If you’ve ever heard that interest rates moved by 25 basis points and wondered what that actually means, you aren’t alone. Financial jargon can make tiny numbers sound intimidating, but basis points (BPS) are simple once you translate them. One basis point equals 0.01%, which means 100 basis points equals 1%. That’s the core answer to what is a basis point, and it’s why basis points are so useful when comparing mortgage rates, savings yields, bond yields, or investment fees.

Quick facts: BPS meaning is “basis points,” often pronounced “bips.” One basis point is 1 hundredth of 1%. Finance professionals use BPS because they remove confusion when talking about small changes in percentages.

What Does BPS Mean? The Math Explained

BPS means basis points. A basis point is a tiny unit used to measure changes in percentages, especially interest rates and financial fees. If 1% is like a dollar, one basis point is like a penny.

1 BPS equals 0.01%.

10 BPS equals 0.10%.

25 BPS equals 0.25%.

50 BPS equals 0.50%.

75 BPS equals 0.75%.

100 BPS equals 1.00%.

This is the simplest basis points meaning. To convert basis points to percent, divide by 100. To convert a percentage into basis points, multiply by 100. So a 0.25% rate change equals 25 BPS, and a 1.50% change equals 150 BPS.

If you’re searching for a quick tool, a BPS calculator or basis point calculator can help automate these conversions.

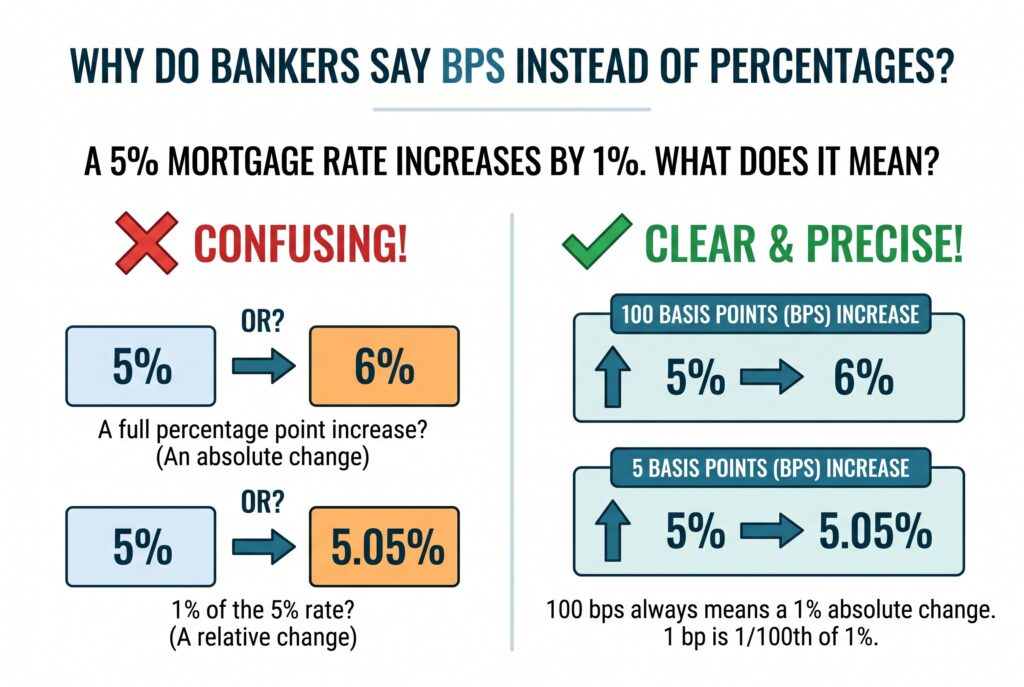

Why Do Bankers Say BPS Instead of Percentages?

Bankers, lenders, investors, and analysts use basis points because percentages can be confusing. Imagine a mortgage rate is 5%. If someone says the rate increased by 1%, that statement can be unclear. Do they mean it moved from 5% to 6%, which is a full percentage point increase? Or do they mean it rose by 1% of 5%, which would move it only slightly to 5.05%?

Saying the rate increased by 100 basis points removes the confusion. It means the rate moved from 5% to 6%. Saying it increased by 5 basis points means it moved from 5% to 5.05%. That precision is why basis points are common in finance news, Federal Reserve updates, bond markets, credit spreads, mortgage pricing, and fund fee comparisons.

