If you’ve been asking what is recasting a mortgage, you’re probably in a very specific situation. You have a lump sum of cash, you want lower monthly payments, but you don’t want to give up the low rate already attached to your home loan. That’s exactly where principal curtailment becomes powerful. Instead of refinancing into a brand new mortgage, recasting lets you reduce your balance and keep the loan you already fought to get.

For homeowners sitting on a strong rate from a better market, that matters a lot. A mortgage recast can reduce monthly pressure without restarting the clock or paying full refinance closing costs. It’s one of the most overlooked ways to create breathing room in a budget while keeping the structure of the original loan intact.

The Definition: What Does It Mean to Recast a Loan?

A recast loan is a mortgage that has been recalculated after you make a large lump sum payment toward the principal. The lender then takes the new, lower balance and reamortize the remaining payments across the rest of the original term.

That sounds technical, but the plain English version is simple. You send in a big principal payment, your lender updates the math, and your required monthly payment drops. Your interest rate stays the same. Your payoff date stays the same. The loan itself doesn’t become new. The lender simply recalculates your existing schedule based on the reduced balance.

This is why recasting mortgage strategies appeal to homeowners who like their current rate but want more monthly flexibility. You aren’t replacing the mortgage. You’re adjusting the payment structure after lowering the amount owed.

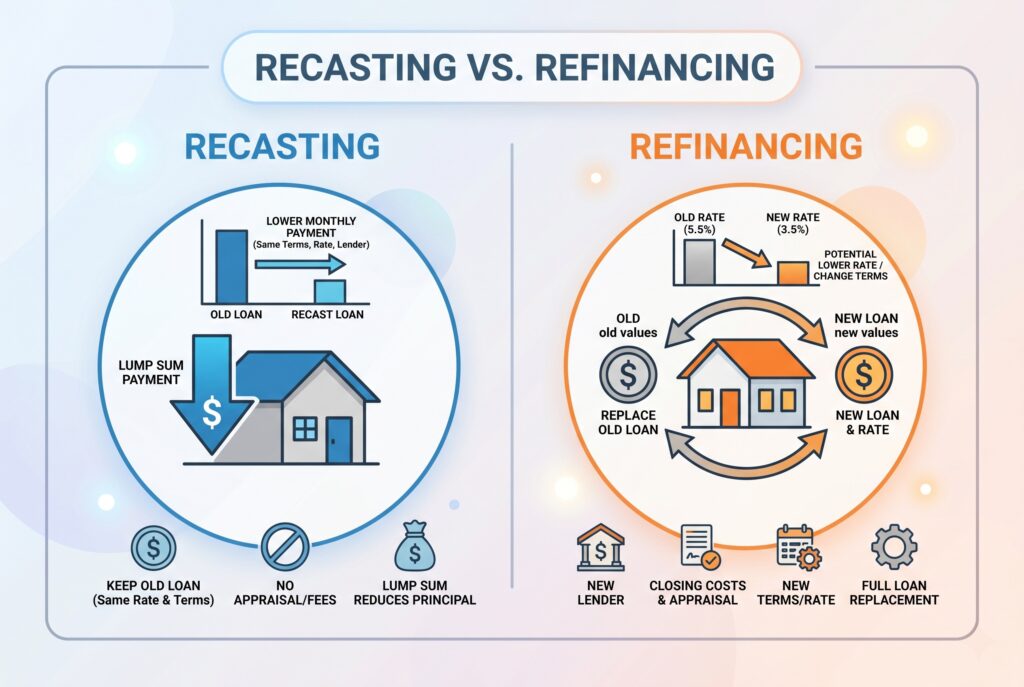

Recasting vs. Refinancing: The Ultimate Strategy

This is where a lot of homeowners make the wrong comparison at first. They assume that if they want a lower monthly payment, the only answer is refinancing. But in many cases, recasting mortgage options is the smarter move.

Refinancing means replacing your current mortgage with a brand new one. That usually comes with fresh underwriting, a new rate, and closing costs that can run into the thousands. If today’s mortgage rates are higher than the rate you already have, refinancing can actually solve one problem while creating another.

A mortgage recast works differently. Instead of trading out your old loan, you keep your current rate and current term. You make a lump sum payment, pay a smaller administrative fee, and let the lender lower your payment by recalculating the remaining schedule. In many cases, that fee is only a few hundred dollars instead of the much larger cost of refinancing.

