If you’ve ever checked your banking app, done the math in your head, and still felt like the numbers didn’t match, you aren’t imagining things. One of the most frustrating money questions people ask is, why wouldn’t every purchase you made show up on your account statement? The short answer is that card payments don’t move through the banking system in one instant step. They move in stages, and that delay is exactly why some charges feel invisible for a while.

This matters because those missing purchases can affect your real spending power before they fully appear on your credit card statement or bank account history. That’s also why people get confused by pending transactions, mismatched balances, and purchases that seem to appear late. Once you understand the system behind it, the whole thing becomes much easier to manage.

The Short Answer: Authorization vs. Settlement

When you swipe, tap, or enter your card online, the purchase usually goes through two stages. The first stage is authorization. This is when the merchant checks whether your card is valid and whether the account appears to have enough money or credit available. At this point, the transaction often becomes a pending transaction. The bank or card issuer is basically saying, “This purchase looks approved, so we’ll reserve room for it.”

The second stage is settlement. That’s when the merchant actually submits the finalized charge to collect the money. Settlement often happens later, sometimes in daily batches and sometimes after weekends or holidays. That gap between authorization and settlement is the main reason a purchase may not show up on your formal account statement right away. So if a purchase feels missing, it usually isn’t gone. It’s just sitting in the space between being approved and being fully posted.

4 Real World Reasons Your Purchase Is Missing

1. The Gas Station and Hotel Holds

Gas stations and hotels are classic examples of why purchases can look strange at first. At a gas station, the system often doesn’t know how much fuel you’re about to buy when you insert your card. So instead of posting the exact amount immediately, it may place a temporary hold for a larger estimate. Hotels do something similar for room charges, deposits, or incidentals.

That means the final amount may not appear on your account statement right away. Instead, a temporary hold affects your spending power first, and the real charge shows up later once the merchant finishes settlement.

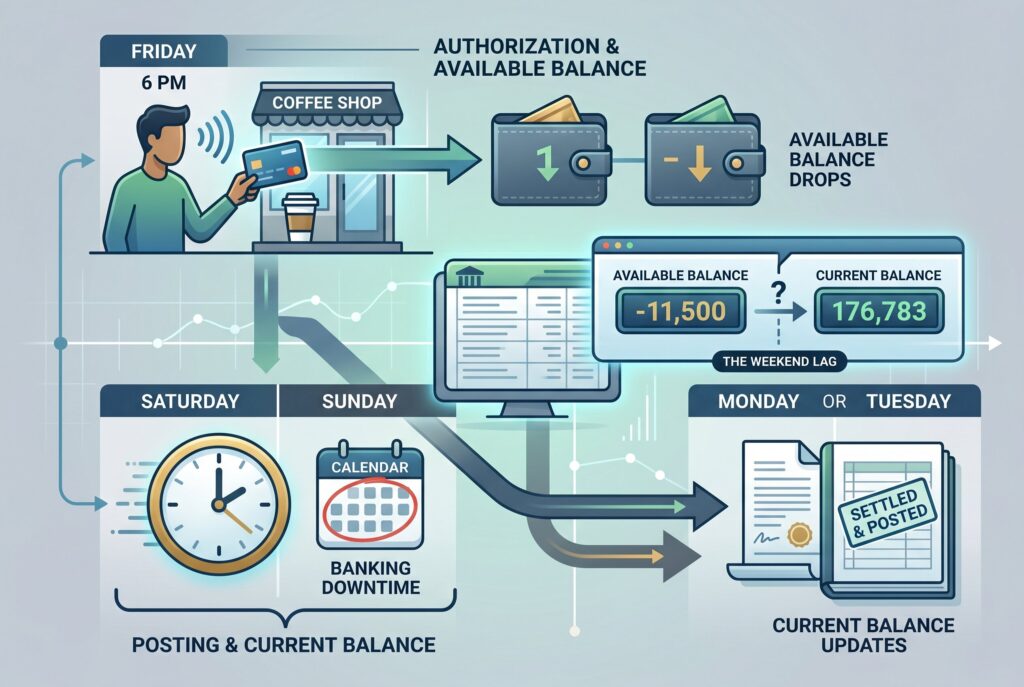

2. The Weekend Lag

Banks and merchants don’t always process transactions on the same timeline as your calendar. A purchase made late on Friday may not fully settle until Monday or even Tuesday, depending on weekends, holidays, and the merchant’s processing schedule. That’s why a charge can feel delayed even though you definitely made it already. The card was authorized, but the back-end movement of money didn’t fully finish yet.

This is one of the biggest answers to why current and available balances sometimes show different amounts of money in the same account. The available side often reacts faster than the official posted side.

3. The Statement Cut Off Date

This matters especially for credit cards. Your credit card statement closes on a specific date. If you make a purchase very close to that cut off, the charge may be authorized immediately but not settled in time to appear on that month’s statement. In that case, it moves into the next billing cycle instead.

