If you want to give your child a serious financial head start, time matters more than almost anything else. A small investment made while a child is young can have decades to grow, and that is what makes a custodial Roth IRA so powerful.

A Roth IRA for kids isn’t a loophole or a special child-only account. It’s a Roth IRA opened and managed by an adult custodian for a minor who has legitimate earned income. The account can grow tax-free, and qualified withdrawals in retirement can also be tax-free.

Can I open a Roth IRA for my child? Yes, if your child has documented earned income. For 2026, the IRA contribution limit is $7,500 or the child’s taxable compensation for the year, whichever is lower. The adult manages the custodial Roth IRA until the child reaches the age of majority, usually 18 or 21 depending on the state.

Understanding the Math: Why Starting Early Matters

The biggest advantage of a child Roth IRA isn’t the first contribution, but the gift of time. A teenager who invests even a small amount can benefit from 40 to 50 years of tax-free compounding. Money invested at age 15, for instance, has decades more to grow than money first invested at age 35. Over time, even modest earnings from a summer job can turn into substantial retirement savings. More importantly, starting early helps children see investing not as something to do “someday,” but as a lifelong habit.

The Golden Rule: What Counts as Earned Income?

The strict rule is simple: the child must have earned income. Allowance for normal household chores doesn’t count. W-2 income qualifies, such as working as a lifeguard, retail employee, restaurant worker, camp counselor, or barista. Self-employment income may also qualify, such as babysitting, lawn mowing, tutoring, pet sitting, or dog walking. Family business wages can qualify too, but they must be reasonable, documented, and paid for real work. Paying a child an inflated wage just to fund a Roth IRA can create tax trouble.

2026 Contribution Limits and the Parent Match Strategy

For 2026, the maximum IRA contribution is $7,500, but a child can’t contribute more than they earned. If your child earns $2,000, the maximum contribution is $2,000, not $7,500. The contribution doesn’t have to come from the child’s exact dollars. If your child earns $2,000 lifeguarding, you can let them keep their paycheck and contribute $2,000 of your own money into the custodial IRA. This “parent match” keeps the child motivated while still building long-term wealth.

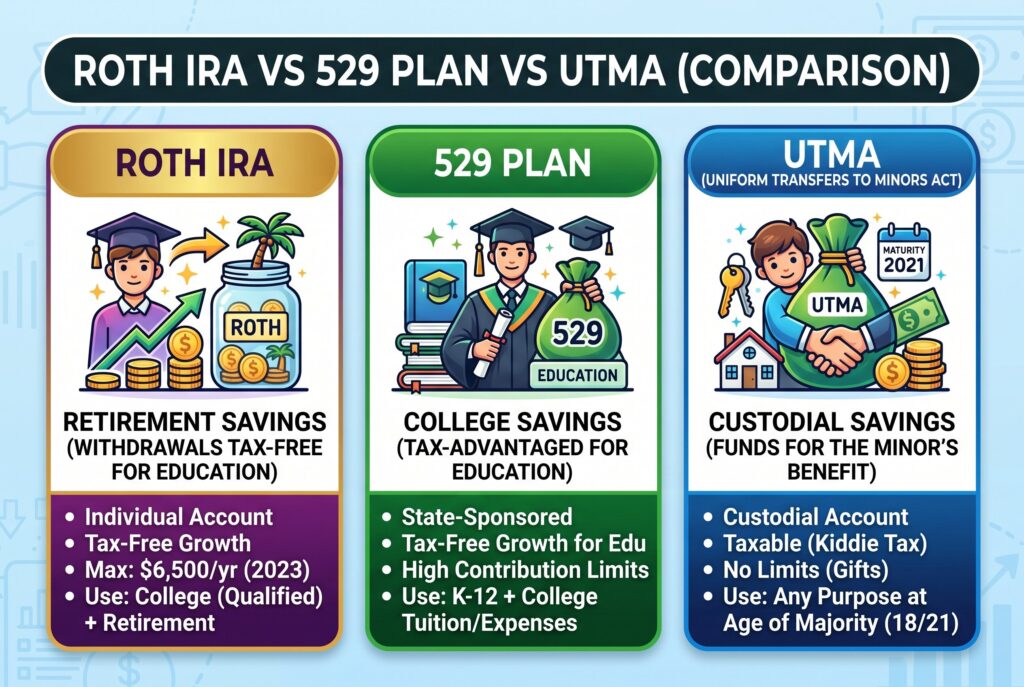

Roth IRA vs 529 Plan vs UTMA: Which Is Best?

A 529 plan is best when the goal is education savings. It doesn’t require earned income and can offer tax advantages for qualified education expenses.

A custodial Roth IRA is best when the child has earned income and the goal is long-term investing, retirement savings, and some withdrawal flexibility. Contributions can generally be withdrawn, but earnings have stricter rules.

A UTMA or UGMA account is more flexible because the money can be used for many purposes, but it may have a stronger impact on financial aid and becomes the child’s asset when they reach adulthood.

Step by Step Setup Guide: How to Open the Account

- First, choose a low-cost broker that offers custodial Roth IRAs. Fidelity, Schwab, Vanguard, and similar major platforms are common options.

- Second, gather information for both the custodian and child, including Social Security numbers, birthdates, addresses, and banking details.

- Third, open the custodial IRA and fund it up to the allowed amount.

- Fourth, invest the money. A Roth IRA is only the account. If you leave the cash uninvested, it may not grow meaningfully. Many families choose broad index funds or target-date funds, depending on risk tolerance.

Tax Documentation: Keeping the IRS Happy

Documentation matters most when the child has self-employment income. If they babysit, mow lawns, tutor, or walk dogs, keep a simple income log. Record the date, service, client name, amount paid, and payment method. Save invoices, bank deposits, or written confirmations when possible. If the child earns enough from self-employment, they may need to file a tax return and pay self-employment tax. W-2 income is easier because the employer creates the paper trail, but parents should still keep pay stubs and year-end tax forms.

The FAFSA Impact: Will This Hurt College Financial Aid?

Retirement accounts such as Roth IRAs are generally not reported as assets on the FAFSA, which can make them more aid-friendly than some taxable custodial accounts. However, withdrawals during college can create problems. If the child takes money out while applying for aid, that withdrawal may be treated as income and could reduce future financial aid eligibility. Because of that, avoid using the Roth IRA casually during college years unless you understand the aid impact.

Conclusion

A custodial Roth IRA for kids isn’t just about retirement. It’s about teaching investing, documenting earned income properly, and giving compounding decades to work. The rules are simple but strict: your child needs real earned income, contributions can’t exceed the 2026 limit or earned income, and the account should be invested thoughtfully. Used well, a Roth IRA for minors can turn small early earnings into lifelong financial confidence.