")

The quick ratio formula is one of the most useful ways to measure whether a business can handle short term obligations without relying on inventory sales. That’s why the quick ratio is often seen as a stricter test of financial strength than broader liquidity measures. For business owners, finance teams, and investors, it offers a faster look at true liquidity by focusing only on assets that can realistically be turned into cash in the near term. In this guide, we’ll break down the formula, explain what counts as liquid assets, compare it with the current ratio, and walk through practical examples so the concept feels useful instead of abstract.

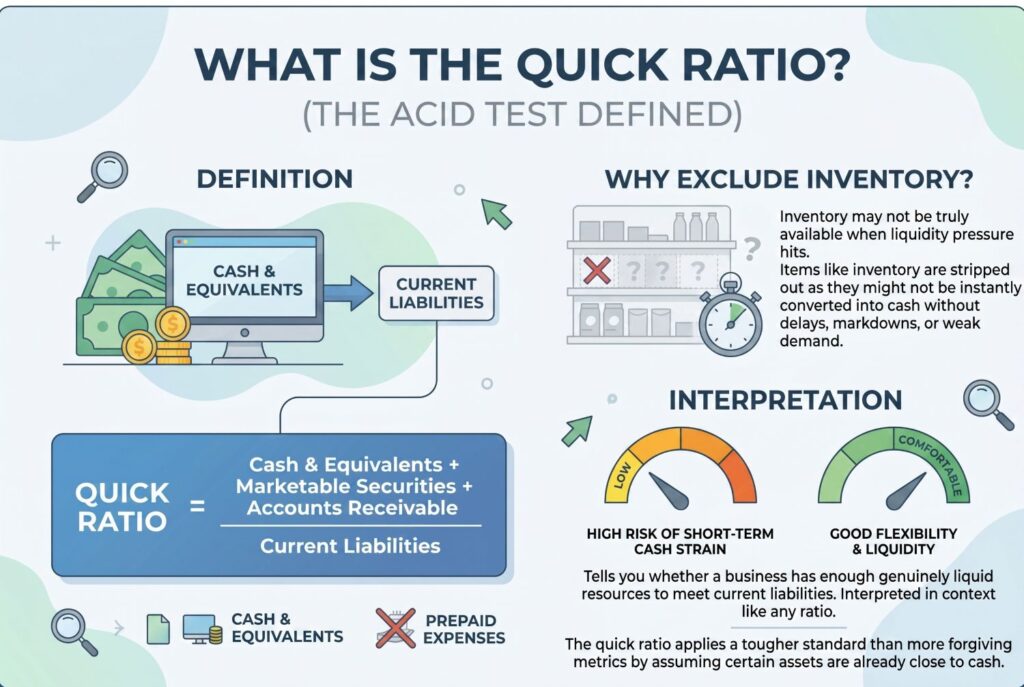

What Is the Quick Ratio? (The Acid Test Defined)

The quick ratio is a liquidity ratio that measures a company’s ability to pay short term liabilities using only its most liquid current assets. It’s also called the acid test ratio because it applies a tougher standard than more forgiving metrics. Instead of assuming inventory can always be sold quickly and at full value, the quick ratio asks a more demanding question: if the business had to cover near term obligations soon, how much could it rely on assets that are already close to cash?

That’s what makes the acid test ratio formula so useful. It strips out items that may look good on a balance sheet but may not be truly available when liquidity pressure hits. Inventory is the clearest example. A retailer may hold plenty of goods, but that doesn’t mean those goods can instantly be converted into cash without markdowns, delays, or weak demand. Prepaid expenses are also excluded because they’re not cash resources the company can use to pay bills.

In simple terms, the quick ratio tells you whether the business has enough genuinely liquid resources to meet current liabilities. If the number is too low, the company may be exposed to short term cash strain. If it’s comfortably strong, the company usually has more flexibility. Still, like any ratio, it only becomes truly meaningful when interpreted in context.

