? SG&A Comparison")

Operating expenses are the day-to-day operating costs a business pays to stay open, serve customers, and manage its teams. Classifying these costs correctly matters more than ever because one mistake can distort margins, confuse tax planning, and make a healthy business look weaker than it is. This guide explains OpEx, SG&A, COGS, depreciation expense, and CapEx in plain English.

Interactive Tool: The Expense Classifier & Calculator

A useful expense classifier starts with three questions:

- Does this cost increase when production or client delivery increases?

- Does this cost support general business operations?

- Is this cost a long-term asset instead of a short-term expense?

If the cost supports daily operations, include it in OpEx. If it directly rises with production or delivery, it may belong in COGS. If it creates long-term value, it may be CapEx.

Example:

Revenue: $500,000

COGS: $200,000

Gross Profit: $300,000

Operating Expenses: $180,000

Operating Income: $120,000

Operating Margin = Operating Income / Revenue × 100

Operating Margin = $120,000 / $500,000 × 100 = 24%

That 24% margin tells you how much profit remains after core operating costs.

Expense Classifier & Calculator

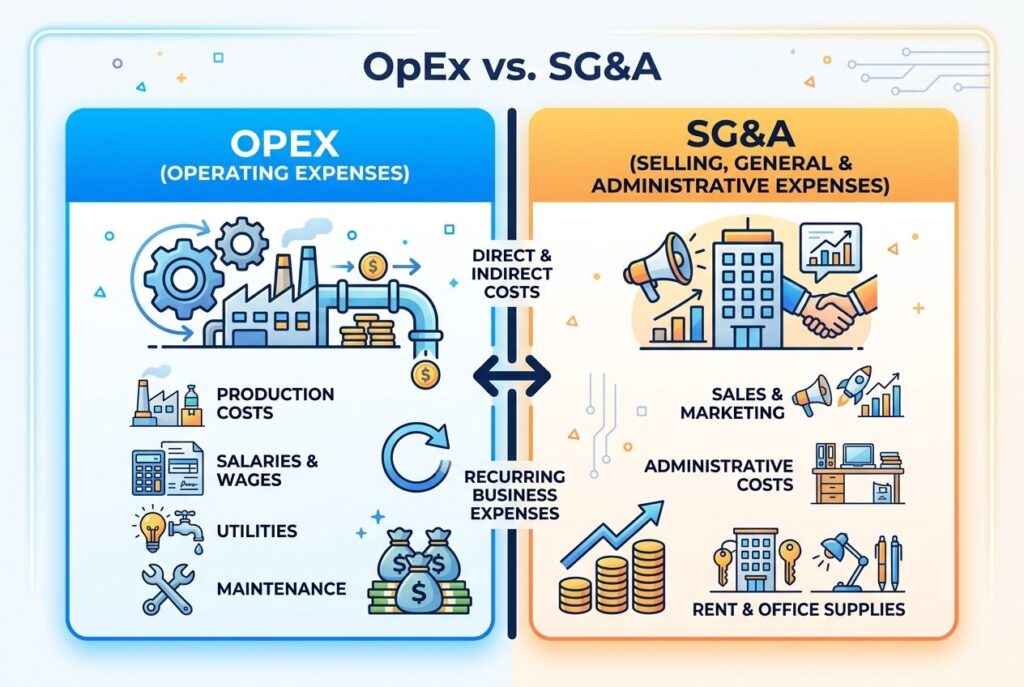

OpEx vs. SG&A: What Is the Difference?

What is SG&A? SG&A stands for selling, general, and administrative expenses. It includes costs related to selling products, running the office, and managing the company.

SG&A usually includes:

- Sales commissions

- Advertising and marketing

- Executive salaries

- HR, legal, and accounting

- Office rent

- Business insurance

- Administrative software

The main difference is that SG&A is usually a subcategory of operating expenses. Operating expenses can be broader, while SG&A focuses on selling and overhead functions. In many small businesses, agencies, and SaaS companies, people use OpEx and SG&A almost interchangeably because most overhead costs fall into selling, general, or administrative categories. Still, the cleaner view is this: all SG&A is usually OpEx, but not all OpEx is always SG&A.