So the transaction isn’t missing in a permanent sense. It simply didn’t finish posting early enough to make the statement that just closed. This is one reason people get confused when comparing statement balance vs current balance. A purchase can already be part of your live current balance while still being absent from the statement balance for that month.

4. Restaurant Tips

Restaurants are another easy place for timing confusion. When you first swipe your card, the authorization is usually for the meal amount before the tip is added. Later, once the tip is entered and the restaurant settles its daily batch, the final posted amount changes. That means the number you first see may not match the final charge that appears later on your account statement. This is completely normal, but it’s one more reason purchases can feel like they’re showing up in pieces instead of all at once.

The Balance Confusion: Current vs. Available

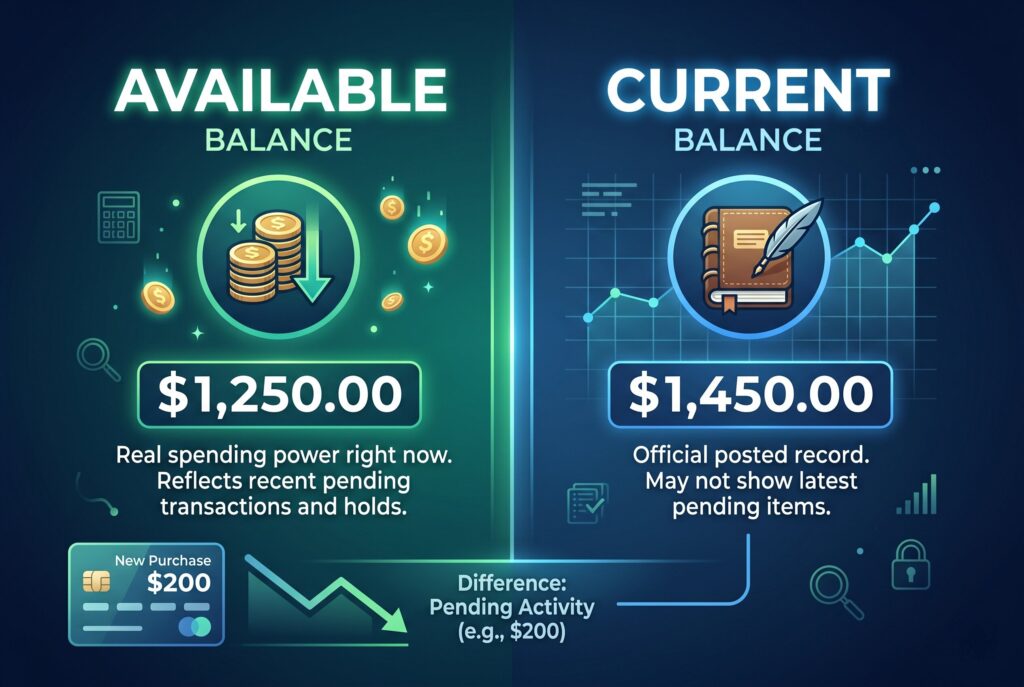

Pending transactions also explain why your balances can look inconsistent. Available balance is your real spending power right now. It usually reflects money already set aside for recent pending transactions, holds, or authorizations.

Current balance, or in some contexts ledger balance, is more like the official posted record. It may not fully reflect the newest pending items yet. That’s why the two numbers can show different amounts of money in the same account.

In practical terms, this means a purchase can reduce what you can safely spend before it fully appears in the historical record of the account. That’s the trap that leads a lot of people into overdrafts. They look at the bigger number, assume it’s all available, and forget that pending activity has already reduced their real usable balance.

Statement Balance vs Current Balance for Credit Cards

This distinction matters even more on credit cards. Statement balance is the fixed amount you owed at the end of the last completed billing cycle. That’s the number that appears on your monthly credit card statement. Current balance is the live total you owe now. It includes the statement balance plus newer purchases, minus payments, and any other posted activity since the statement closed.

So if a purchase is still pending when your billing cycle ends, it may not appear on that month’s statement balance even though it can still be part of the broader live picture you see in the app. That’s why statement balance vs current balance can feel confusing. One number is frozen in time for billing. The other keeps moving.

Conclusion

The safest habit is simple: rely on your available balance, not just the posted or historical numbers. If you’re trying to avoid overdraft fees, the available balance is the better guide because it reflects the money you can actually use right now. The larger posted number may look reassuring, but it can be misleading when pending transactions haven’t fully settled yet.

It also helps to turn on push notifications in your banking app. That way, you’ll know when a pending transaction actually posts, not just when it was first authorized. Watching those updates makes your account balance much easier to understand.

In the end, missing purchases usually aren’t truly missing. They’re just moving through a system that still works in stages. Once you understand authorization, settlement, and pending transactions, your bank’s math starts to make a lot more sense.