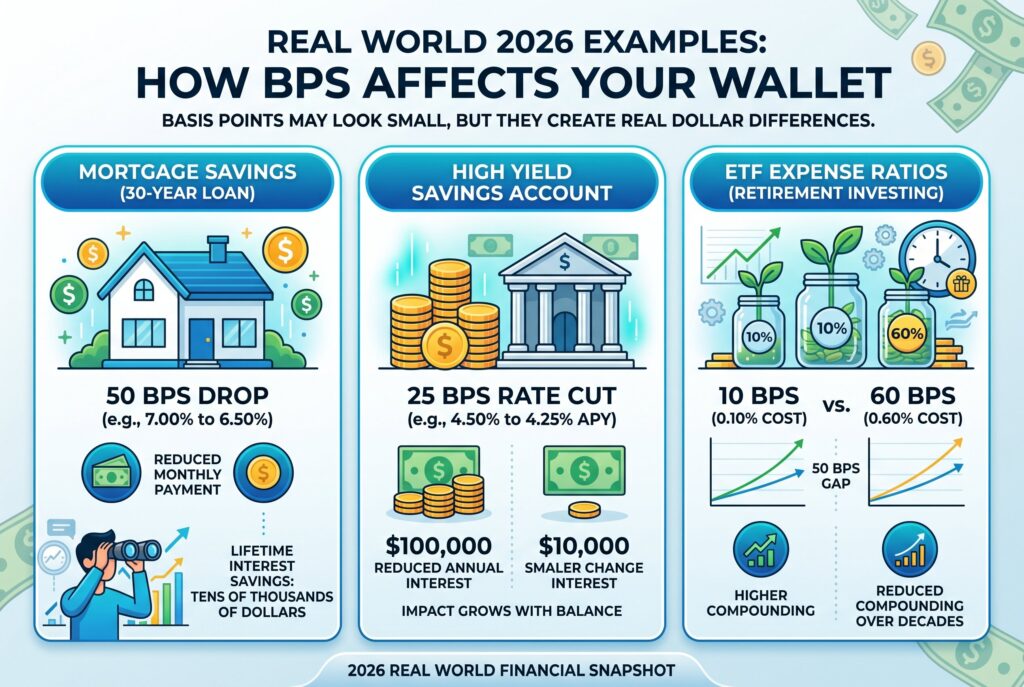

Real World Examples: How BPS Affects Your Wallet

Basis points may look small, but they can create real dollar differences. In a mortgage scenario, a 50 BPS drop in rates can make a major difference over a 30 year loan. If a borrower qualifies for 6.50% instead of 7.00%, the monthly payment may fall noticeably, and the lifetime interest savings can reach tens of thousands of dollars depending on the loan size. This is why homebuyers watch mortgage rate changes so closely.

In a high yield savings account scenario, a 25 BPS rate cut means an APY moving from 4.50% to 4.25%. That may not feel dramatic on a small balance, but on $50,000 or $100,000, it changes annual interest earnings. In an ETF expense ratio scenario, basis points matter even more over long periods. A fund charging 10 BPS costs 0.10% per year. A fund charging 60 BPS costs 0.60% per year. That 50 BPS gap may sound tiny, but over decades of retirement investing, it can reduce compounding significantly.

