If your banking app shows two different numbers and you’re wondering which one is your real money, you aren’t overreacting. The difference between ledger balance vs available balance matters because one number reflects the bank’s official record, while the other reflects what you can actually spend right now. That gap is exactly where confusion, declined transactions, and overdraft fees tend to happen.

A lot of people assume the bigger number is the safe one to use. That’s the mistake. Understanding which balance is static, which one is live, and why they don’t always match is one of the simplest ways to manage your bank balance more safely.

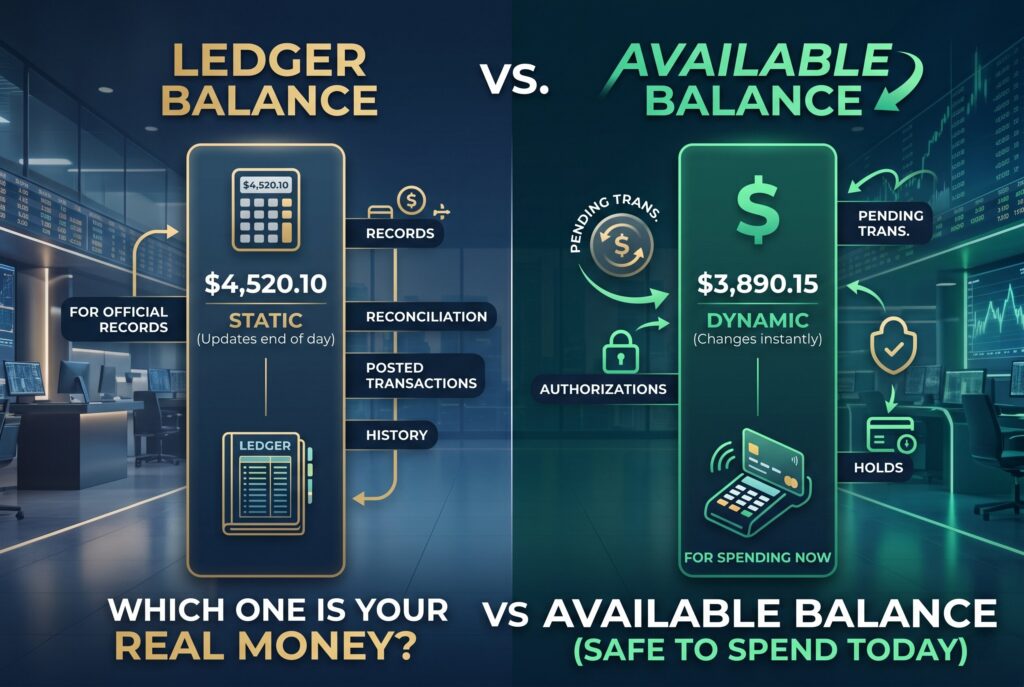

What Is a Ledger Balance? The Bank’s Historical Record

What is a ledger balance? Ledger balance is the official balance in your account at the end of the previous business day after all cleared transactions have been processed and posted. That’s the simplest ledger balance meaning in plain English. It’s the bank’s settled record of your account once completed credits and debits are officially entered into the books.

This is why ledger balance often feels a little behind real life. It doesn’t always reflect what happened in the last few minutes or even the last few hours. If you just swiped your debit card, received a pending transfer, or had a merchant place a temporary hold, that activity may affect your actual spending power before it fully changes the ledger side of the account. So ledger balance is useful, but it’s better understood as the historical record than as your real-time spending guide.

What Is Available Balance? Your Real Spending Power

Available balance is the amount of money you can actually withdraw, spend, or transfer right now. This is the live number. It changes more dynamically because it takes pending transactions, temporary holds, and certain deposit restrictions into account. In other words, it’s designed to reflect your real spending power at this moment, not just the official posted record from the end of the last business day.

That’s why the available balance is usually the more practical number for daily money decisions. If you’re about to make a purchase, withdraw cash, or send money, this is the balance that matters most. A useful way to remember it is this: ledger balance tells you what has officially cleared. Available balance tells you what is truly available to use.

