If you’re researching Chase credit card pre approval, you’re usually trying to answer two questions before you apply. First, can you check your odds without hurting your score? Second, what credit bureau does Chase use when you move from a soft-pull offer check to a real application? Chase now has an official “See if you have pre-approved offers” page that says you can check for offers with no impact to your credit score, which makes the first part much easier than it used to be.

That still doesn’t mean approval is guaranteed. Pre-approval and pre-qualification are useful signals, but Chase can still review your full application, apply its underwriting rules, and pull one or more credit reports when you submit for a card. Chase’s own education content says issuers may use one or more of the three major bureaus, while application data points reported by applicants continue to show Chase leaning heavily toward Experian, with Equifax or TransUnion showing up in some states and occasional multi-bureau pulls in certain situations.

Does Chase Have a Pre-Approval Tool in 2026? Soft Pull Explained

Yes, Chase does have a live self-serve pre-approval flow in 2026. Its public pre-approved offers page says you can check to see if you have offers available without affecting your credit score, which means the inquiry for that check is handled as a soft pull rather than a hard pull. Chase also surfaces the same “check for pre-approved offers with no impact to your credit score” language across several current card pages and card comparison pages.

That matters because a soft-pull chase pre approval check lets you test the waters before you generate a hard inquiry. It’s a useful screening step, especially if you’re trying to protect your profile, stay selective with applications, or gauge whether you’re even in the right tier for a Chase card. But treat it as a signal, not a contract. Once you submit a formal application, Chase can still hard pull your report and make a different final decision.

3 Ways to Check Your Chase Credit Card Pre Approval

1. The Official Online Pre-approval Tool

This is the easiest route for most people. Go to Chase’s public pre-approved offers page, enter the requested identifying details, and see whether you have eligible offers. Chase says this check doesn’t affect your credit score. That makes it the cleanest version of credit card pre approval chase shoppers usually want.

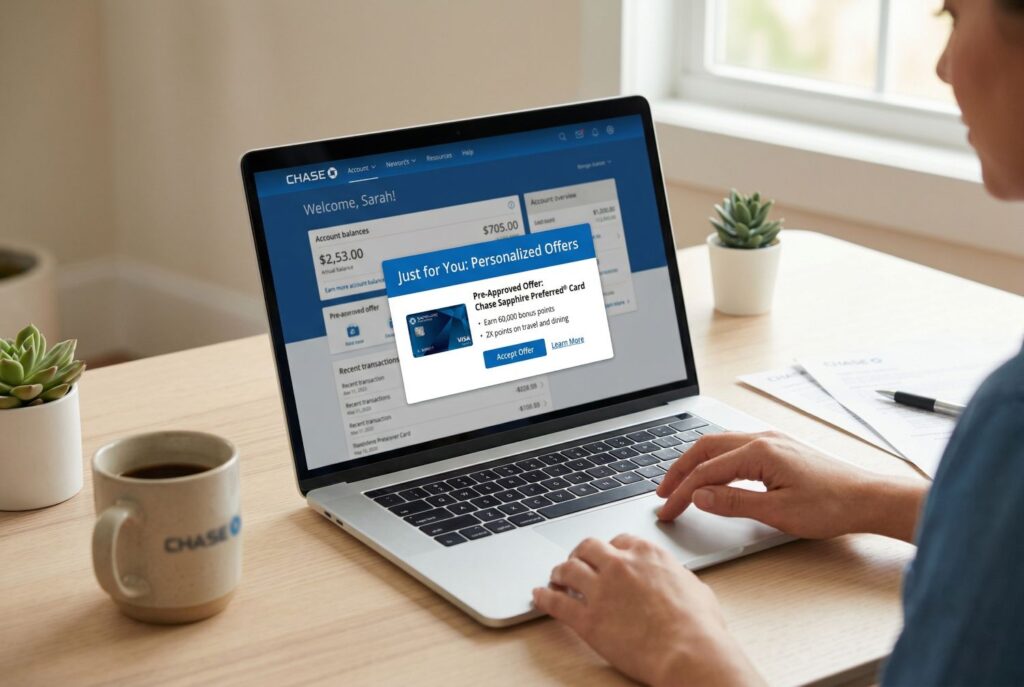

2. Logged-in “Just for You” Offers

If you already bank with Chase, sign in and look for personalized offers inside your account. These can appear in card marketing sections or “Just for You” style areas. Chase also promotes pre-approved offer checks directly on current card pages and logged-in paths, so existing customers may see more tailored offers than the public site shows.

