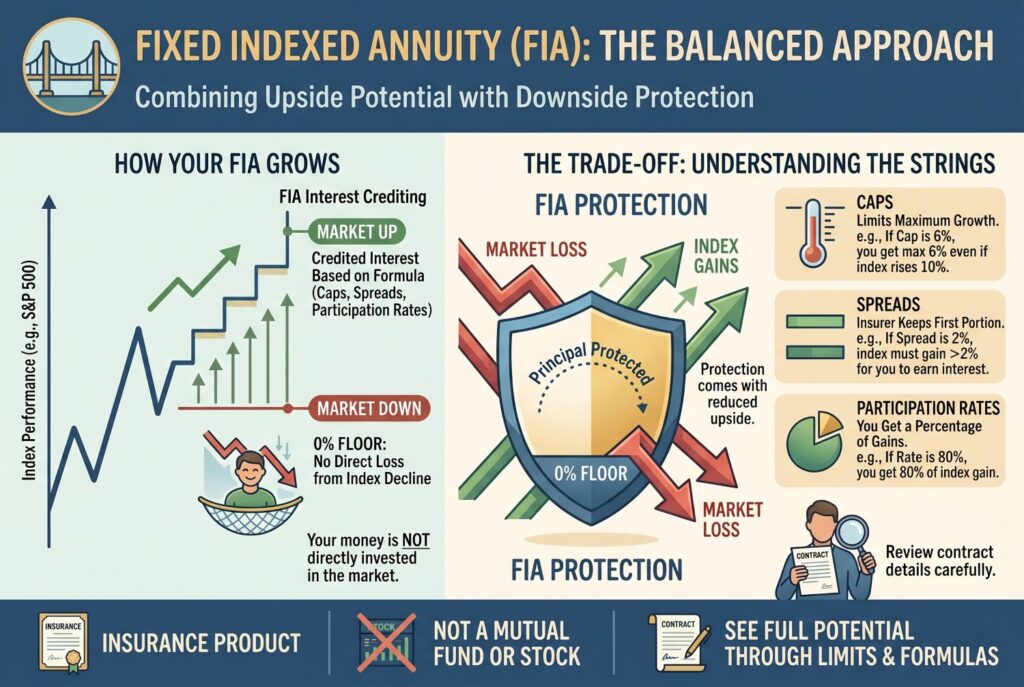

A fixed indexed annuity, sometimes called an index annuity, is an insurance product that links part of its growth potential to the performance of a market index while protecting you from direct market losses. In plain terms, it’s built for people who want more upside than a traditional fixed annuity but less downside risk than market-based investments.

So what is a FIA in everyday language? It isn’t a mutual fund, and it isn’t a direct stock market investment. Your money is held inside an annuity contract, and the insurer uses a formula to decide how much interest gets credited based on index performance. If the market falls, the contract typically applies a 0% floor, which means you don’t lose principal because of index decline. That’s one of the biggest emotional selling points of an FIA investment. People like the idea that bad market years don’t directly reduce their annuity value.

But that protection comes with strings attached. You don’t get the full market upside either. The contract keeps some of that upside through limits and formulas, and those details matter more than most buyers realize.

How FIA Investments Work: The Mechanics of Growth

This is where many people get lost, because the product brochure often sounds easier than the actual contract. The basic idea is simple enough: your return is tied to an index. But the insurer doesn’t just give you whatever the index earns.

