Whether you found a cheaper rate, sold your vehicle, moved to a new state, or simply no longer drive, you may wonder: can I cancel my car insurance at any time? In most cases, yes. You’re usually allowed to cancel your policy before the end of a 6-month or 12-month term. But canceling the wrong way can create a coverage lapse, cancellation fees, DMV problems, lender penalties, or higher future premiums. The goal isn’t just to cancel car insurance. The goal is to cancel cleanly, protect your driving record, and recover any auto insurance refund you’re owed.

The Golden Rule: Never Cancel Before Buying New Coverage

A coverage lapse is the biggest mistake drivers make when canceling car insurance. Even a one-day gap between policies can create problems. Your state may flag your registration, future insurers may treat you as higher risk, and your next premium could increase.

If you’re switching companies, make your new policy start before the old policy ends. A safe approach is to schedule your old policy cancellation for the same day or the day after your replacement coverage begins. If you sold the car and won’t drive anymore, the risk is different. In that case, focus on DMV rules, plate return requirements, and written proof that the vehicle is no longer yours.

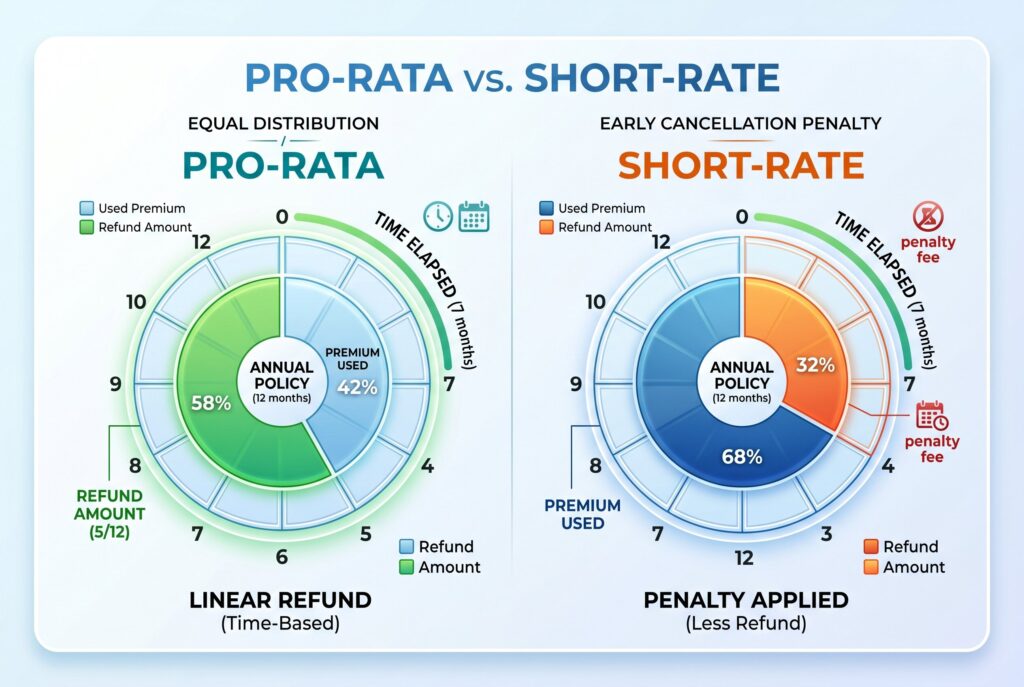

Understanding Your Refund: Pro-Rata vs. Short-Rate

Pro-Rata Cancellation

A pro-rata refund gives back the unused portion of your premium. If you paid $600 for a 6-month policy and canceled halfway through, you may receive about $300 back. This is the cleanest refund method because you only pay for the days you were insured. Many major insurers use some version of prorated refunds, but you should still confirm before canceling.

Short-Rate Cancellation

A short-rate cancellation means the insurer keeps part of the unused premium as a penalty. This may appear as a percentage of the remaining premium or a flat cancellation fee. For example, if you have $300 in unused premium and the insurer charges a 10% short-rate fee, your refund may be reduced by $30. Some insurers may also charge admin fees.