Ledger Balance vs Available Balance: A Quick Comparison

The easiest way to compare ledger balance vs available balance is to break the difference into function. Ledger balance is more static. It updates after the bank processes and posts cleared transactions. Available balance is more dynamic. It changes as new authorizations, holds, and pending items affect what you can safely spend.

Ledger balance exists mainly for official account recordkeeping, reconciliation, and posted transaction history. Available balance exists to show what your usable account balance is right now.

In practical terms, if you want to know how your bank sees your settled account history, ledger balance matters. If you want to know whether you can safely make a purchase today, available balance matters more. That’s why asking which number is your real money has a simple answer for day-to-day spending. Your real money is the available balance, not the ledger number.

Why Don’t These Numbers Match? Three Common Reasons

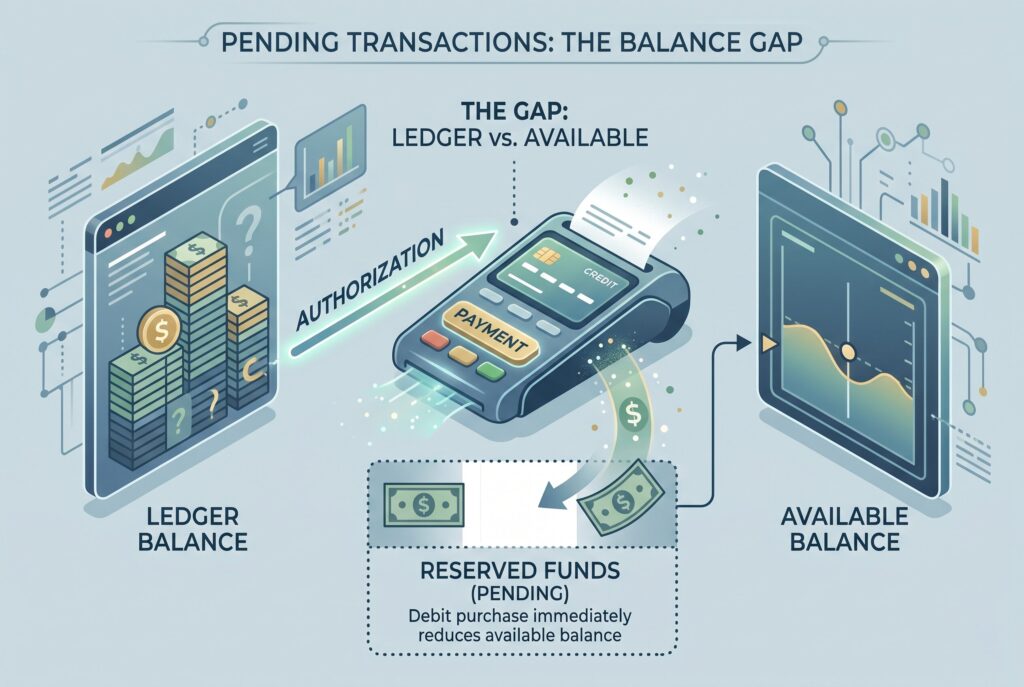

The reason these balances don’t match usually comes down to timing.

1. Pending Transactions

Pending transactions are one of the biggest causes of the gap. A debit purchase may immediately reduce your available balance, but not yet be fully posted to the ledger side of the account. The bank is already reserving that money, even if settlement hasn’t finished.

2. Temporary Holds

Hotels, gas stations, rental car companies, and some restaurants often place temporary holds. These holds reduce the amount you can use, even though the final charge hasn’t been posted yet. That means your available balance can drop while your ledger balance still looks stronger than it really is for spending purposes.

