Is depreciation an operating expense? Usually, yes. Depreciation expense is generally treated as an operating expense when the asset is used in daily business operations. That may include office computers, delivery vehicles, furniture, equipment, or buildings used to run the company.

The important detail is classification. Depreciation isn’t always placed in the same account. Depending on how the asset is used, depreciation expense may appear in COGS, SG&A, or even as a non-operating expense. These days, getting this right matters because it affects gross profit, operating income, EBITDA, lender confidence, and financial reporting accuracy.

Interactive Tool: The Depreciation Classifier & EBITDA Calculator

Use this simple decision flow:

Question 1: Does the asset help make or deliver the product?

If yes, depreciation may belong in COGS.

Question 2: Does the asset support sales, admin, or office operations?

If yes, depreciation likely belongs in SG&A.

Question 3: Is the asset outside normal business activity?

If yes, depreciation may be non-operating.

Now connect it to EBITDA:

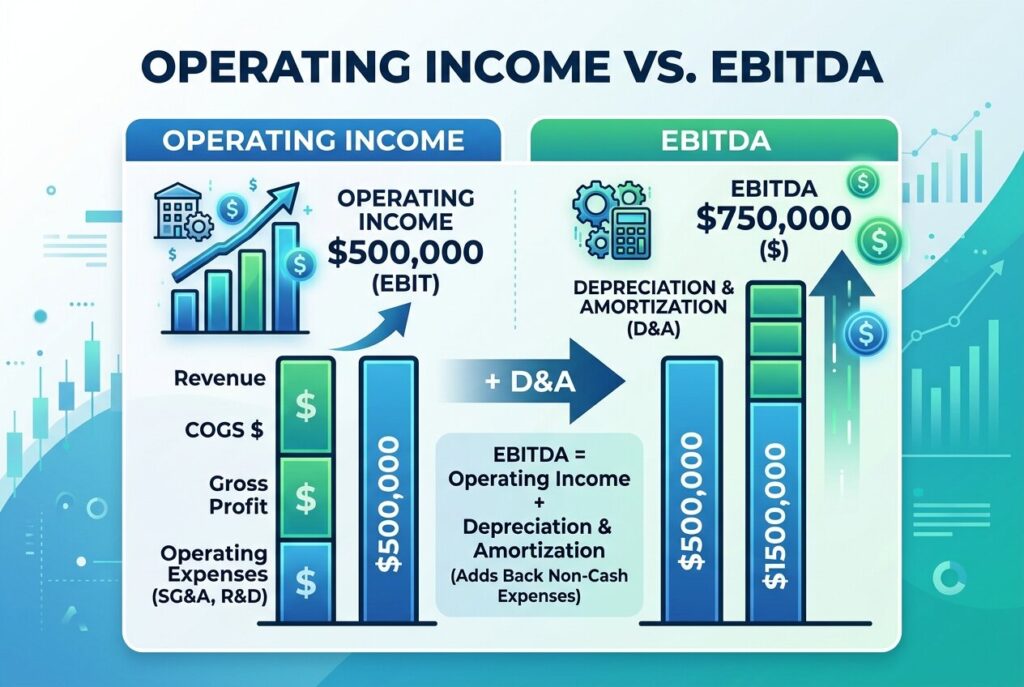

EBITDA = Operating Income + Depreciation + Amortization

Example:

Revenue: $800,000

COGS: $350,000

SG&A: $220,000

Depreciation Expense: $30,000

Operating Income: $200,000

EBITDA = $200,000 + $30,000 = $230,000

This shows why depreciation matters. It lowers operating income, but because it’s a non-cash expense, analysts add it back when evaluating cash-generating power.

Depreciation Classifier & EBITDA Calculator

The 3 Ways to Classify Depreciation Expense

1. Depreciation as COGS

Depreciation belongs in COGS when the asset is directly involved in production or service delivery. This is common in manufacturing, printing, logistics, and asset-heavy service businesses. Examples include factory machines, production equipment, manufacturing tools, and certain delivery assets used directly to fulfill customer orders. This classification affects gross margin. If production equipment depreciation is placed in COGS, gross profit becomes lower. That may be accurate, but it also means your product margins look tighter.