When You May Not Get Much Back

If you pay monthly, you may not receive a large refund because you haven’t prepaid much. But you still need to cancel officially. Simply stopping payment can lead to cancellation for nonpayment, which is worse than a normal cancellation.

How to Cancel Car Insurance in 5 Simple Steps

1. Secure Your Replacement Policy First

Before you cancel car insurance, shop for new coverage and confirm the exact start date. Don’t rely on a quote. A quote isn’t active insurance. Once the new policy is issued, compare the start date with your old policy’s cancellation date. Your goal is continuous coverage with no gap.

2. Contact Your Current Provider

Call your insurer, broker, or agent and say: “I’d like to cancel my policy effective [date]. I’ve already secured replacement coverage. Please confirm whether I’ll receive a prorated refund and send written cancellation confirmation.” This simple script prevents confusion. It also makes clear that you aren’t canceling by mistake or simply missing a payment.

3. Sign the Cancellation Request Form

Some insurers require a signed cancellation form, email confirmation, or electronic signature. Complete this step promptly. Don’t assume a phone call alone finishes the process. If the insurer needs your signature and you don’t provide it, the policy may remain active or billing may continue.

4. Notify the DMV and Return License Plates if Required

If you’re canceling because you sold the car, moved out of state, or no longer need coverage, check your state DMV rules. Some states require you to return license plates or cancel registration before insurance ends. This step is easy to miss, but it can matter. In certain states, canceling insurance while the vehicle is still registered can trigger fines, registration suspension, or proof-of-insurance notices.

5. Monitor Your Bank for the Refund

After cancellation, watch your bank account or credit card for the refund. Keep your cancellation confirmation, new insurance declarations page, sale documents, or plate return receipt. If the refund doesn’t arrive within the expected timeframe, contact the insurer and ask for the refund breakdown in writing.

Special Scenarios: Financed Cars and Month-to-Month Policies

Financed or Leased Vehicles

If your car is financed or leased, your lender usually requires full coverage, including comprehensive and collision. If you cancel without replacement coverage, the lender may buy force-placed insurance. Force-placed insurance is usually expensive and protects the lender, not you. Before canceling, make sure your new policy satisfies your loan or lease agreement.

Month-to-Month Car Insurance

Many drivers search for month to month car insurance, but most auto policies are still written for 6 or 12 months. Paying monthly doesn’t always mean you have a true monthly policy. If you pay monthly and want to stop, you still need to formally cancel. Otherwise, the insurer may continue auto-drafting or cancel you for nonpayment.

Selling Your Car

If you sell your vehicle, wait until the sale is complete before canceling. Keep the bill of sale and any DMV transfer documents. If you plan to buy another car soon, ask your insurer whether it makes sense to keep a non-owner policy or maintain continuous coverage to avoid future rate issues.

Moving to Another State

Insurance laws vary by state, so don’t assume your old policy works after a move. Contact your insurer before relocating and arrange a new policy that meets the new state’s requirements.

Frequently Asked Questions

Does Canceling Car Insurance Hurt My Credit Score?

Canceling normally doesn’t hurt your credit score. However, unpaid balances sent to collections could damage your credit. Always pay any final bill or resolve disputed charges quickly.

Can I Just Stop Paying My Bill?

No. Stopping payment can lead to cancellation for nonpayment, which may make future insurance more expensive. It can also leave you with fees or an unpaid balance.

Will I Always Get an Auto Insurance Refund?

Not always. Refunds depend on how much premium you prepaid, your cancellation date, and whether your insurer charges cancellation fees. Ask for the refund amount before finalizing cancellation.

Should I Cancel If I’m Not Driving Temporarily?

Maybe not. If you still own the car, consider reducing coverage, suspending optional coverage, or switching to storage coverage if available. Canceling completely can create registration and lapse problems.

Final Thoughts

You can usually cancel car insurance at any time, but timing matters. Before asking, “can I cancel my car insurance at any time,” make sure you buy replacement coverage first and avoid a lapse. Also remember that it doesn’t always mean you should cancel immediately without checking refund rules, DMV requirements, and getting written proof. Canceling correctly can save money. Canceling carelessly can cost more than keeping the policy for a few extra days. Treat the process like a clean handoff, not a quick goodbye.