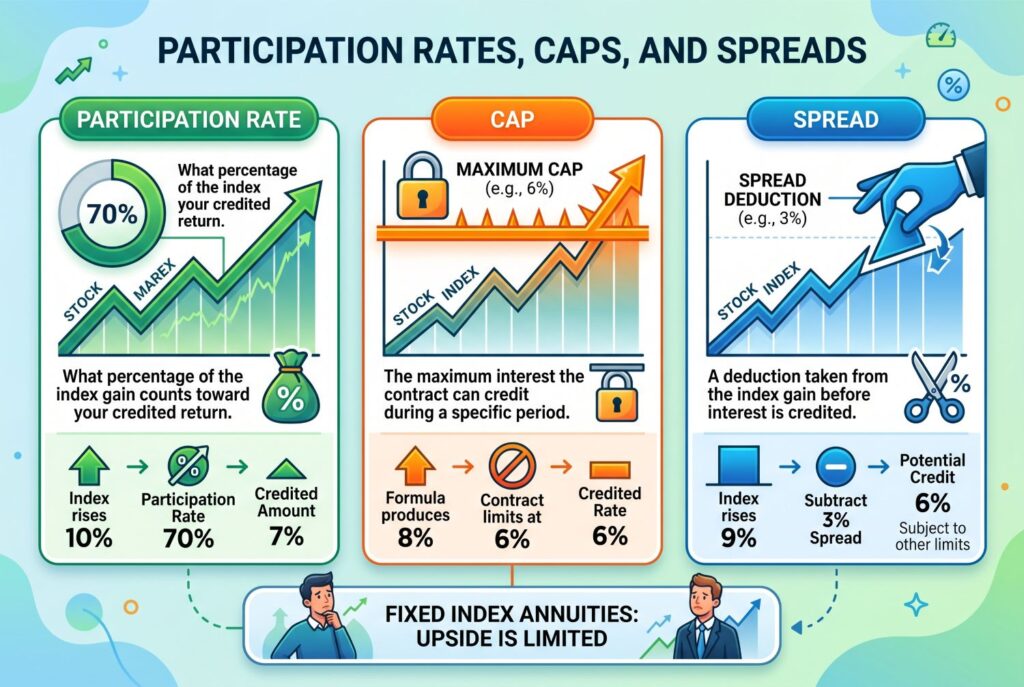

Participation Rates, Caps, and Spreads

A participation rate tells you what percentage of the index gain counts toward your credited return. If the participation rate is 70% and the index rises 10%, your starting credited amount may be 7%.

A cap is the maximum interest the contract can credit during a specific period. If your contract has a 6% cap and the formula produces 8%, you still only receive 6%.

A spread is a deduction taken from the index gain before interest is credited. If the index rises 9% and the spread is 3%, the insurer may only credit 6%, subject to any other limits.

This is why a fixed index annuity can feel disappointing if someone expects stock-market-like growth. Yes, the index may soar in a strong year, but your contract may still deliver a much lower credited rate because participation rates, caps, and spreads all work together to limit upside.

