Many homeowners assume their insurance should match their mortgage balance or home value, but neither determines how much homeowners insurance you actually need. The right amount is the coverage required to rebuild your home, replace your belongings, cover temporary living expenses, and protect you from liability after a major loss. With construction costs and severe weather continuing to rise in 2026, under-insurance has become increasingly common. Knowing how much coverage you need before disaster strikes can help you avoid costly gaps when filing a claim.

Most Homeowners Need More Than They Think

There is no universal insurance amount that works for every homeowner. Two houses with identical market values can require very different levels of protection depending on their rebuilding costs, personal belongings, location, and liability exposure.

However, most homeowners need enough coverage to accomplish four things:

- Rebuild the home completely

- Replace personal belongings

- Pay for temporary living expenses during repairs

- Protect against major liability claims

If any of those areas are significantly underinsured, a serious loss could create substantial out-of-pocket expenses.

Can You Afford to Rebuild Your Home?

The first question isn’t how much your home is worth. The question is how much it would cost to rebuild it. Many homeowners focus on market value because it is easy to find. Real estate websites, tax assessments, and appraisals all provide estimates of what a property could sell for. Insurance companies, however, are concerned with replacement costs.

Replacement cost is the amount required to reconstruct the home using current labor and material prices. It includes demolition, debris removal, permits, contractor costs, and rebuilding expenses. It doesn’t include the value of the land. For example, a home that sells for $550,000 may only require $420,000 to rebuild. In another market, a house worth $400,000 could cost more than $500,000 to reconstruct because labor and materials are expensive. This is why the amount of insurance you need should begin with a realistic rebuilding estimate rather than a market valuation.

If Everything Inside Your Home Disappeared, Could You Replace It?

Most homeowners underestimate the value of their belongings. Furniture, electronics, clothing, appliances, cookware, tools, sporting equipment, and everyday household items add up surprisingly quickly. After a major fire or natural disaster, replacing everything at once can cost far more than people expect.

Imagine walking through your home and making a list of everything you own. Then imagine buying every item again at today’s prices. For many households, the total would reach well into six figures. This doesn’t mean every homeowner needs the same amount of personal property coverage. A retired couple in a smaller home may have very different needs than a family with children, home office equipment, high-end electronics, or expensive hobbies.

The amount of homeowners insurance you need should reflect the value of what you would actually need to replace, not an average number used by someone else.

Could You Handle Living Somewhere Else for Several Months?

Many people focus entirely on rebuilding costs and forget what happens during the rebuilding process. After a major fire, severe storm, or other covered disaster, repairs can take months. In some cases, reconstruction may take a year or longer. During that time, you may still need a place to live.

Temporary housing expenses can include rent, hotel stays, meals, storage costs, laundry services, and transportation expenses. These costs are often much higher than homeowners expect, particularly in cities with expensive rental markets. A policy that pays to rebuild your home but leaves you struggling to afford temporary housing may still leave you in a difficult financial position. When evaluating how much homeowners insurance you need, consider not only the cost of rebuilding but also the cost of maintaining your normal life while the rebuilding takes place.

What Would Happen If Someone Sued You?

Homeowners insurance is often associated with property damage, but liability protection can be equally important. If a guest is injured on your property or if you are found responsible for someone else’s injuries or property damage, legal costs can escalate quickly. Medical bills, attorney fees, settlements, and court judgments can easily exceed what many households could comfortably afford.

This risk varies from one homeowner to another. A person who regularly hosts gatherings, owns a swimming pool, has a dog, or has substantial financial assets may face greater liability exposure than someone with fewer risk factors. When determining how much homeowners insurance you need, it is worth considering not only what you own today but also what you are trying to protect in the future.