The Quick Ratio Formula: Breaking Down Quick Assets

The quick ratio formula is:

Quick Ratio = Quick Assets / Current Liabilities

Some versions of the formula are written by listing the components individually:

Quick Ratio = (Cash + Cash Equivalents + Marketable Securities + Accounts Receivable) / Current Liabilities

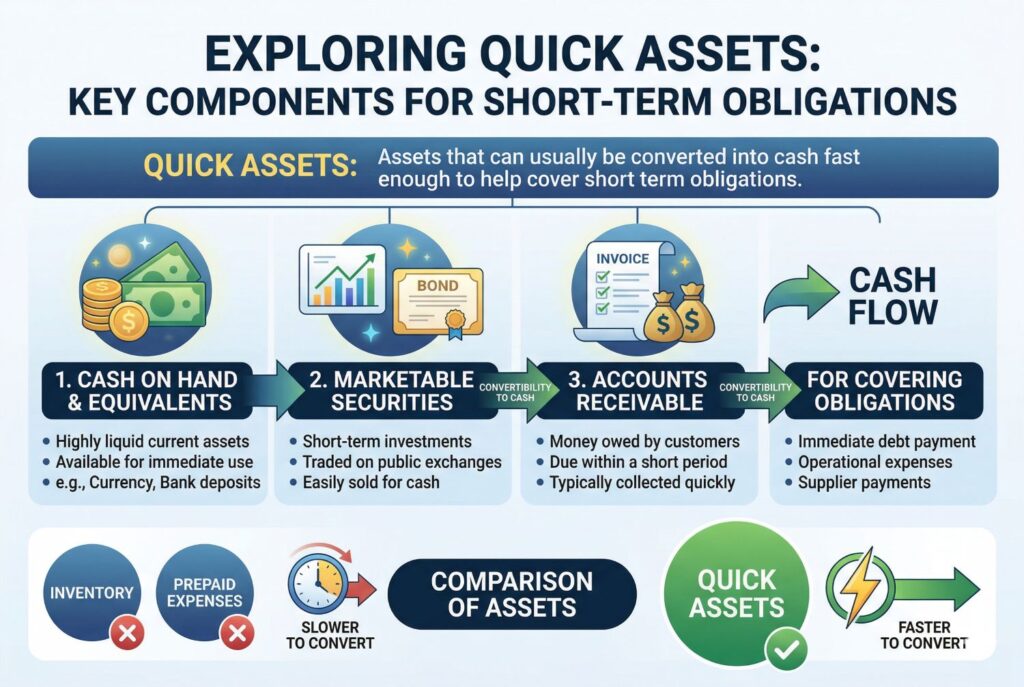

The key term here is quick assets. Quick assets are the assets that can usually be converted into cash fast enough to help cover short term obligations. In most cases, quick assets include cash on hand, cash equivalents, marketable securities, and accounts receivable. These assets are considered more immediately available than inventory or prepaid expenses.

This is where the formula becomes more insightful than a basic liquidity glance. Two companies can have the same total current assets, but very different quick ratios if one is heavily dependent on inventory. That’s why the quick ratio formula is often preferred when users want to understand true short term liquidity rather than just general working capital coverage.

It’s also worth remembering that not all quick assets are equally “quick” in real life. Accounts receivable may look collectible, but some customers pay late. Marketable securities may be liquid, but price volatility can affect how useful they really are in a stressful environment. Good finance content often points out that the quick ratio is helpful, but it still isn’t a perfect mirror of real-time cash access.

Step by Step Calculation: Real World Business Examples

The easiest way to understand the ratio is to calculate it using realistic scenarios.

Example 1: Service Business with Minimal Inventory

Imagine a consulting firm has:

- Cash: $60,000

- Cash equivalents: $15,000

- Accounts receivable: $45,000

- Inventory: $0

- Current liabilities: $80,000

Its quick assets are:

60,000 + 15,000 + 45,000 = 120,000

Now divide quick assets by current liabilities:

120,000 / 80,000 = 1.5

So the quick ratio is 1.5.

That’s a healthy result for a service business. Since the company doesn’t rely on inventory, its quick ratio and current ratio may be fairly close. In this kind of model, the quick ratio is often a very useful measure because most current assets are already close to cash.

Example 2: Retail Business with Heavy Inventory

Now imagine a retail company has:

- Cash: $25,000

- Marketable securities: $10,000

- Accounts receivable: $20,000

- Inventory: $145,000

- Current liabilities: $100,000

Its quick assets are:

25,000 + 10,000 + 20,000 = 55,000

Now divide by current liabilities:

55,000 / 100,000 = 0.55

So the quick ratio is 0.55.

