Understanding a company’s debt capacity isn’t as simple as looking at how much debt it has. A business can carry a large loan balance and still be financially healthy if its operations generate enough earnings to cover interest payments comfortably. At the same time, a company with less debt can still be risky if its profits are too weak to meet basic interest obligations.

That is why the times interest earned ratio formula matters. Also called the TIE ratio or interest coverage ratio, this solvency metric helps investors, lenders, business owners, and finance students answer one direct question: can this company pay interest from operating earnings without strain?

In this guide, we will break down the times interest earned ratio, explain the difference between EBIT and cash flow, walk through clear times interest earned ratio examples, and show how to interpret a good or bad result in 2026.

Times Interest Earned Ratio Formula

The times interest earned ratio formula is calculated by dividing Earnings Before Interest and Taxes by total interest expense.

For example, if a company has EBIT of $5 million and interest expense of $1 million, its TIE ratio is 5.0x. That means the company earns five times enough operating profit to cover its current interest bill. In general, a ratio above 2.5x is often viewed as more comfortable, while a ratio near 1.0x can signal financial stress.

What Is the Times Interest Earned Ratio?

The times interest earned ratio measures how many times a company can cover its interest expense using operating profit. It’s a key solvency metric because it focuses on the relationship between earnings and debt obligations.

Lenders use the TIE ratio to judge whether a borrower has enough operating strength to handle interest payments. Investors use it to evaluate creditworthiness, debt capacity, and financial risk. Business owners use it to understand whether taking on more debt would be safe or dangerous. A higher times interest earned ratio usually means stronger financial flexibility. A lower ratio suggests the company has less room for error if sales decline, margins shrink, or interest rates rise.

Why the Interest Coverage Ratio Matters

The interest coverage ratio matters because interest payments aren’t optional. A company can delay expansion, reduce marketing, or cut discretionary spending, but it must still pay lenders on time. When the TIE ratio is strong, the business has breathing room. It can absorb temporary downturns, reinvest in operations, or negotiate better lending terms. When the ratio is weak, even a small decline in EBIT can create pressure. This is why creditors care about TIE before approving new loans. The ratio not only shows whether a company is profitable, but also whether that profit is large enough to support debt.

How to Calculate Times Interest Earned Step by Step

Start by finding EBIT on the income statement. EBIT stands for Earnings Before Interest and Taxes. It reflects operating earnings before financing costs and tax expenses. Next, find total interest expense for the same period. This includes interest paid or accrued on loans, bonds, credit lines, and other debt instruments. Then divide EBIT by interest expense.

If EBIT is $3 million and interest expense is $750,000, the calculation is:

A TIE ratio of 4.0x means the company generated four dollars of operating profit for every one dollar of interest expense.