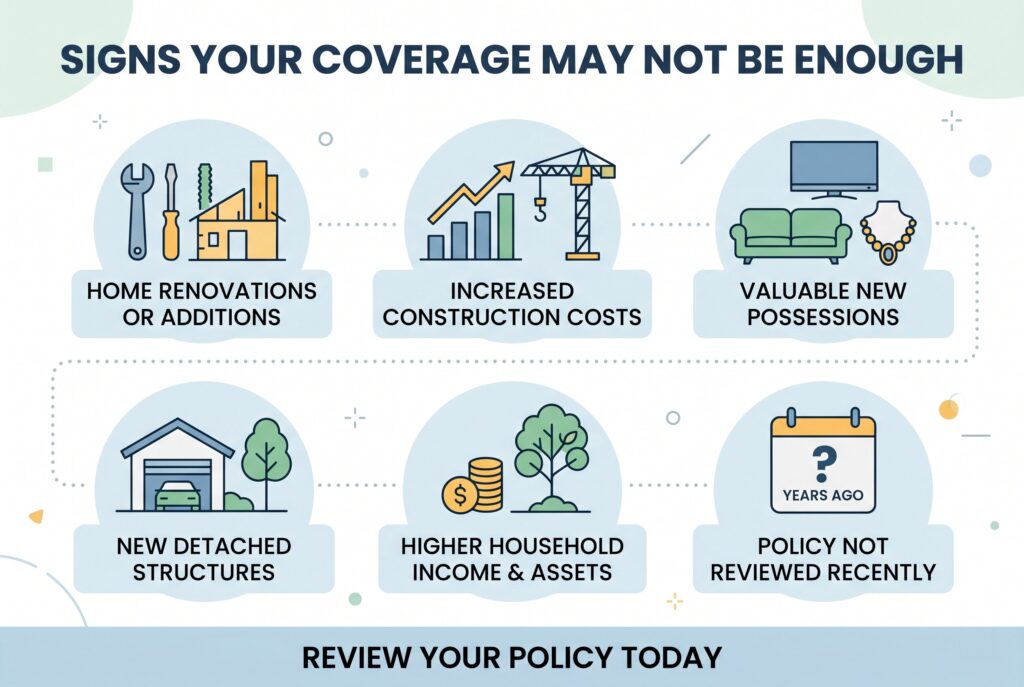

Signs Your Current Coverage May Not Be Enough

Many homeowners purchase a policy and rarely review it again. Over time, however, their insurance needs change.

You may need more coverage than you currently have if:

- Your home has been renovated or expanded

- Construction costs in your area have increased significantly

- You have purchased expensive furniture, electronics, jewelry, or collectibles

- You added a detached structure such as a workshop or garage

- Your household income and assets have grown

- Your policy hasn’t been reviewed in several years

A policy that was adequate five years ago may no longer provide the same level of protection today.

Signs You May Be Paying for More Insurance Than You Need

While under-insurance is a common problem, over-insurance can happen as well. One example is insuring your home based on market value rather than rebuilding cost. In areas where land values are high, a significant portion of the property’s value may come from the location itself rather than the structure. Since insurance is intended to rebuild the home rather than replace the land, using market value can sometimes lead to unnecessarily high coverage limits. The goal isn’t to buy the largest policy available. The goal is to buy coverage that accurately reflects your financial exposure.

The Best Way to Calculate Your Insurance Needs

Instead of asking, “How much is my house worth?” ask a series of more practical questions.

- How much would it cost to rebuild the structure?

- How much would it cost to replace everything inside?

- How long could rebuilding take in my area?

- How much liability protection would I need if a serious accident occurred?

The answers to those questions provide a far more accurate picture of your insurance needs than a mortgage balance or online home valuation ever could.

Conclusion

So, “how much homeowners insurance do I need,” the answer isn’t determined by a single number. It is determined by whether your policy can fully protect your home, belongings, lifestyle, and finances after a major loss.

For most homeowners, that means having enough coverage to rebuild the house, replace personal property, pay for temporary living expenses, and absorb the financial impact of a liability claim. Rather than focusing on your home’s market value, focus on the real-world costs you would face if everything had to be replaced tomorrow. When your coverage reflects those realities, you are far more likely to have the protection you actually need when it matters most.

Related Articles

How Much Is Homeowners Insurance? 2026 US Averages by State

How Much Is Homeowners Insurance on a $150,000 House? 2026 Breakdown

How Much Is Homeowners Insurance on a $400,000 House? 2026 Hidden Costs