This example shows why the metric matters. On paper, the company may still look reasonably healthy if you include inventory in broader liquidity analysis. But once inventory is removed, the business appears much more exposed. That doesn’t always mean the retailer is in immediate danger. Some retail models operate with lower quick ratios because inventory turns quickly. But it does mean the company has less near term flexibility than the balance sheet first suggests.

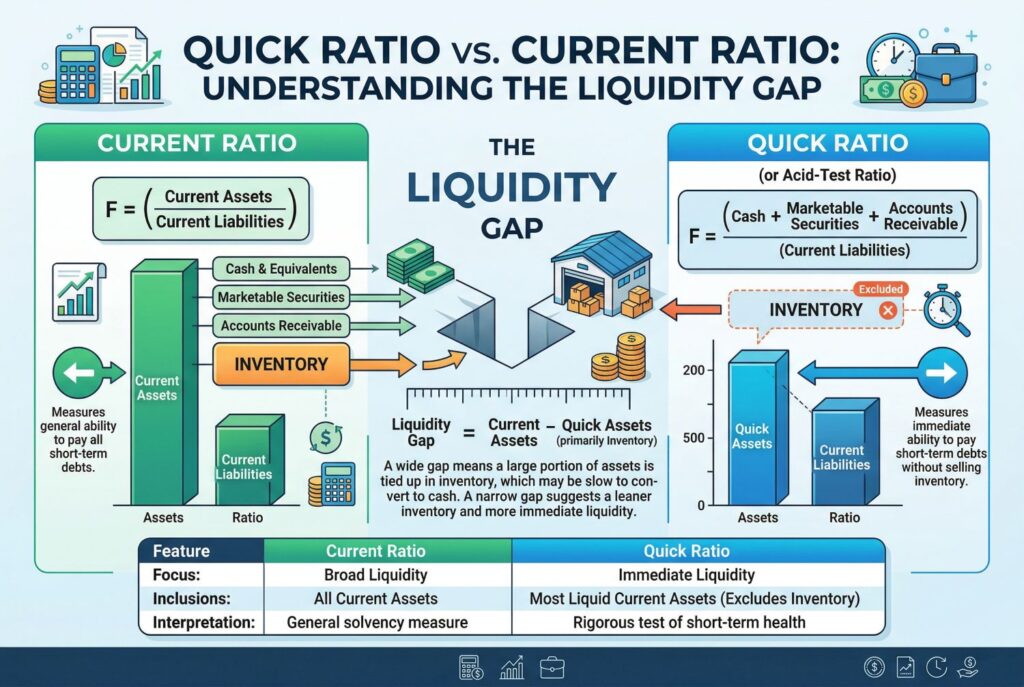

Quick Ratio vs. Current Ratio: Understanding the Liquidity Gap

The quick ratio vs current ratio comparison matters because both ratios measure liquidity, but they do it with different levels of strictness. The current ratio includes all current assets divided by current liabilities. That means it counts inventory and other less liquid current assets. The quick ratio removes inventory and focuses only on assets that are closer to cash. That makes the quick ratio a more conservative measure.

If a company has a large gap between its current ratio and quick ratio, that usually tells you inventory plays a major role in its liquidity picture. For a manufacturer or retailer, that may be normal. For a business with little inventory, the gap should usually be much smaller. So when should you use each one? The current ratio is useful for a broad view of short term coverage. The quick ratio is better when you want a tougher test of whether the company can meet obligations without depending on stock sales.