3. Targeted Mailers and In-branch Offers

Some people still receive physical mail offers or can ask about eligibility in a branch. These offers can be useful, but they still aren’t the same as final approval. In practical terms, think of pre-qualified as a softer marketing signal and pre-approved as a stronger signal, but neither overrides full underwriting once you actually apply.

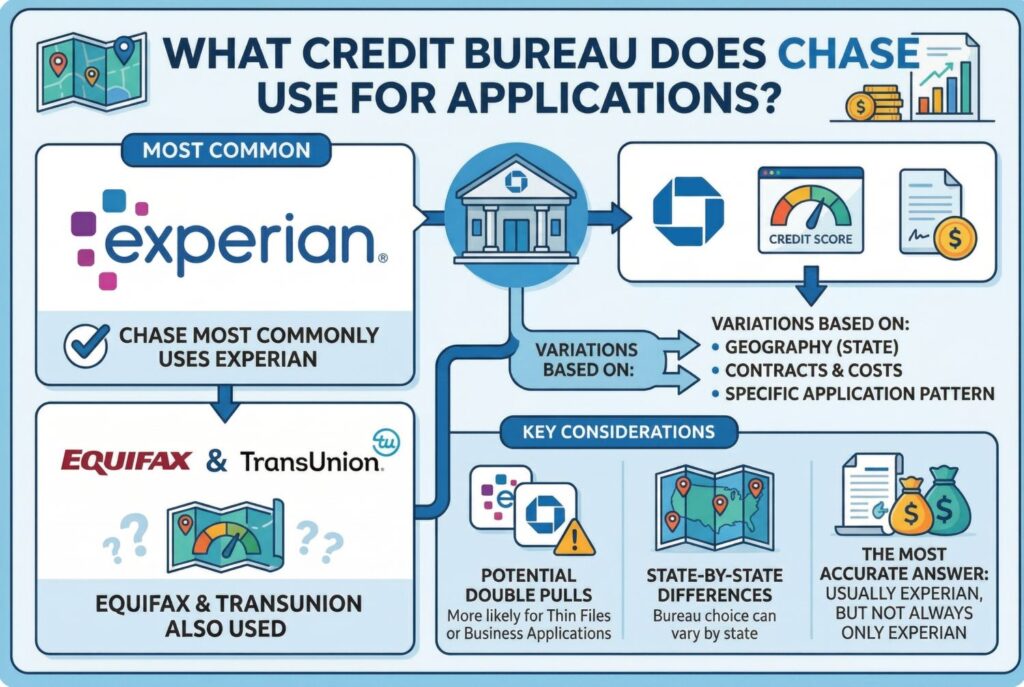

What Credit Bureau Does Chase Use for Applications?

This is where the official Chase material gets more general than many applicants want. Chase says issuers may use one or more of the three major bureaus: Experian, Equifax, and TransUnion. It also explains that bureau choice can vary based on geography, contracts, and cost.

In real-world application reports, Chase is most commonly associated with Experian, but Equifax and TransUnion do show up depending on the state and the specific application pattern being reported. Community tracking also shows that Chase can pull more than one bureau in some cases, which is why thin files or certain business-card applications sometimes create concern about a double pull. That’s why the most accurate answer to what credit bureau does chase use is this: usually Experian, but not always only Experian.

What Credit Score Do You Need for Chase Cards?

There isn’t one universal cutoff, but Chase’s lineup clearly breaks into tiers. Premium travel cards usually require stronger credit. The Chase Sapphire Preferred page currently promotes pre-approved offer checks, and applicants commonly treat the card as a good-to-excellent credit product. As a practical benchmark, many applicants target roughly the 670 to 700 plus range before trying for a Sapphire product, especially if they’re also watching utilization, recent inquiries, and account age.

Cash back cards such as Freedom cards also tend to favor solid credit, though they’re usually viewed as a bit more accessible than the premium Sapphire tier. For newer or rebuilding profiles, Chase itself highlights Freedom Rise as a starter card and says applicants who have never had a credit card may improve approval odds by having a Chase checking or savings account with at least $250 in qualifying funds. Chase also positions Slate Edge as a fair-credit product designed to help improve your score over time.

