If you’re nervous about applying for a Chase card, that’s completely normal. A lot of people want a safer path that starts with Chase credit card pre approval instead of jumping straight into a full application and risking a hard inquiry. That’s exactly why Chase pre approval matters. It gives you a way to check whether Chase has offers for you before you formally apply. Chase’s official pre-approved offers page says you can check with no impact to your credit score, which means this first step is a soft pull, not a hard pull.

For beginners, that changes the whole process. Instead of guessing, you can start with a softer screening step, then decide whether cards like Chase Freedom Rise make sense for your profile. It also helps to understand one more piece before you apply for real: what credit bureau Chase uses when it moves from soft-pull screening to final approval. Chase says issuers can use one or more of the major bureaus, and bureau selection can vary by geography and other factors.

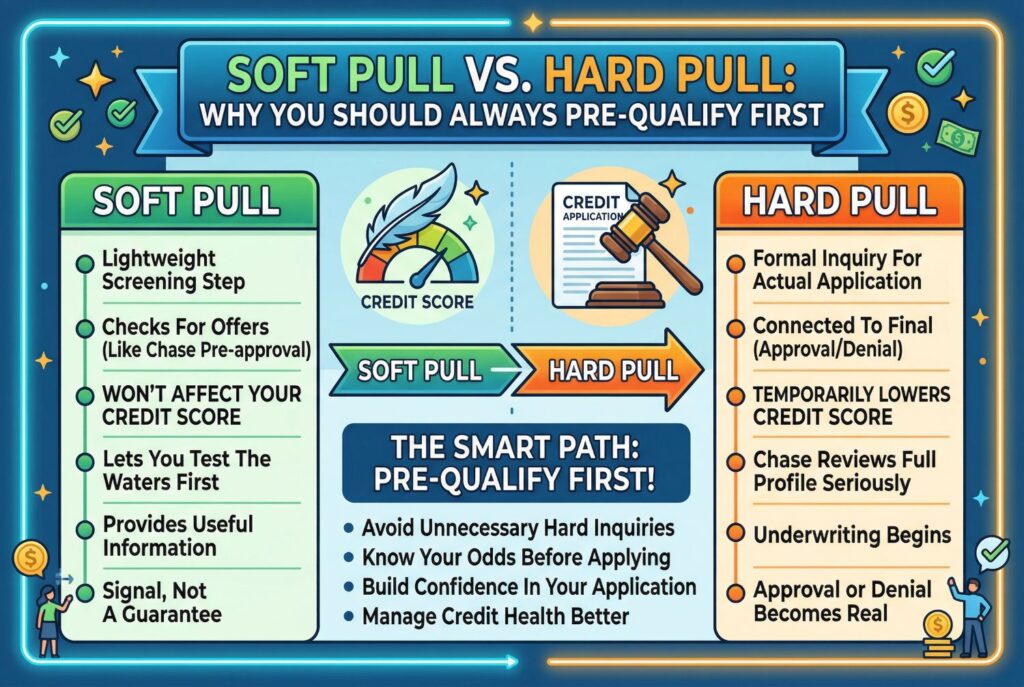

Soft Pull vs. Hard Pull: Why You Should Always Pre-Qualify First

The easiest mistake new applicants make is treating every credit check like it works the same way. It doesn’t. A soft pull is the lighter screening step. A hard pull is the formal inquiry tied to an actual application.

In practical terms, credit card pre approval Chase checks are valuable because they let you test the waters first. Chase’s official pre-approved offers page explicitly says checking for offers won’t affect your credit score. That’s the main reason to start there. You get useful information without the pressure of a hard inquiry right away.

The hard pull usually happens only after you submit the actual application. That’s when Chase reviews your full profile more seriously, and that’s when approval or denial becomes real. Pre-approval helps, but it doesn’t override underwriting. It’s a signal, not a guarantee.

The Truth About the “Chase Secured Credit Card” in 2026

A lot of people search for a Chase secured credit card because they assume a secured product must be the easiest place to start. The important thing to know is simple: Chase doesn’t offer a traditional secured credit card. Chase says this directly across multiple education pages about secured cards and starter cards.