2. Depreciation as SG&A

SG&A stands for selling, general, and administrative expenses. This is the most common home for depreciation expense when the asset supports business overhead rather than production. Examples include office laptops, office furniture, headquarters equipment, sales team vehicles, accounting software servers, and administrative systems. If a marketing team uses laptops, the depreciation usually belongs in SG&A. If executives use office equipment, that depreciation also belongs in SG&A. These assets help run the business, but they don’t directly create inventory or deliver the core service.

3. Depreciation as a Non-Operating Expense

Depreciation may be non-operating when the asset isn’t part of normal business activity. For example, if a company owns an empty building that’s being held for sale and it isn’t used in operations, depreciation related to that building may be non-operating. The same may apply to assets connected to discontinued operations or side investments. This classification prevents non-core assets from distorting operating performance.

Why Lenders Care About Your Depreciation Classification

Lenders look closely at profitability, repayment capacity, and margin quality. Depreciation classification can influence all three. If too much depreciation is pushed into COGS, gross margin may look weaker. That can make the business appear less efficient at producing goods or delivering services. On the other hand, if production-related depreciation is moved into SG&A, gross margin may look artificially strong.

Neither result is ideal. Lenders want consistent, credible financial statements. Clean depreciation classification helps show the true economics of the business. For loan applications, precision can strengthen your story. It shows that management understands costs, tracks asset use, and can explain operating performance clearly.

Operating Income vs. EBITDA: The Add-Back Secret

Depreciation is a non-cash expense. That means it reduces accounting profit, but it doesn’t represent cash leaving the business during the current period. Operating income includes depreciation. If depreciation rises, operating income falls.

EBITDA treats depreciation differently. It adds depreciation and amortization back to earnings to estimate operating cash-generating power before non-cash charges, interest, taxes, and capital structure effects. This is why EBITDA vs operating income matters. Operating income shows profit after depreciation. EBITDA shows profit before depreciation and amortization. Both are useful, but they answer different questions.

Operating income tells you how profitable operations are under accounting rules. EBITDA helps investors, buyers, and lenders understand cash flow potential.

Where Does Depreciation Appear on Financial Statements?

On the income statement, depreciation appears inside COGS, SG&A, or another expense category depending on asset use. Production asset depreciation may be inside COGS. Office asset depreciation may be inside SG&A.

On the cash flow statement, depreciation in cash flow statement reporting appears in cash flows from operating activities. It’s added back to net income because depreciation reduced profit but didn’t use cash in the current period.

On the balance sheet, accumulated depreciation reduces the book value of fixed assets. For example, if equipment costs $100,000 and accumulated depreciation is $40,000, the net book value is $60,000.

Real-World Business Examples

- Manufacturing: A factory buys a CNC machine for $100,000. Since the machine is used to produce goods, its depreciation usually belongs in COGS. This affects gross profit and product-level margin.

- SaaS/Tech: A company owns servers used to deliver its platform. Server depreciation may be part of COGS because the assets support service delivery. But laptops used by the marketing team usually fall under SG&A.

- Real Estate: A rental property business depreciates apartment buildings used to generate rent. Because those buildings are part of core operations, depreciation is treated as an operating expense for that business model.

- Service Business: A consulting company depreciates office furniture and team laptops. These assets support daily operations, so depreciation usually belongs in SG&A.

Conclusion

Depreciation isn’t just a bookkeeping detail. It affects operating expenses, SG&A, gross margin, operating income, EBITDA, and lender perception. The safest rule is to classify depreciation based on how the asset is used.

If the asset supports production, consider COGS. If it supports sales or administration, SG&A is usually right. If it isn’t tied to core operations, non-operating treatment may be more accurate. For best results, work with a CPA to set up a clear chart of accounts from the beginning. Accurate depreciation classification protects your margins, improves reporting quality, and makes your financial statements easier to trust.