The Hidden Rule: Will Pre-Approval Bypass the Chase 5/24 Rule?

No. A Chase pre approval credit card offer doesn’t mean Chase’s broader approval rules disappear. The biggest one people talk about is 5/24, the idea that if you’ve opened five or more personal credit cards across issuers in the last 24 months, Chase often won’t approve you for another one. Chase doesn’t spell that rule out on its own consumer pages, but it remains one of the most widely cited approval filters in credit-card strategy content, and even prequalification articles warn that the tool doesn’t show your 5/24 status.

What to Do If You Have No Pre-Approved Offers

If nothing appears, don’t treat that as a permanent rejection. It can simply mean Chase doesn’t want to extend an offer right now. A smarter next move is to improve the parts of your profile you can control: pay down balances, avoid unnecessary new accounts, and consider building a stronger relationship with Chase if you’re new to the bank. That’s one reason Freedom Rise is so important for beginners. Chase explicitly says a qualifying Chase deposit relationship can improve approval chances for applicants with little or no card history. Slate Edge can also be a more realistic path for fair-credit applicants than jumping straight to a premium card.

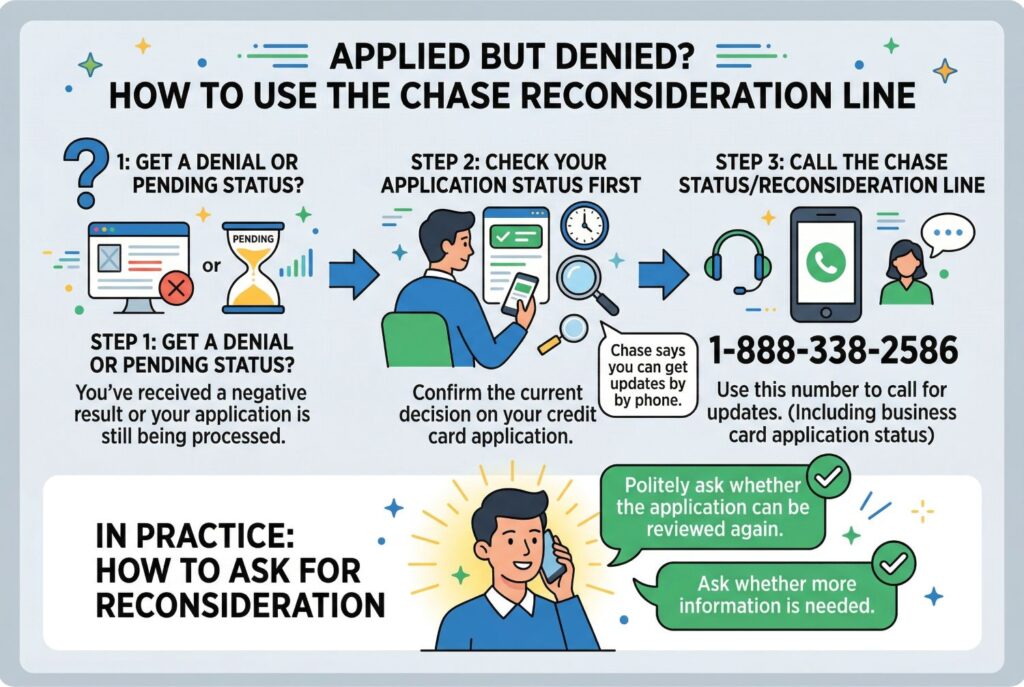

Applied but Denied? How to Use the Chase Reconsideration Line

If you already applied and got a pending or denied result, check your Chase credit card application status first. Chase says you can get updates by phone and lists 1-888-338-2586 as the number to call for status updates, including business card application status. In practice, many applicants use that same channel as the Chase reconsideration line by politely asking whether the application can be reviewed again or whether more information is needed.

Conclusion

The most practical sequence is simple. Start with the official chase credit card pre approval tool and use the soft pull to see whether you have offers. Then think about what credit bureau does Chase use in your state and whether your reports are ready for a hard pull. After that, make sure you aren’t likely to run into 5/24 trouble, choose the Chase card tier that actually fits your profile, and only then apply. That’s the smartest way to use a Chase pre approval credit card check without wasting an application.