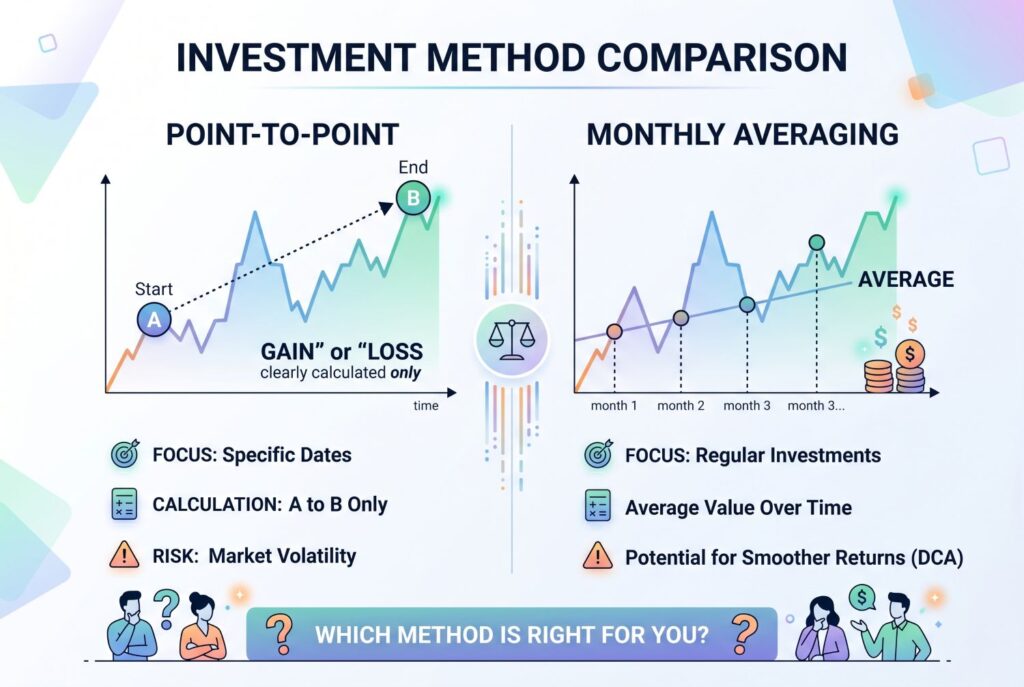

Point-to-Point vs. Monthly Averaging

Another important detail is the crediting method. Point-to-point looks at the index value at the start and end of a defined period, often one year. Monthly averaging uses multiple measurements across the year and averages them.

Point-to-point can feel more direct, but it may create different outcomes depending on when the market moves. Monthly averaging can smooth things out, but it may also dilute gains in sharply rising markets. These methods don’t change the core value proposition of an FIA investment, but they do affect how much growth you actually see over time.

The “Hidden” Pros: Why Investors are Flocking to FIAs in 2026

The strongest fixed indexed annuity benefits are easy to understand once you step back from the fine print.

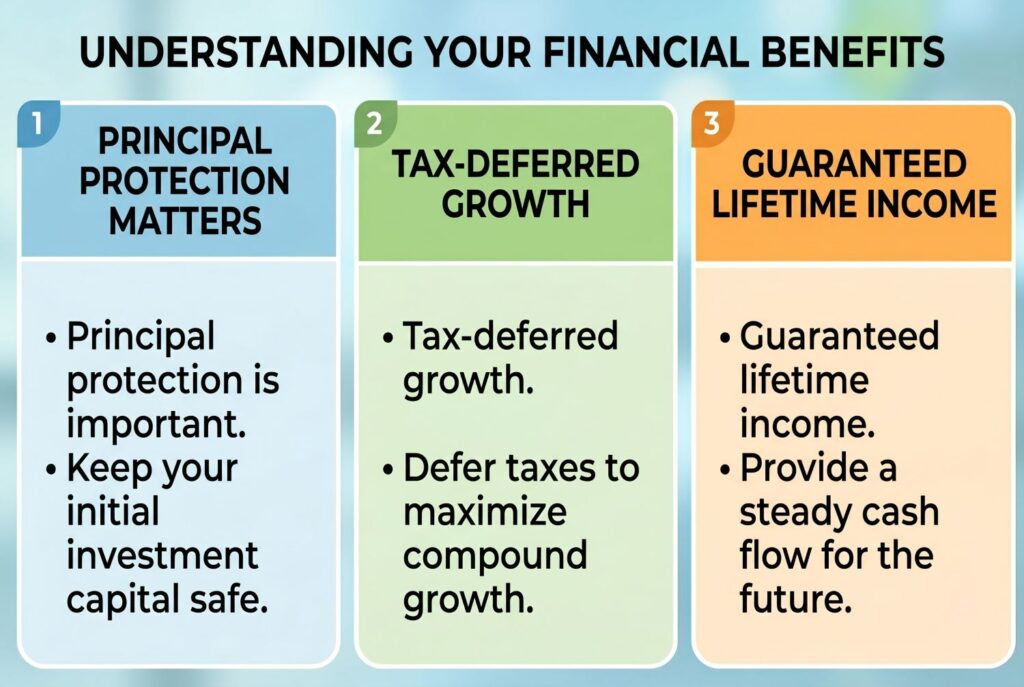

First, principal protection matters. For people nearing retirement, avoiding a major drawdown can matter more than chasing the highest possible return. An FIA can feel psychologically reassuring because a bad stock market year doesn’t directly slash the contract value due to index losses.

