")

You have the title to a car, but you don’t have a valid driver’s license. Maybe your license was suspended, you bought a car for a teen driver, a medical condition keeps you from driving, or you own a classic car that stays parked most of the year. The situation sounds impossible, but it isn’t.

Yes, you can get car insurance without a license in some cases. The challenge is that insurers usually want to know who will actually drive the car. If that person isn’t you, the policy has to be structured carefully so the vehicle is protected without pretending an unlicensed owner is the primary driver.

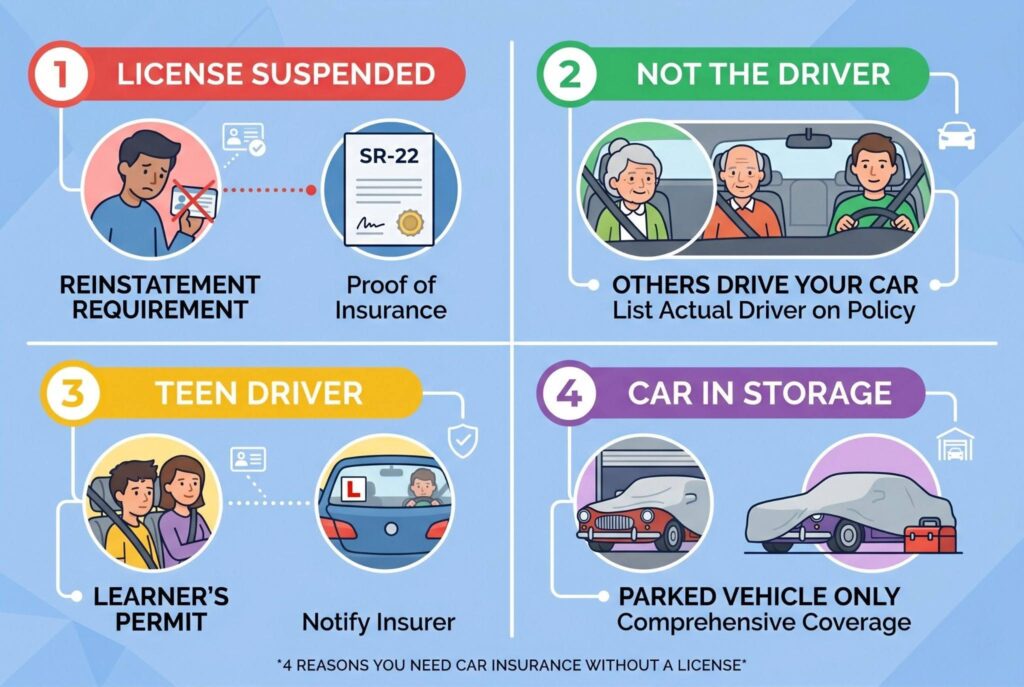

4 Reasons You Still Need Car Insurance Without a License

Suspension and SR-22 Requirements

If your license was suspended after a serious violation, your state may require proof of financial responsibility before reinstatement. That proof often comes through SR-22 insurance or, in some states, FR-44 filing. This doesn’t mean you can drive before your license is valid again. It simply means you may need an active insurance policy to start the reinstatement process.

Health or Age Limitations

Some people own a vehicle but no longer drive because of age, disability, or health concerns. A caretaker, spouse, adult child, or family member may drive them around in that car. In this case, the licensed driver should usually be listed as the primary driver. The insurer needs to rate the policy based on the person actually behind the wheel.

Teen Driver or Learner’s Permit

Parents may buy or own a vehicle for a teen who only has a learner’s permit. In many cases, the parent owns the car, but the teen or another licensed adult is the driver. Learner’s permit insurance rules vary, so it’s important to tell the insurer exactly who will drive and how often. Hiding a young driver can create claim problems later.

Classic Car or Storage Situation

If the car isn’t being driven, you may not need full liability coverage. Parked car insurance, sometimes called storage coverage or comprehensive-only coverage, can protect against theft, fire, vandalism, falling objects, and weather damage. This is useful for collectors, project cars, inherited vehicles, and cars waiting for repair.

How to Buy Car Insurance Without a License

1. List Someone Else as the Primary Driver

The cleanest option is often listing a licensed person as the primary driver. This may be a spouse, parent, adult child, roommate, caretaker, or trusted family member. The primary driver should be the person who actually drives the vehicle most. The insurer will usually use that person’s license and driving record to calculate risk.

2. Sign an Excluded Driver Form

An excluded driver form says you are not covered to drive the vehicle. This can make insurers more willing to insure the car because they are not taking on the risk of an unlicensed owner driving. This is serious. If you drive while excluded and crash, the insurer may deny the claim. You could be personally responsible for injuries, property damage, legal penalties, and vehicle repairs.

3. Purchase Parked Car Insurance

If no one will drive the car, ask about parked car insurance. This may remove liability and collision while keeping comprehensive protection. It is usually cheaper than full coverage because the car isn’t being driven on public roads. However, if anyone plans to drive it, even briefly, you need active road coverage before moving it.

4. Add a Co-Owner to the Title

If insurers reject the application because the titled owner has no license, adding a licensed co-owner may help. This gives the insurer a licensed person connected to the vehicle. This is a legal and financial decision, not just an insurance trick. A co-owner may have rights to the vehicle, so only use this route with someone you fully trust.

Registration Hurdles by State

Having insurance doesn’t always mean you can register the car. Some states require the registered owner to show a valid license, while others allow an unlicensed owner to register a vehicle if a licensed driver and valid insurance are listed. Before buying a policy, check your DMV rules for unlicensed vehicle registration. This matters most if you are buying a car, transferring title, renewing plates, or trying to register a vehicle after a license suspension.

What to Say When You Call an Insurer

Online quote tools often reject applications without a license number. Calling a human agent usually works better.

Use this script:

“Hi, I am the titled owner of the vehicle, but I am not the primary driver. I need a policy listing [Name] as the licensed primary driver. I may also need to be listed as an excluded driver. Can you quote this situation?”

If your license is suspended, add:

“I also need to know whether you can file an SR-22 or FR-44 for reinstatement.”

Final Thoughts

Car insurance without a license is possible, but insurers usually require a licensed primary driver on the policy and may exclude the unlicensed owner from coverage. The safest approach is simple: don’t drive without a valid license, be honest with the insurer, gather the primary driver’s license information, and call an agent instead of relying only on online quote forms. Your goal is protecting the vehicle without creating claim problems later.