If you want to reamortize your mortgage without giving up a low rate, a recast loan may be one of the smartest moves available. A lot of homeowners are sitting on older mortgages with rates they don’t want to lose, but they still want lower monthly payments. That’s exactly why recasting mortgage strategies matter right now. Instead of replacing your loan, you make a large principal payment and ask the lender to recalculate the payment on the balance that remains.

This matters because high-rate environments change the math. Refinancing can lower your payment in some cases, but it can also force you into a much higher interest rate than the one you already have. A mortgage recast works differently. It lets you keep the old rate, keep the same loan term, and lower the required payment by changing the amortization math after a lump sum payment.

What Is Recasting a Mortgage? The Power of Principal Curtailment

What is recasting a mortgage in plain English? It means you make a large lump sum payment toward your principal balance, and then your lender recalculates the loan over the rest of the original term. That process is why people use the word reamortize. The balance drops, the lender updates the payment schedule, and your monthly payment becomes lower.

This is where principal curtailment becomes important. Principal curtailment is the banking term for making a direct reduction to the loan balance. But by itself, that doesn’t always lower your monthly bill. The lower payment happens when the lender formally processes the recast and reamortizes the remaining balance. That distinction matters. A mortgage recast doesn’t change your interest rate. It doesn’t create a new loan. It doesn’t extend your payoff date either. It simply recalculates your required payment using a lower principal amount and the same remaining timeline.

Recast Loan vs. Refinancing: The 2026 Strategy Guide

A recast loan and a refinance can both reduce monthly pressure, but they solve the problem in very different ways. Refinancing replaces your entire mortgage with a new one. That means new underwriting, new closing costs, and a new interest rate based on today’s market. If your current mortgage rate is much lower than current rates, refinancing can easily become the more expensive choice, even if the monthly payment looks better at first.

A mortgage recast usually works better when the rate you already have is a major asset. You keep that older low rate and avoid the full reset that comes with refinancing. In most cases, the lender charges only a modest administrative fee rather than thousands in closing costs.

That’s why recasting mortgage strategies are so attractive for homeowners with strong older loans. If your current rate is something you’d never want to replace, recasting protects it. Refinancing doesn’t. The tradeoff is simple. Refinancing changes the entire loan. Recasting changes the payment on the same loan.

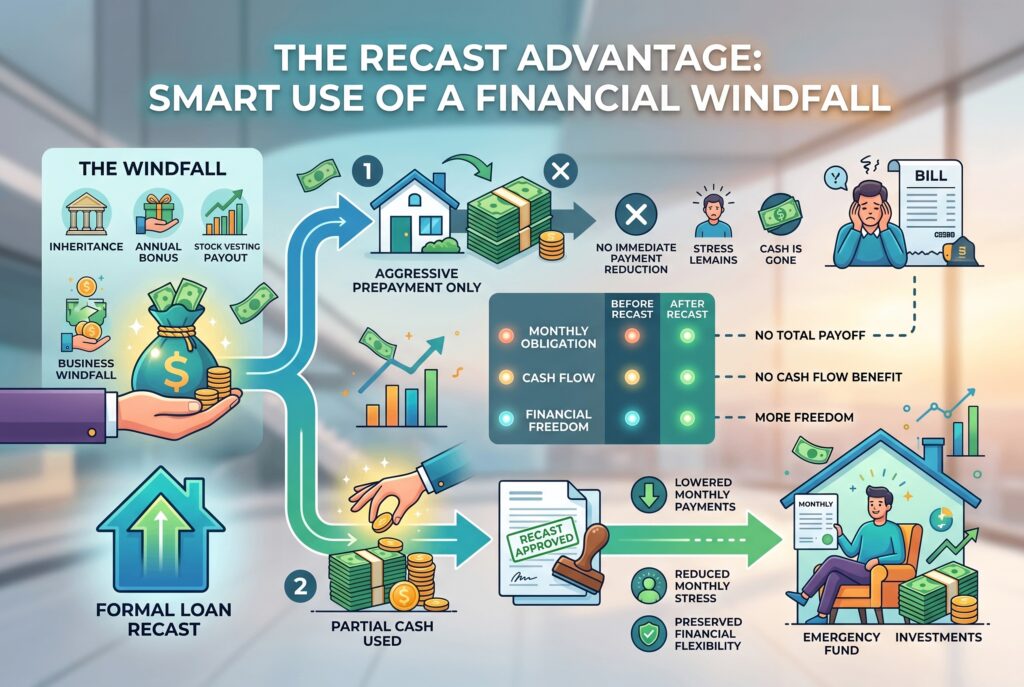

Real World Scenarios: When Does It Make Sense to Reamortize?

A mortgage recast makes the most sense when a homeowner suddenly has access to a large lump sum and wants lower fixed overhead.

One common situation is the buy before you sell strategy. A homeowner buys a new house before the old one sells, so they make a smaller down payment than they originally planned. Once the previous home sells, they use the sale proceeds to make a big principal payment and then reamortize the new mortgage. That lowers the monthly payment to a much more comfortable level without replacing the low rate they already secured.