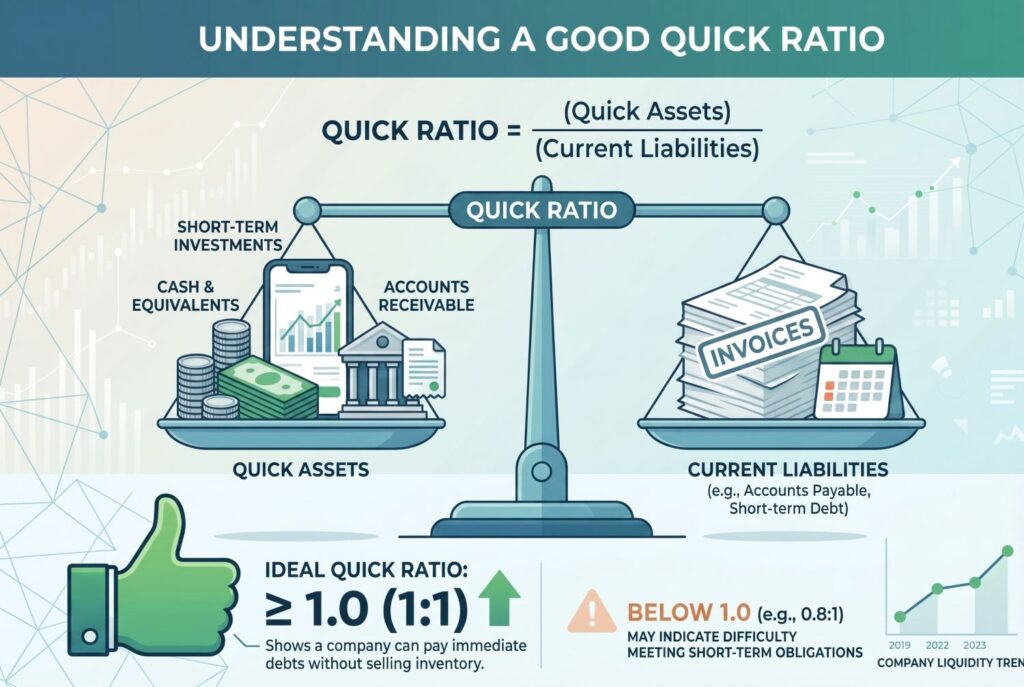

Industry Benchmarks: What Is a Good Quick Ratio?

A ratio of 1.0 or higher is often described as a reasonable benchmark, because it suggests quick assets are enough to cover current liabilities. But a “good” ratio still depends on the industry, operating model, and cash cycle. Several strong source articles note that retail businesses may safely operate lower, while businesses with slower receivable collection or less predictable cash flow may need a bigger cushion.

Here’s a simple benchmark table:

| Industry | Often Acceptable Range | Why It Varies |

|---|---|---|

| Retail | 0.5 to 1.0 | Fast turnover can support lower quick ratios |

| Manufacturing | 0.8 to 1.3 | Inventory matters, but near term cash still matters too |

| Technology / SaaS | 1.0 to 2.0 | Lower inventory reliance often supports stronger liquidity |

| Professional Services | 1.0 to 1.8 | Receivables and cash collection speed are key |

A low ratio can suggest liquidity pressure, but a very high ratio isn’t automatically ideal either. If the number is excessively high, it may mean the company is holding too much idle cash or not deploying capital efficiently. That’s why interpretation should never stop at “higher is better.”

Operational Strategy: How to Improve Your Quick Ratio

This is where many finance explainers get too theoretical. If a business has a weak ratio, it needs practical next steps.

One of the best ways to improve the ratio is to collect receivables faster. If customers pay sooner, more of the company’s resources shift toward cash. Another lever is negotiating better supplier terms, which can reduce short term liquidity pressure by stretching payment timing more effectively. Businesses can also improve the ratio by cutting unnecessary cash outflows, restructuring short term debt where possible, or improving cash forecasting so decisions don’t create avoidable liquidity strain.

For inventory-heavy businesses, improving the quick ratio may also mean reducing overstock and converting stale inventory into cash more efficiently. Even though inventory doesn’t count in the formula, better inventory discipline can still improve real liquidity by freeing working capital and reducing pressure elsewhere.

Conclusion

The quick ratio formula is valuable because it focuses on what a business can actually use to meet short term obligations without leaning on inventory. That’s why the quick ratio remains one of the clearest ways to test true liquidity. It helps business owners, investors, and finance teams look past surface-level current assets and ask a harder, more practical question: how much real flexibility does this company have right now?

Used regularly, the quick ratio can become part of a smarter financial health check. Track it over time, compare it against peers, and pair it with cash flow analysis rather than treating it as a standalone answer. When used that way, the quick ratio formula stops being just a finance definition and becomes a useful decision tool for running a healthier business.