You need to borrow a friend’s car for a weekend, drive a newly purchased vehicle home, or cover a relative who is visiting for a few days. Naturally, you search for temporary driver insurance and expect to find a simple 1 day car insurance policy. The problem is that short-term car insurance works very differently depending on where you live. In the U.K., daily or weekly cover can be a real product. In the U.S., true temporary car insurance is much harder to find, and many drivers need a legal workaround instead.

The Truth About 1 Day and Daily Car Insurance

Daily car insurance sounds convenient, but U.S. drivers need to be careful. Major U.S. insurers usually don’t sell true standalone 1 day car insurance or one week car insurance the way many people imagine. Most standard auto policies are written for six or 12 months, even if you pay monthly. That doesn’t mean you should drive uninsured. It means you need to choose the right legal alternative for your situation. If a website promises instant cheap temporary car insurance with almost no questions asked, slow down. Some offers may be misleading, limited, or not valid in your state.

In the U.K., the situation is different. Short-term car insurance can often be purchased for a few hours, one day, a week, or up to several weeks. That is why search results can be confusing: the answer depends heavily on the country and insurance market.

5 Best Workarounds for Short-Term Car Insurance

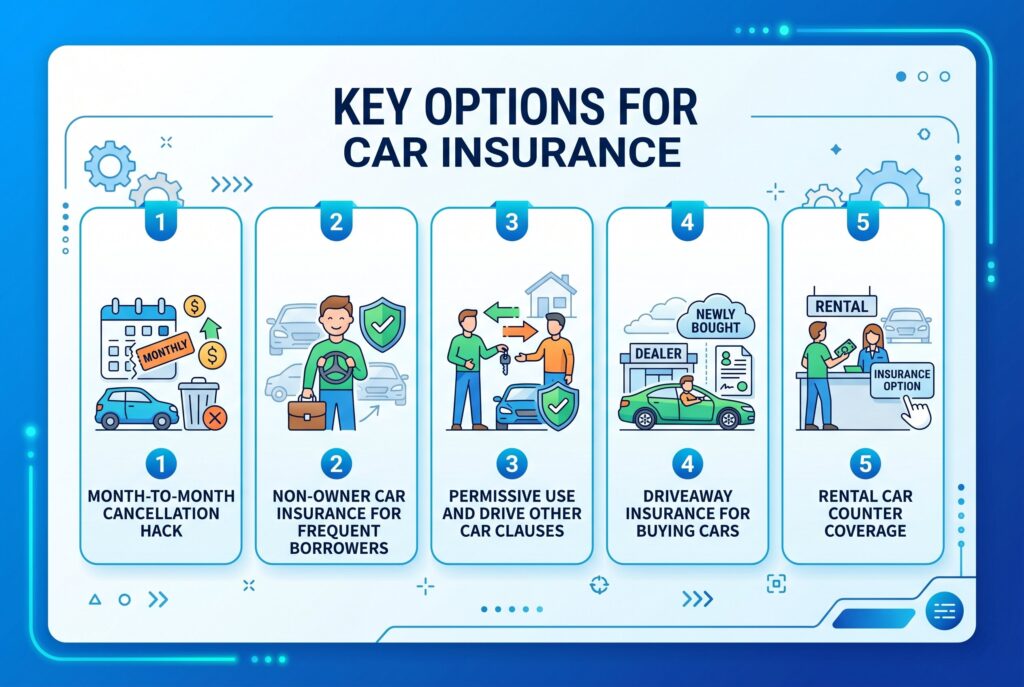

1. The Month-to-Month Cancellation Hack

If you own or just bought a car in the U.S., the most realistic option may be to buy a regular auto policy, pay monthly, and cancel when you no longer need coverage. This isn’t technically month to month car insurance, but it can function that way if the insurer allows early cancellation. Before buying, ask about cancellation fees, refund rules, and whether unused premium is prorated. This workaround is best when you need legal coverage for a few weeks or months, not just a few hours.

2. Non-Owner Car Insurance for Frequent Borrowers

Non owner car insurance is useful if you don’t own a car but borrow or rent vehicles regularly. It typically provides liability coverage when you drive a car you don’t own. This can be a smart option for people who frequently borrow cars, use car-sharing services, or want continuous insurance history. However, it usually doesn’t cover damage to the borrowed car itself, so read the policy carefully.

3. Permissive Use and Drive Other Car Clauses

If you borrow someone’s car with permission, their insurance may cover you under permissive use. This is often the simplest answer for a one-time borrowed vehicle situation. But there’s a catch. If you cause an accident, the claim may affect the owner’s policy and future premiums. Also, not every policy treats permissive drivers the same, so the owner should call their insurer before handing over the keys.