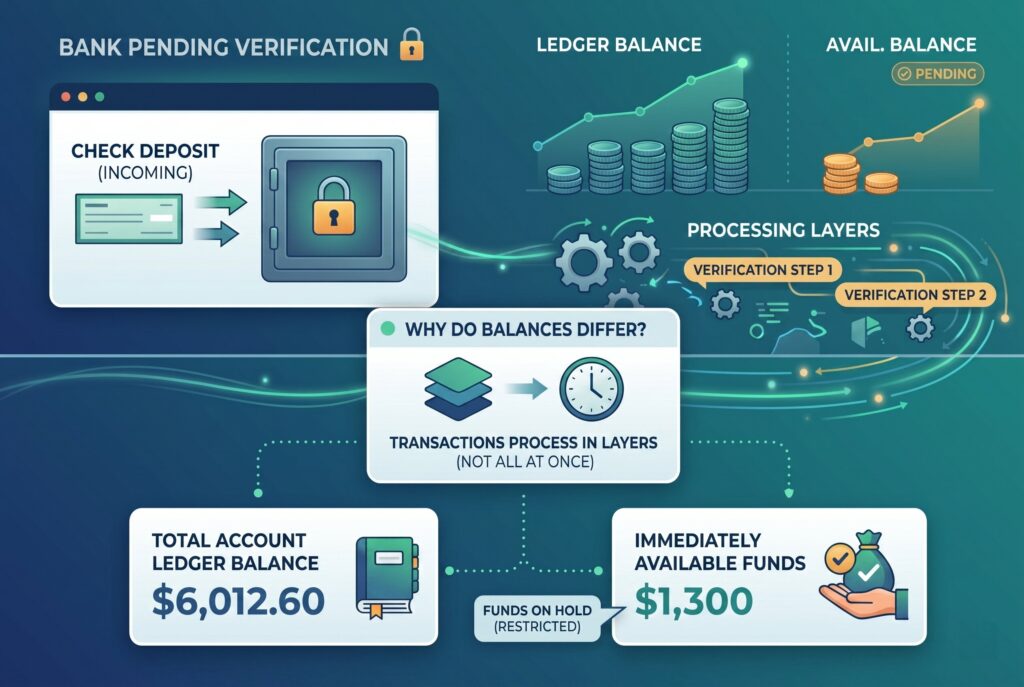

3. Deposits On Hold

Check deposits and some incoming transfers can also create a mismatch. A deposit may appear in account activity, but all or part of it may still be restricted until the bank finishes verification. In that situation, the ledger side and the available side can briefly tell two different stories. This is also why people ask why current and available balances sometimes show different amounts. The answer is basically the same: the bank processes transactions in layers, not all at once.

Which Number Is Your Real Money?

For spending, your real money is the available balance. That’s the expert advice most people need. If your goal is deciding whether you can safely buy something right now, available balance is the number to trust. It reflects the money you can actually use without stepping into a technical overdraft problem.

If your goal is reconciling books, reviewing official posted transactions, or working from the bank’s settled historical record, ledger balance is the legally official number. So the answer depends on the task. For spending decisions, available balance is real money. For recordkeeping and historical account status, ledger balance is the official number. The confusion happens when people use the official historical number for a real-time spending decision. That’s when the trouble starts.

How to Avoid Overdraft Fees When Balances Differ

Overdraft fees often happen because people look at ledger balance, assume the money is safe to use, and ignore what the available balance is already telling them. The safest rule is simple: never spend based on ledger balance alone. Use available balance as your spending guide.

A few habits make this easier:

- Set low-balance alerts in your banking app so you get warned before your usable balance gets too low.

- Leave a small cushion in the account if possible, especially if you use your debit card often or have recurring bills coming through.

- Learn your bank’s clearing cycle. Some banks update certain items faster than others, and knowing your own institution’s rhythm can reduce surprises.

- Watch autopay closely. A recurring bill can clear while other transactions are still pending, which creates the exact mismatch that leads to overdraft fees.

This is where how to manage bank balance becomes practical, not theoretical. The goal isn’t memorizing definitions. It’s avoiding mistakes caused by timing.

Conclusion

The simplest takeaway is this: don’t let the larger number fool you. Ledger balance is the official historical record. Available balance is your real-time spending power. If you’re trying to decide whether money is safe to use right now, available balance is the number that should guide you. That one shift can help you avoid overdraft fees, manage pending transactions more confidently, and make your account balance less confusing overall. When in doubt, trust the live number, not just the posted one.

Related Articles

Current Balance vs Available Balance: Why They Differ & How to Avoid Overdraft Fees