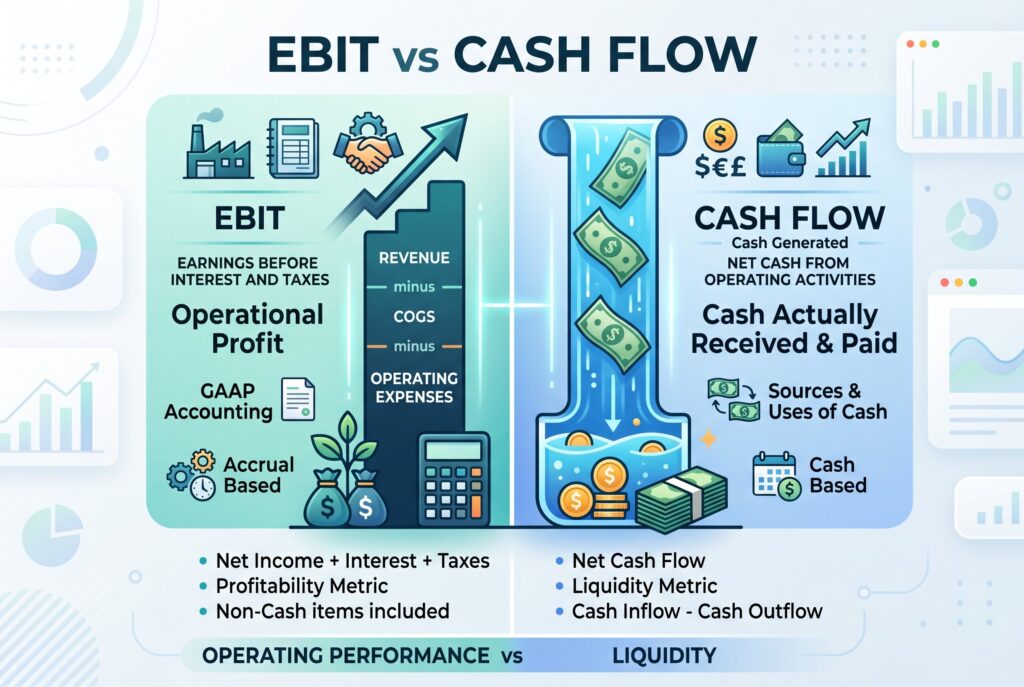

The Dangerous Flaw: EBIT vs Cash Flow

The biggest limitation of the times interest earned ratio formula is that it uses EBIT, not actual cash flow. This distinction is critical.

EBIT is an accounting profit measure. It can include revenue that has been earned but not yet collected in cash. A company may report strong EBIT while customers are slow to pay invoices. Another company may show healthy operating earnings but have cash trapped in inventory.

That means a high TIE ratio doesn’t always guarantee strong liquidity. A business can appear safe on paper but still struggle to make payments if cash conversion is poor. This is why analysts often pair TIE with operating cash flow, free cash flow, EBITDA coverage, and debt service coverage ratio.

Times Interest Earned Ratio Example 1: Tech Startup

Imagine a fast growing software company with EBIT of $10 million and annual interest expense of $500,000.

This company has a very strong TIE ratio. It can cover interest expense twenty times using operating profit. Lenders would likely view this as a low credit risk, assuming the earnings are stable and cash collection is healthy. However, analysts should still check whether growth depends on heavy spending, customer concentration, or delayed receivables.

Times Interest Earned Ratio Example 2: Manufacturing Firm

Now consider a manufacturing company with EBIT of $5 million and interest expense of $1.5 million.

A TIE ratio of 3.3x is generally healthy. It suggests the company can cover interest obligations with a reasonable cushion. Still, manufacturing businesses often face inventory costs, equipment spending, and cyclical demand. Because of that, analysts should review cash flow and capital expenditure needs before assuming the company has unlimited debt capacity.

Times Interest Earned Ratio Example 3: Retail Chain in Trouble

A struggling retail chain has EBIT of $2 million and interest expense of $2.5 million.

This is a warning sign. A TIE ratio below 1.0x means the company doesn’t generate enough operating profit to cover interest expense. Unless conditions improve, it may need to refinance debt, sell assets, cut costs, raise capital, or restructure. This is the kind of scenario that makes lenders nervous because there is no earnings cushion.

What Is a Good Times Interest Earned Ratio?

A good times interest earned ratio depends on the industry. Stable utility companies may operate safely with a lower ratio because revenue is predictable. A TIE ratio around 2.0x may be acceptable in certain regulated industries.

More volatile companies usually need a higher ratio. Tech hardware, retail, construction, and cyclical manufacturing businesses may need 4.0x or 5.0x to look safe because earnings can shift quickly. As a general rule, 1.0x or lower is risky, 2.0x to 3.0x is moderate, and above 4.0x is more comfortable. But context matters more than one number.

How to Improve the TIE Ratio

A company can improve its times interest earned ratio in two main ways: increase EBIT or reduce interest expense. To increase EBIT, management can raise prices, improve margins, reduce operating costs, increase sales volume, or exit unprofitable product lines. To reduce interest expense, the company can refinance at a lower rate, repay debt, renegotiate terms, or avoid taking on unnecessary borrowing. The best improvements are sustainable. Cutting essential spending may improve EBIT temporarily, but it can damage long term growth.

Finance Interview Cheat Sheet: How to Explain TIE

If asked in a finance interview, keep the explanation simple and precise. The times interest earned ratio shows how many times a company’s EBIT can cover interest expense. A TIE ratio of 1.5x means the company covers interest only one and a half times, leaving little room for a downturn. I would then check operating cash flow to confirm whether those earnings are converting into real cash. That answer shows you understand both the formula and its limitations.

Conclusion

The times interest earned ratio formula is a powerful starting point for credit analysis, investment research, and business debt planning. It tells you whether operating earnings are strong enough to cover interest obligations and whether the company has room to handle financial pressure. But the ratio should never be used alone. EBIT isn’t the same as cash flow, and debt safety depends on liquidity, repayment schedules, margins, industry stability, and future earnings risk.

The smartest analysis starts with the TIE ratio, then goes deeper. Look at trends over time, compare industry peers, review cash flow, and ask whether the company could still cover interest if earnings declined. That is how the times interest earned ratio becomes more than a formula. It becomes a practical test of financial resilience.