Another common example is an inheritance, annual bonus, stock vesting payout, or business windfall. In that case, the homeowner doesn’t necessarily want to eliminate the mortgage entirely. They want to use part of the cash to reduce monthly obligations while preserving flexibility in the rest of their finances.

This is where a recast loan can feel more practical than just prepaying aggressively. If the goal is lower monthly stress, the formal recast matters more than simply sending extra money to principal and hoping the payment changes on its own.

Crunching the Numbers: Use a Mortgage Recast Calculator

Recast Calculator

Find out your new monthly payment and interest savings after recasting your mortgage.

Your Recast Results

Before asking your lender for a recast, it helps to test the numbers first. That’s where a mortgage recast calculator becomes useful. A good recast calculator or recast mortgage calculator helps you estimate the new payment after a lump sum reduction. The main inputs are simple. You need your current loan balance, your remaining term in months, your interest rate, and the amount you plan to pay toward principal.

This matters because the results can vary more than people expect. A very large lump sum can create a meaningful drop in monthly payment. A smaller payment may still help, but not enough to justify using that much cash.

Using a mortgage recast calculator also helps you compare the decision against other uses for the money. You may decide the lower payment is worth it. Or you may realize you’d rather keep more liquidity and simply make targeted principal payments without formally recasting. The calculator phase turns the idea from a concept into a decision.

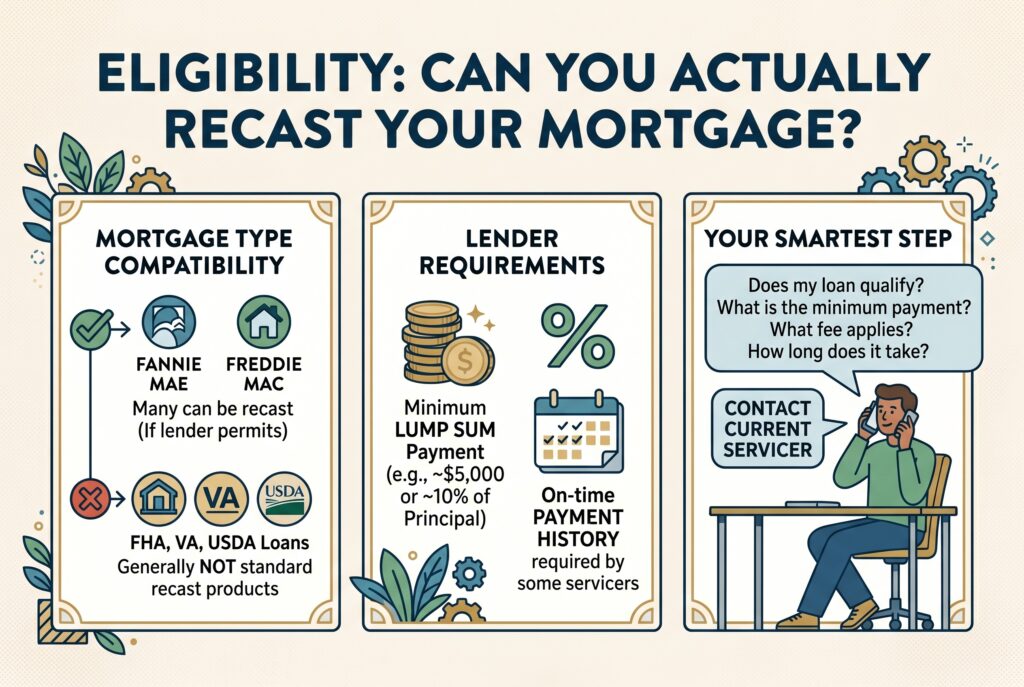

Eligibility: Can You Actually Recast Your Mortgage?

Not every borrower can recast, and not every loan allows it. In general, conventional mortgages are the best candidates. Many loans backed by Fannie Mae or Freddie Mac can be recast if the lender permits it. Government-backed loans usually don’t work the same way. FHA, VA, and USDA loans generally aren’t treated as standard mortgage recast products.

Lenders also tend to impose minimum requirements. In many cases, you’ll need a minimum lump sum payment, often around $5,000 or sometimes closer to 10% of the unpaid principal balance. Some servicers also require a history of on-time payments before they’ll approve the request.

This is why the smartest step is always contacting your current servicer directly. Ask whether your loan qualifies, what minimum payment is required, what fee applies, and how long the recast process usually takes.

Conclusion

If you’re cash rich but rate protective, reamortizing your mortgage through a recast loan can be one of the cleanest ways to lower your monthly payment without making a major financing mistake. It keeps the loan you already have, preserves the interest rate you probably don’t want to lose, and uses principal curtailment strategically instead of emotionally.

For the right homeowner, that makes mortgage recast decisions much more than a technical option. It becomes a practical tool for preserving a low rate while giving your monthly budget more room to breathe. If that sounds like your situation, the next move is straightforward. Run the numbers with a mortgage recast calculator, review your cash reserves honestly, and contact your loan servicer to ask for the paperwork needed to request a recast.