If you’re checking your Chase credit card application status after getting a Chase credit card pre approval offer, the waiting can feel a lot worse than the application itself. You did the smart thing, you checked for offers first, you felt reasonably confident, and then the screen didn’t say approved. It said pending. That’s frustrating, but it also isn’t unusual. A pre-approval is helpful, not final, and a pending result often means Chase needs a little more time or a little more information before making the decision. The layout and keyword focus for this article come directly from your provided files.

The good news is that you don’t have to sit around guessing. There are clear ways to check your status, interpret Chase’s messages, and decide when it’s time to wait, when it’s time to call, and when it’s time to use the chase reconsideration line.

I Was Pre-Approved! Why Is My Chase Application Pending?

This is the part many applicants don’t expect. A Chase pre approval or credit card pre approval Chase offer is usually based on a softer early review of your profile. That first step helps Chase identify people who may be eligible, but it isn’t the same as full underwriting.

Once you actually submit the application, Chase can do a hard pull and review your profile much more closely. That’s when the process can slow down. A pending result doesn’t automatically mean rejection. It often means the bank wants to review something manually before giving a final answer.

There are a few common reasons this happens. Identity verification is a big one. If Chase sees something that looks inconsistent, even something as simple as an address mismatch, it may hold the application. Another reason is the 5/24 rule, where too many recently opened cards can create a problem even if the pre-approval looks encouraging. Income verification can also trigger a pause, especially if something in the application needs a second look. In some cases, your chase credit score expectations may not match the report Chase actually pulled for the final review. That gap between soft screening and final underwriting is why a pre-approved offer can still lead to a pending application.

3 Ways to Check Your Chase Credit Card Application Status

If your application is pending, the best thing to do is stop guessing and check it directly.

1. The Automated Status Phone Line

This is usually the fastest method. Call Chase’s automated application status line and follow the prompts. You’ll typically need to enter identifying details such as your Social Security number to hear the current status. This method is useful because it gives you an update immediately and often provides a timeline message that can tell you more than the word pending ever does.

2. Chase Online Banking Dashboard

If you already have a Chase checking account, savings account, or another Chase credit card, log in to your account and look for any application-related updates. Chase sometimes shows application details or sends follow-up requests through the online dashboard. This method is especially helpful if your application is tied to an existing relationship with Chase, since you may see alerts faster than waiting for a letter.

3. Secure Message or Email

Sometimes Chase follows up by asking for more information rather than making a decision right away. That’s why it’s important to check your email and any secure message center linked to your Chase account. If Chase needs identity documents or clarification, delays can drag out simply because the applicant never saw the request. If you’re actively waiting on your chase credit card application status, make checking those messages part of the process.