That might sound frustrating at first, but it actually makes the next step clearer. Instead of looking for a Chase secured card that doesn’t exist, beginners should focus on Chase’s actual starter option. For most people in this situation, that means looking at Freedom Rise.

Chase Freedom Rise: The Ultimate Starter Card

Chase Freedom Rise is built for people who are new to credit. Chase says the card lets you establish credit, earn 1.5% cash back on all purchases, and pay no annual fee. It also comes with Chase Credit Journey access, which gives cardholders a way to track their credit score and monitor progress as they build history.

That combination matters because beginner cards often force people into tradeoffs. Some are easier to get but come with weak rewards. Others have fees that make the card harder to justify. Freedom Rise stands out because it stays simple. No annual fee, straightforward rewards, and a structure designed for people who are just getting started.

Another detail that helps is that Chase says no prior credit history is required to qualify for Freedom Rise. That makes it a much more realistic entry point than premium cards that expect stronger scores and longer histories.

The $250 “Secret”: How to Improve Your Freedom Rise Approval Odds

This is one of the most useful practical details Chase gives directly. Chase says that having at least $250 in your Chase checking account within three days of submitting your Freedom Rise application may improve your chances of approval. Chase also says that having qualifying funds is neither a requirement nor a guarantee of approval, so it’s best to think of this as an approval booster, not a magic loophole.

Psychologically, this matters a lot for beginners. It gives you something concrete to do before applying. If you’re worried that your file is too thin, opening a Chase checking account and funding it can make the process feel less random. It’s not a promise, but it is one of the clearest steps Chase publicly links to improved approval odds for this specific card.

Step by Step: How to Use the Chase Pre Approval Tool

Start with Chase’s official pre-approved offers page. Enter the requested information exactly as prompted and see whether any cards appear. If you already bank with Chase, it’s also smart to sign in and check for personalized “Just for You” style offers inside your account. Chase also continues to use targeted mailers and branch-based offers for some customers.

If you see an offer, read it carefully. Pre-approved and pre-qualified language can both be helpful, but neither should make you ignore Chase’s broader approval rules. One of the biggest is the 5/24 rule, which is the widely reported guideline that many Chase cards become difficult or impossible to get if you’ve opened five or more cards across issuers in the last 24 months. A pre-approval signal doesn’t reliably erase that risk.

What Credit Bureau Does Chase Use for Final Approval?

What credit bureau does Chase use? The most accurate answer is that Chase can use more than one, but Experian is often reported as the most common. Chase’s own education content says issuers may use one or more bureaus and that bureau choice can vary by location, contracts, and cost. That means Equifax or TransUnion can show up too, depending on your state and profile.

For applicants, the practical takeaway is simple. Don’t assume only one report matters. Before you formally apply, make sure all three of your reports are in decent shape, especially if you’re right on the edge of approval. Thin files and certain business applications can sometimes create multiple pulls, so it’s smarter to prepare broadly rather than guess narrowly.

Applied but Denied? How to Use the Chase Reconsideration Line

If you apply and don’t get instant approval, don’t panic. The first thing to do is check your Chase credit card application status. Chase says you can call 1-888-338-2586 for status updates, including business card applications. In practice, applicants also use this same path as the Chase reconsideration line when they want a manual review or want to provide more context after a pending or denied result.

This step matters because denial isn’t always final in the way people assume. Sometimes Chase just needs more information. Sometimes the application needs a human review. If your profile is otherwise reasonable and your story makes sense, a reconsideration call can be worth making.

Conclusion

The safest path is straightforward. Start with Chase pre approval so you can screen for offers by soft pull first. If you’re a beginner, focus on Chase Freedom Rise rather than wasting time searching for a Chase secured credit card that Chase doesn’t offer. If possible, consider the $250 checking relationship step to strengthen your Freedom Rise odds. Then, before you submit a real application, make sure your credit reports are ready and remember that Chase may check Experian, Equifax, or TransUnion depending on your situation. That’s the smartest way to turn Chase pre approval credit card research into an actual approval plan.