That makes recasting mortgage decisions especially attractive in a higher-rate environment. If your existing loan sits at a historically low rate, protecting it becomes part of the strategy.

Recasting vs. Extra Principal Payments

This is one of the biggest points of confusion around a mortgage recast. If you simply send your lender an extra $20,000 and do nothing else, your monthly payment usually won’t change. What changes is the speed of your payoff. You’ll reduce interest over time and shorten the life of the loan, but the required payment on your statement generally stays the same.

That’s where principal curtailment by itself differs from a formal recast. A principal payment alone helps you pay off the home faster. A principal payment combined with an official recast is what tells the lender to reamortize the balance and lower the required monthly bill.

This difference matters because the goal isn’t always the same. Some homeowners want to get debt-free as fast as possible. Others want to free up monthly cash flow. If your goal is a lower payment, you usually need the formal mortgage recast process, not just an informal extra payment.

See Your Savings: The Mortgage Recast Calculator

Recast Calculator

Find out your new monthly payment and interest savings after recasting your mortgage.

Your Recast Results

Before requesting a recast, it helps to estimate what the payment change might look like. That’s why so many homeowners search for a mortgage recast calculator, a recast mortgage calculator, or simply a recast calculator.

The basic inputs are straightforward. You need your current mortgage balance, your interest rate, the remaining term, and the lump sum you plan to apply. Once those numbers are adjusted, you can estimate how much lower your new monthly payment may be after the lender recalculates the schedule.

This step is important because a mortgage recast calculator helps you decide whether the payment drop is worth using your cash this way. For some people, the savings are substantial and immediate. For others, the result is useful but not dramatic enough to justify locking up liquidity in the house. That’s why the calculator stage matters. It moves the decision from theory to actual numbers.

How to Qualify: Can Any Mortgage Be Recast?

Not every mortgage can be recast, so this step matters before you get too far into the idea. In general, most conventional loans are the strongest candidates for a mortgage recast. That includes many loans backed by Fannie Mae or Freddie Mac. On the other hand, government-backed loans like FHA, VA, and USDA loans generally don’t allow recasting in the same way.

Lenders also tend to require a minimum lump sum payment before they’ll process the request. That minimum varies, but it’s often at least $5,000 or a percentage of the remaining balance. Some lenders are more flexible than others, and some don’t offer recasting at all.

This is why the best next step is always contacting your servicer directly. Ask whether your current loan is eligible, what minimum payment is required, and what fee applies.