4. Driveaway Insurance for Buying Cars

Driveaway insurance can help when you buy a car and need to drive it home legally. Some dealerships or sellers may help arrange temporary coverage, but rules vary. Don’t assume dealer paperwork automatically protects you. Before leaving the lot, confirm that you have active liability coverage that satisfies your state’s requirements.

5. Rental Car Counter Coverage

If you’re renting a car, the fastest short-term solution is often rental car coverage. You may be able to buy liability coverage, collision damage waiver, or supplemental protection at the rental counter. Some credit cards also offer rental car benefits, but many exclude liability coverage. Always check the card terms before relying on it.

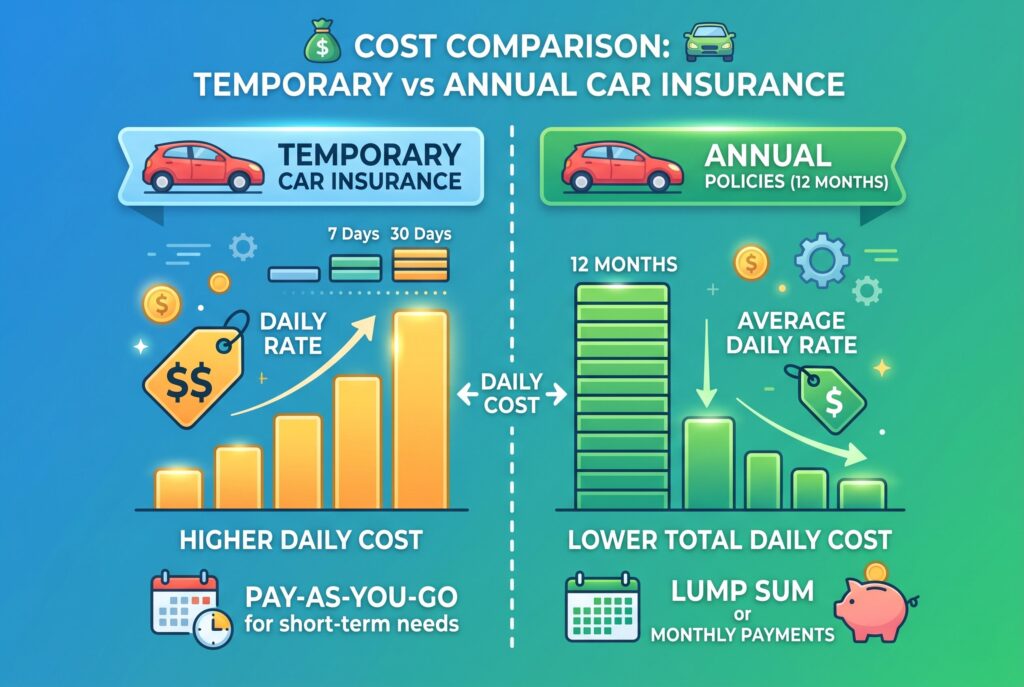

Temporary Car Insurance Costs vs Annual Policies

Temporary coverage often sounds cheaper because you only need it briefly. But on a daily basis, it can be more expensive than standard insurance. MoneyLion’s analysis notes that state-minimum short-term coverage may cost around $80 per month compared with around $30 per month for a standard policy, though real prices vary by driver, state, vehicle, and coverage level. This is why buying and canceling a standard policy can sometimes be more practical than chasing a “daily” policy. The cheapest option isn’t always the safest or most legitimate option.

Special Scenarios: Learner Drivers and SORN

Learner drivers often need temporary coverage when practicing in a parent’s or relative’s car. In many cases, adding the learner to an existing policy is simpler than trying to buy standalone daily cover. Parents should ask the insurer how learner drivers are handled before practice begins.

SORN is mostly a U.K. concept, referring to a vehicle declared off the road. If you want to drive that vehicle again, even briefly, you may need proper temporary insurance and must make sure the car is legally allowed back on the road.

Conclusion

Temporary driver insurance can be confusing because the product people search for doesn’t always exist in the form they expect. In the U.S., true daily or one week car insurance is rare, so legal workarounds matter more.

If you need coverage today, start with your situation. Borrowing once? Check permissive use. Borrowing often? Consider non owner car insurance. Buying a car? Arrange standard coverage or driveaway insurance before driving. Renting? Compare rental counter and credit card coverage. The goal isn’t just to find cheap temporary car insurance. The goal is to avoid driving uninsured, avoid scams, and choose coverage that actually protects you when something goes wrong.