A blanket mortgage allows multiple properties to be financed under a single loan instead of separate mortgages. The approach is popular with real estate investors because it can simplify financing and make portfolio growth more efficient. However, the same loan is secured by multiple properties, which means the risks can be higher if the investment doesn’t perform as planned.

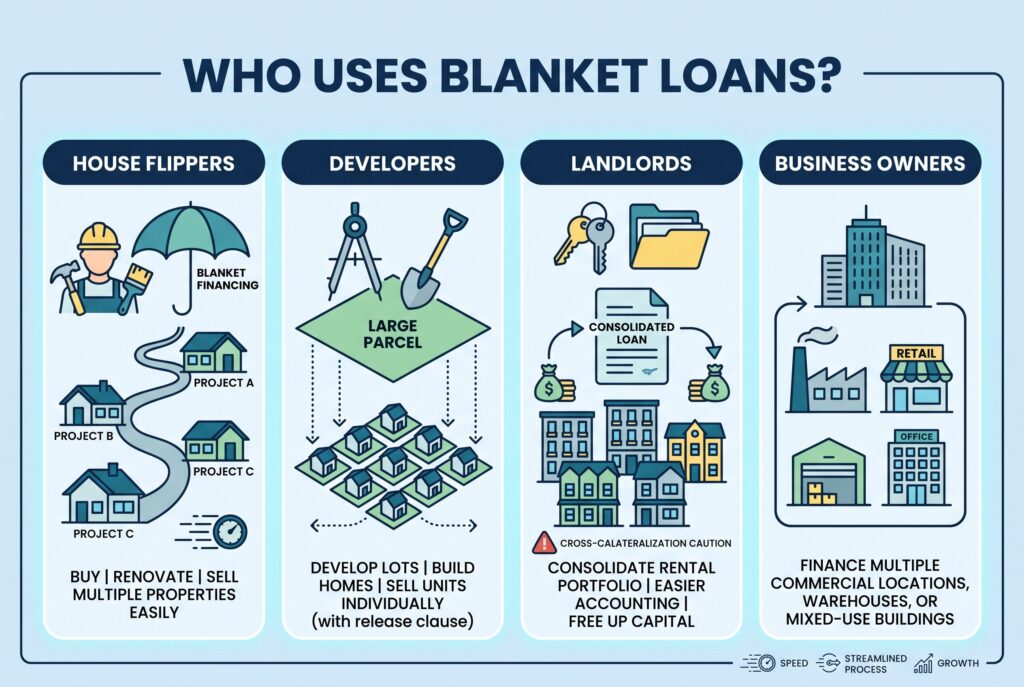

Who Actually Uses a Blanket Loan?

Blanket mortgages are designed for investors managing multiple properties rather than buyers purchasing a single primary residence. They work best when borrowers need flexible financing across an entire portfolio.

House flippers use blanket mortgage financing when they want to buy several distressed homes, renovate them, and sell each one separately. Instead of applying for a new loan every time they purchase a property, they can finance multiple projects under one umbrella. This can save time, reduce paperwork, and help them move quickly in competitive markets.

Developers use blanket mortgages when they buy a large parcel, divide it into lots, build homes, and sell units one by one. The loan covers the broader project, while the release clause allows specific lots or homes to be released from the mortgage after sale.

Landlords may use blanket mortgage loans to consolidate several rental properties into one loan. This can make accounting easier and may free up capital for more acquisitions. However, landlords must be especially careful because one weak rental can affect the whole structure if the loan is cross collateralized.

Business owners may also use blanket financing when they own several commercial locations, warehouses, or mixed use buildings.

The Release Clause: The Detail That Makes or Breaks the Deal

The release clause is the most important feature in a blanket mortgage. It allows one property to be removed from the loan after certain conditions are met, usually after part of the debt is paid down. Imagine a developer finances ten townhomes with one blanket loan. As each townhome sells, the lender releases that unit from the mortgage so the buyer can receive clear title. Without a release clause, the developer might have to pay off the entire loan before selling one property, which defeats the purpose.

For flippers, the release clause controls exit strategy. If you sell one renovated home, you need to know exactly how much of the sale proceeds must go back to the lender. If the release price is too high, your profit may disappear. Before signing, ask how each release is calculated, whether there are minimum paydown amounts, whether release approvals are automatic, and whether the lender can block a sale. A blanket loan only works when the exit path is clear.

Pros and Cons of a Blanket Mortgage

Lower Closing Costs

Financing several properties under one mortgage can reduce many of the costs that come with separate loans. Depending on the lender, expenses such as loan origination fees, title work, legal documentation, and some administrative costs may only be paid once instead of for every property. For investors purchasing multiple properties at the same time, those savings can free up capital for renovations, reserves, or future acquisitions.

Easier Portfolio Management

Managing multiple mortgages often means tracking different lenders, payment dates, and loan terms. A blanket mortgage simplifies that process by combining several properties into one loan with a single monthly payment. For investors with growing portfolios, fewer loans can make budgeting, recordkeeping, and refinancing discussions much easier.

More Borrowing Power

A blanket mortgage may allow investors to use equity from existing properties to finance additional purchases. Instead of qualifying each property separately, the lender evaluates the overall portfolio, which can make expansion more efficient for experienced investors.