Second, growth is tax-deferred. Like many annuities, an FIA investment allows gains to compound without annual taxation until withdrawal. That can make the product more attractive for people who want deferred growth alongside future income planning.

Third, many contracts offer ways to convert the value into guaranteed lifetime income, either through annuitization or optional riders. For retirees worried about longevity risk, that income angle is one of the category’s biggest appeals. An FIA isn’t just about growth. It’s also about converting a portion of retirement assets into something paycheck-like.

The “Hidden” Cons: What the Brochure Doesn’t Tell You

This is where the pros and cons of annuities discussion gets real. Surrender charges are often the biggest trap for buyers who need flexibility. Many FIA contracts impose meaningful penalties for early withdrawals, and those surrender schedules can last 7 to 10 years. That means this isn’t the right place for money you may need soon.

Capped returns are the second major issue. You’re never getting the full S&P 500 experience. The insurer keeps some of the upside through caps, spreads, or participation limits. In strong bull markets, that can create a big gap between what the market did and what your contract actually credited.

Complexity is the third major drawback. Two FIA contracts can look similar in marketing language but behave very differently because of rider costs, crediting methods, participation formulas, renewal provisions, and withdrawal rules. This is one reason people researching the pros and cons of annuities often end up more confused after reading product brochures than before.

FIA vs. RILA vs. Fixed Annuity: Which One Suits You?

A fixed rate annuity is the simplest option. It offers more predictable interest but generally lower growth potential. An FIA gives you principal protection against index losses with limited upside based on contract formulas.

A RILA, or registered index-linked annuity, usually gives you more upside potential than an FIA, but unlike an FIA, it may expose you to some market downside beyond a defined buffer.

| Product | Downside Risk | Upside Potential | Complexity |

|---|---|---|---|

| Fixed rate annuity | Lowest | Lowest | Low |

| FIA | Low with 0% floor | Moderate, capped | Medium to high |

| RILA | Partial downside exposure | Higher | High |

That’s the heart of FIA vs RILA. FIAs are usually for people who want protection first. RILAs are for people willing to absorb some downside in exchange for more upside potential.

Who Should (and Shouldn’t) Invest in an FIA?

An FIA may suit someone close to retirement who values principal protection, wants tax-deferred growth, and may eventually want guaranteed income. It may not suit a younger investor who needs high liquidity, wants full market participation, or has a long enough time horizon to tolerate volatility for stronger long-term growth.

It’s also a weaker fit for anyone who doesn’t fully understand the contract. If you can’t clearly explain the cap, the participation rate, the surrender schedule, and the rider costs, you probably shouldn’t sign yet.

Is Your FIA Safe? Understanding State Guaranty Associations

An FIA is only as strong as the insurer backing it. These are insurance contracts, so safety depends heavily on the financial strength of the issuing company. That’s why insurer ratings matter. In the U.S., state guaranty associations may provide a backstop if an insurer fails, subject to state-specific rules and limits. That protection helps, but it shouldn’t replace careful insurer selection. A safe FIA starts with a financially strong carrier, not just an attractive illustration.

Conclusion

So, what is an FIA investment really? It’s a protected-growth retirement tool that can work well for the right person, but only when the buyer understands the hidden limits. A fixed index annuity can provide tax deferral, downside protection, and a path to future income, but it also brings surrender charges, capped returns, and contract complexity.

Before you sign, check the current cap, participation rate, spread, surrender schedule, and rider costs. Those details determine whether an FIA is genuinely useful or just sounds reassuring on paper.

Related Articles

Annuity News & Rate Forecasts: Is Now the Time for a Fixed Annuity?