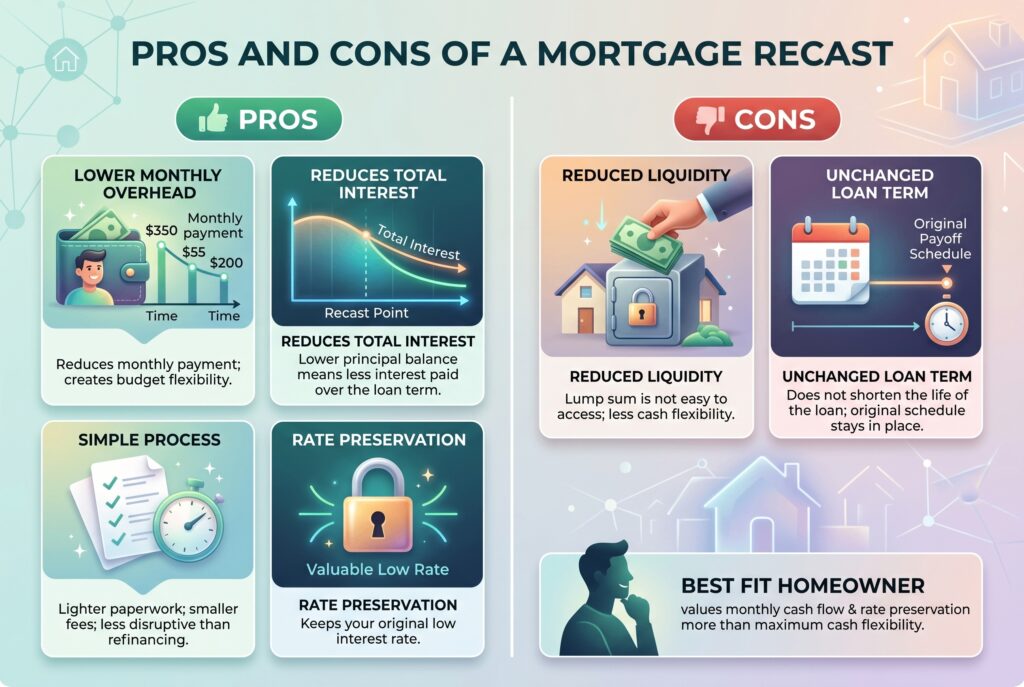

Pros and Cons of a Mortgage Recast

A mortgage recast has clear strengths, but it isn’t perfect for everyone. The biggest benefit is lower monthly overhead. If you want more room in your budget without giving up a valuable low rate, recasting can be an elegant solution. It also reduces total interest over the life of the loan because the principal balance is lower from that point forward.

Another major advantage is simplicity. Compared with refinancing, the paperwork is usually lighter, the fee is smaller, and the process can feel much less disruptive.

The downside is liquidity. Once you push that lump sum into the mortgage, the money isn’t easy to access again. You’ve strengthened your balance sheet, but you’ve also reduced your cash flexibility. A mortgage recast also doesn’t shorten the term of the loan the way aggressive extra principal payments can. It lowers the payment, but it keeps the original payoff schedule in place. That means the best fit is usually a homeowner who values monthly cash flow and rate preservation more than maximum flexibility with cash on hand.

Conclusion

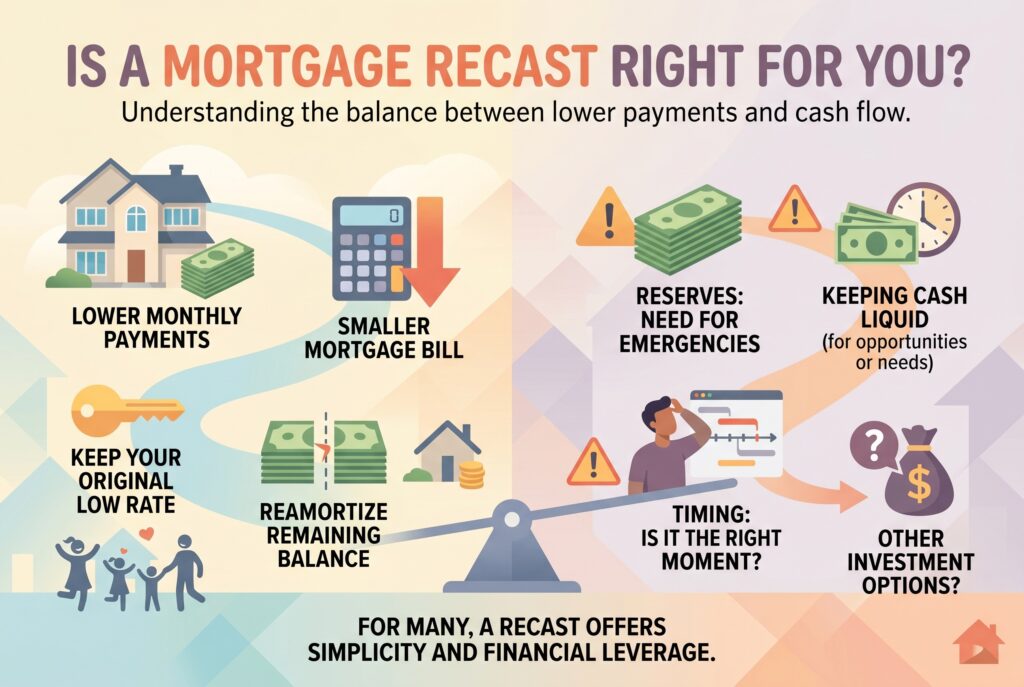

If you have a lump sum available and want lower payments without sacrificing a low interest rate, a mortgage recast can be one of the smartest moves available. It lets you use principal curtailment strategically, keep your original loan, and reamortize the remaining balance into a more manageable monthly obligation.

That doesn’t mean it’s automatically the right answer. You still need to think about reserves, timing, and whether keeping cash more liquid matters more right now. But for many homeowners, especially those sitting on a great rate they don’t want to lose, recasting mortgage options offer a rare combination of simplicity and financial leverage.

If the idea fits your situation, the next step is simple. Contact your loan servicer, ask whether your mortgage qualifies, request the recast paperwork, and run the numbers with a mortgage recast calculator before you commit.