Cross Collateralization Increases Risk

The biggest drawback of a blanket mortgage is cross collateralization. Because multiple properties secure the same loan, financial trouble with one investment can affect the entire portfolio. A prolonged vacancy, unexpected renovation costs, or falling property values may create pressure that extends well beyond a single property. Before using a blanket loan, make sure your portfolio can comfortably support the debt under less favorable market conditions.

Balloon Payments

Many blanket mortgages are commercial loans with relatively short-terms. Monthly payments may be based on a longer amortization schedule, but the remaining balance often becomes due after three to ten years. If interest rates rise or lending standards tighten before the balloon payment comes due, refinancing may become more expensive or more difficult than expected.

Stricter Qualification Standards

Blanket mortgages usually have stricter underwriting than traditional residential loans. Lenders may require larger down payments, strong cash reserves, detailed property schedules, rent rolls, operating statements, and previous investment experience. Borrowers with stable cash flow and a well-managed portfolio generally have the best chance of approval.

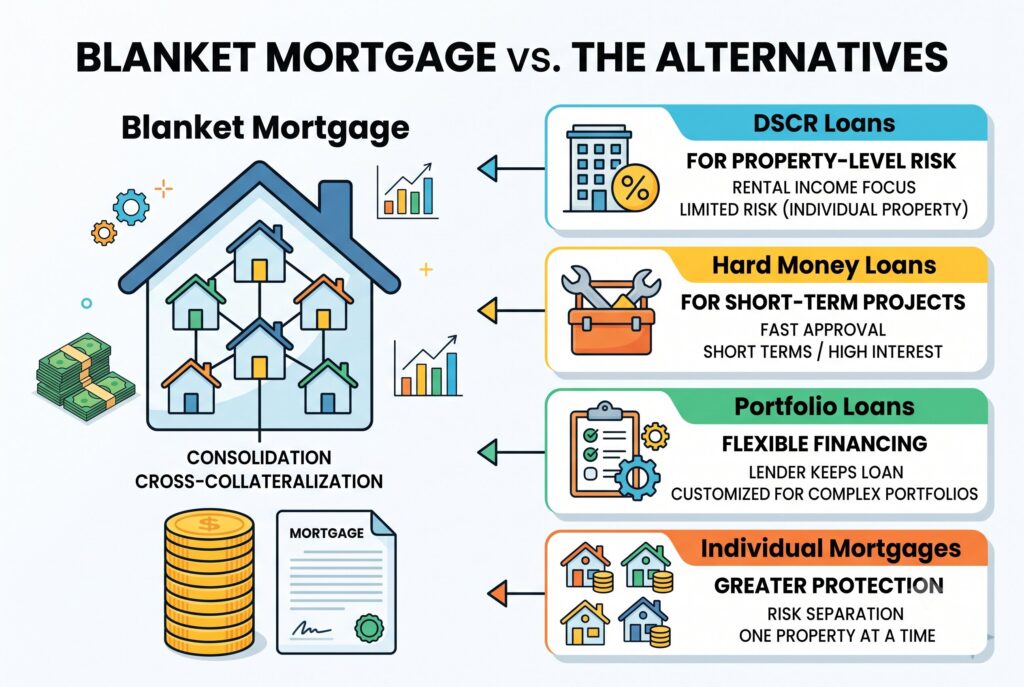

Blanket Mortgage vs. The Alternatives

A blanket mortgage isn’t always the best investor loan. Compare it against DSCR loans, hard money loans, portfolio loans, and individual mortgages before committing.

DSCR Loans: A Better Option for Property-Level Risk Management

DSCR loans are popular with rental property investors because each property is financed separately. Instead of focusing on your personal income, lenders primarily evaluate whether the property’s rental income can cover its debt payments. This structure also limits risk. If one property underperforms, it generally won’t affect financing for the rest of your portfolio.

Hard Money Loans: Ideal for Short-Term Renovation and Flip Projects

Hard money loans are designed for short-term investments such as renovations and house flips. They typically offer faster approvals than conventional financing but come with higher interest rates and shorter repayment terms. For investors planning to buy, renovate, and sell within a few months, the speed of funding may outweigh the higher borrowing costs.

Portfolio Loans: Flexible Financing for Complex Investment Situations

Portfolio loans remain on the lender’s balance sheet instead of being sold on the secondary market. Because of this, lenders often have greater flexibility when evaluating borrowers with multiple properties, nontraditional income, or unique investment situations. Although they don’t combine several properties into one loan like a blanket mortgage, portfolio loans can provide customized financing without exposing an entire portfolio to the same level of cross collateralization.

Individual Mortgages: Greater Protection Through Risk Separation

Traditional mortgages finance one property at a time. While they require more paperwork and multiple closings, they also keep each investment financially separate. For many long-term investors, this added protection outweighs the convenience of consolidating several properties under one loan.

Conclusion

A blanket mortgage can be a powerful tool for real estate investors, developers, house flippers, and landlords who need to finance multiple properties. It can reduce closing costs, simplify payments, and unlock leverage across a portfolio.

But the same structure that creates power also creates danger. Cross collateralization can put several properties at risk. Balloon payments can create refinance pressure. A weak release clause can trap your equity. Before signing, review the loan with a real estate attorney, compare DSCR loans and portfolio loans, and model your exit strategy property by property.

A great blanket loan helps you do more than expand your portfolio, it gives you the freedom to sell, refinance, and stay resilient when market conditions are less than ideal.