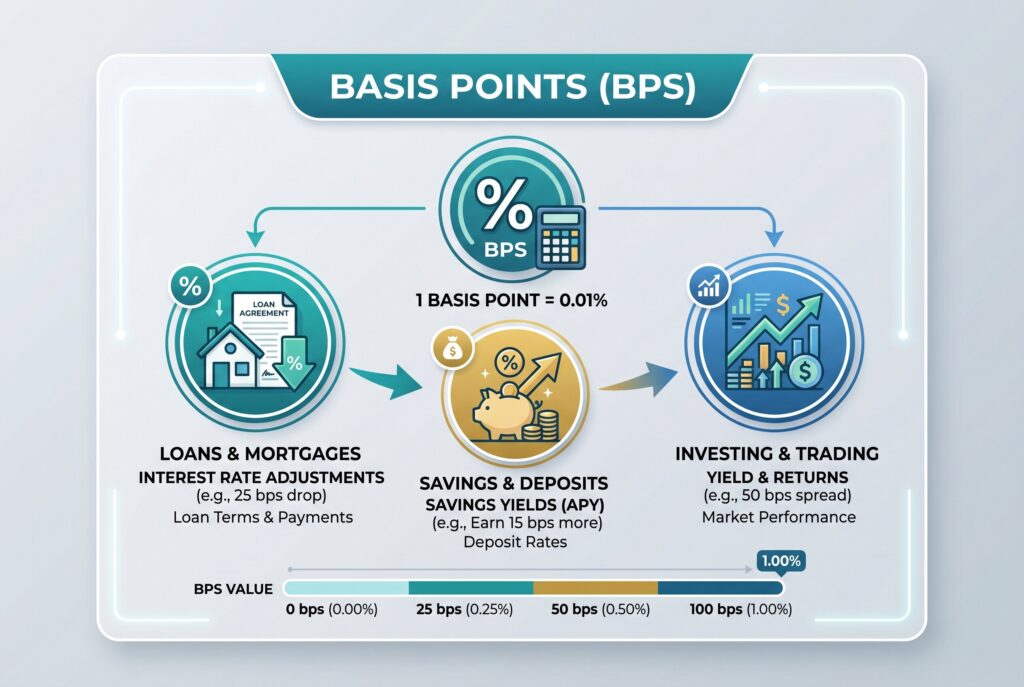

Basis Points in Loans, Savings, and Investing

Basis points show up anywhere small percentage changes matter. For loans, BPS affect APR, monthly payments, and total interest. A 100 BPS increase on a business loan or mortgage means the rate is one full percentage point higher.

For savings, BPS affect APY and interest earned. When banks lower savings rates by 25 BPS, depositors earn less on cash balances. For investing, basis points are often used in expense ratios, bond yields, and credit spreads. A 20 BPS fee difference between two funds may seem small, but lower fees leave more money invested. In bonds, basis points help describe changes in yields and spreads with precision.

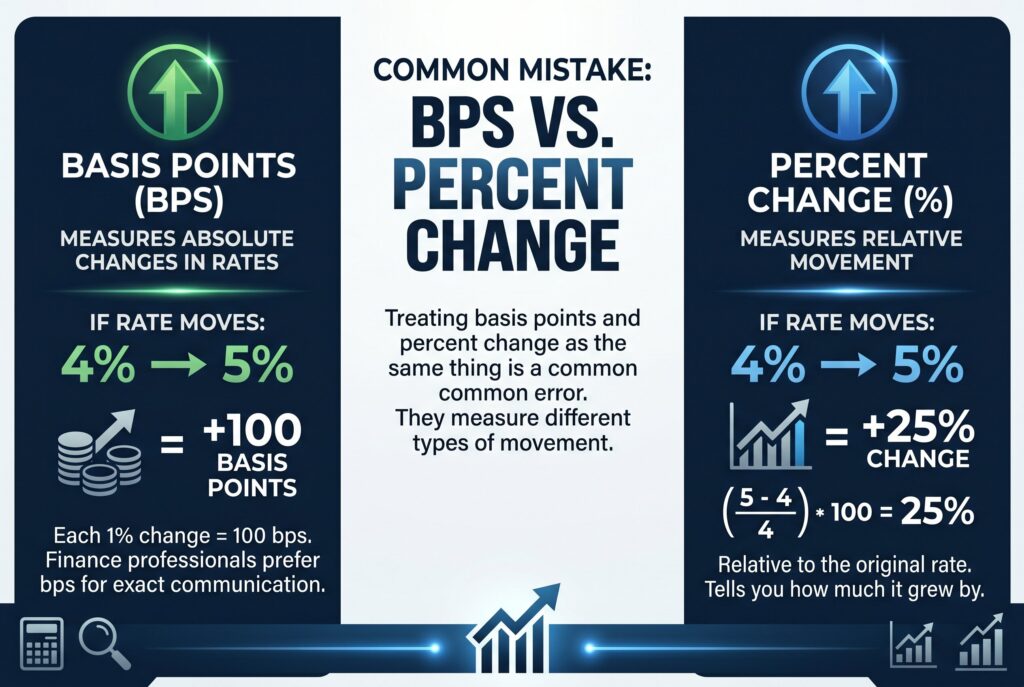

Common Mistake: Basis Points vs Percent Change

The biggest mistake is treating basis points and percent change as the same thing. They aren’t. Basis points measure absolute changes in percentage rates. Percent change measures relative movement. If a rate moves from 4% to 5%, it increases by 100 basis points. But relative to the original 4%, that is a 25% increase. Both statements can be mathematically true, but they mean different things. This is exactly why finance professionals prefer basis points when discussing rates. It keeps the message clean and exact.

Conclusion

Basis points may sound technical, but they are simply a precise way to describe fractions of a percent. One basis point equals 0.01%, and 100 basis points equals 1%.

Once you understand what are basis points, financial headlines about rate changes, mortgage moves, savings APY shifts, ETF fees, and bond yields become much easier to interpret. The next time you see a rate move by 25, 50, or 100 BPS, you’ll clearly understand what changed and how it impacts your money.