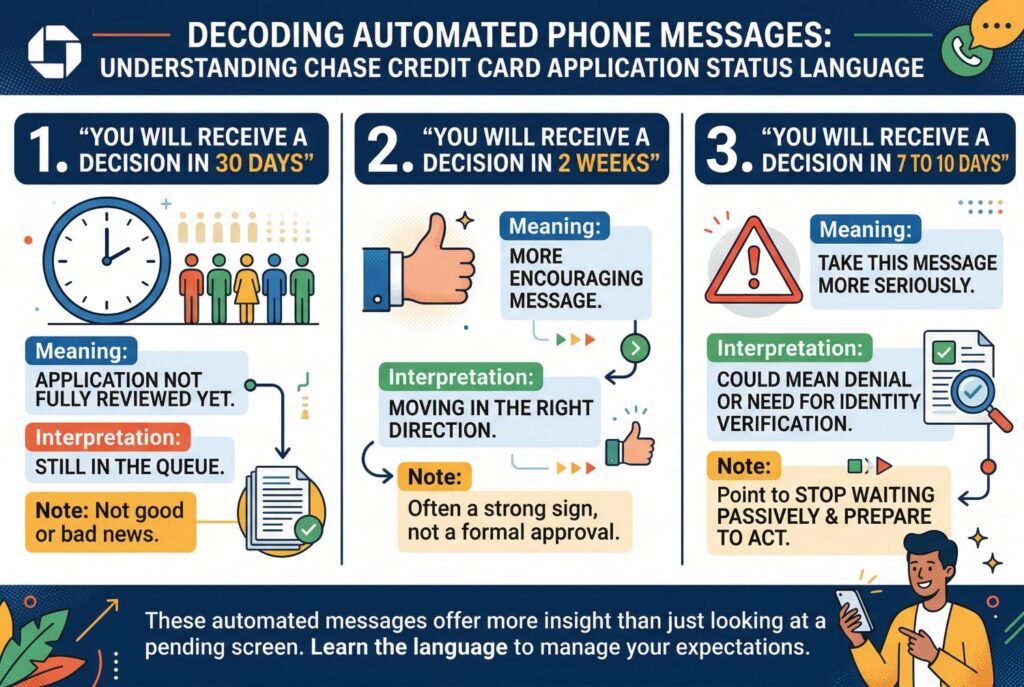

Decoding the Automated Phone Messages

One of the most useful parts of the process is learning how to read the automated status messages. Chase often doesn’t say approved or denied right away. Instead, it gives a timeline language, and that language can tell you a lot.

If you hear that you will receive a decision in 30 days, that usually means the application hasn’t been fully reviewed yet. It isn’t great news or bad news by itself. Most of the time, it just means you’re still in the queue. If you hear that you will receive a decision in 2 weeks, that’s often considered the more encouraging message. Many applicants treat that as a strong sign the application is moving in the right direction, even though it still isn’t a formal approval.

If you hear that you will receive a decision in 7 to 10 days, that’s the message people usually take more seriously. It can mean denial, or it can mean Chase needs identity verification before it can continue. Either way, it’s usually the point where you should stop waiting passively and prepare to act. These messages aren’t perfect, but they give you much more insight than just staring at a pending screen.

The Chase Reconsideration Line: How to Turn a Denial Into an Approval

If the status message looks bad or you receive a denial letter, this is where the chase reconsideration line becomes important. A reconsideration call is your chance to speak with a human being and explain the application. This matters because automated systems and basic underwriting rules don’t always capture the full context of your profile. If your income is stable, your recent inquiries have a reasonable explanation, or you want the card for a clear long-term purpose, a manual review can sometimes make a difference.

Before you call, prepare a short and calm explanation. You don’t need a dramatic story. You just need a credible reason for the card and a clear understanding of your own credit situation. A simple script can work well: you’re calling to ask whether your application can be reconsidered, you’re interested in building a longer-term relationship with Chase, and you’d be happy to clarify anything about your recent accounts, debt, or credit inquiries.

If your goal is something practical, say so. For example, if you wanted a card like Chase Freedom Rise to build credit with Chase over time, that’s a reasonable explanation. If you’ve opened several cards recently, be prepared to explain why. If your debts are manageable, say that clearly and calmly. The point of the reconsideration line isn’t to argue. It’s to give a real person the missing context.

What Credit Bureau Does Chase Use for the Final Hard Pull?

What credit bureau does Chase use? In many cases, applicants report that Chase pulls Experian most often, but it can also use Equifax or TransUnion depending on the state and the specific application context. That matters because the bureau used for the final hard pull may not match the assumptions you made when you were only thinking about pre-approval.

This helps explain why a chase pre approval result can feel more encouraging than the final application experience. If Chase reviews a different bureau for the hard pull, or finds weaker details there, the outcome can change. That’s one reason applicants sometimes feel blindsided.

The practical lesson is simple: don’t focus on just one credit report before applying. If you’re serious about Chase, it’s smarter to review all three bureaus, especially if your profile is thin or you’ve had recent activity that may report unevenly.

Conclusion

If your Chase application is pending, don’t assume the worst and don’t just wait blindly. First, check your chase credit card application status through the phone line, your online dashboard, or secure messages. Then pay attention to the timeline language, because those automated messages often reveal more than people realize. If the outcome turns negative, use the chase reconsideration line quickly and be ready to explain your application clearly. That’s the most practical way to handle the gap between pre-approval optimism and real application anxiety. Good luck with your Chase card.