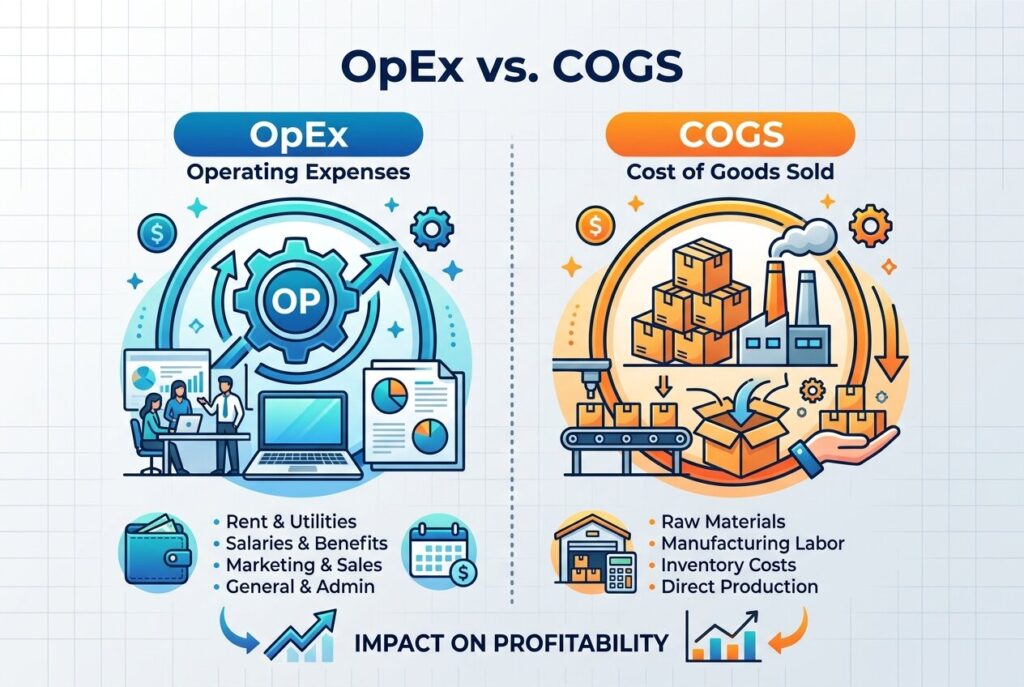

OpEx vs. COGS: The Golden Rule of Classification

COGS means Cost of Goods Sold. These are direct costs needed to produce or deliver what the company sells.

Use this rule:

If the cost increases because you deliver more client work or produce more units, it’s usually COGS. If the cost exists even when delivery pauses, it’s usually an operating expense. For example, raw materials for a product are COGS. Direct labor on a client project may also be COGS. But office rent, HR software, accounting fees, and general marketing campaigns are operating expenses because they support the whole business.

This distinction matters because COGS affects gross profit, while OpEx affects operating income. If you put delivery costs into OpEx by mistake, your gross margin may look too high. If you put overhead costs into COGS, your gross margin may look too low.

Is Depreciation an Operating Expense?

Is depreciation an operating expense? Yes, depreciation is generally considered an operating expense when it relates to assets used in daily operations. Depreciation expense represents the gradual wear and tear of long-term assets such as office equipment, computers, furniture, machinery, or vehicles. Instead of recording the full cost at once, the business spreads the cost across the asset’s useful life.

However, depreciation is a non-cash operating expense. That means it reduces accounting profit, but it doesn’t require a current cash payment in the same period. This is why depreciation is added back when calculating EBITDA. For example, if a company buys equipment for $50,000 and depreciates it over five years, it may record $10,000 of depreciation expense per year. The cash left the business when the equipment was purchased, but the expense appears gradually.

OpEx vs. CapEx

OpEx and CapEx are easy to confuse, but they work very differently. OpEx refers to short-term costs used in normal operations. These are usually fully deductible in the year they’re incurred. Examples include printer ink, monthly SaaS tools, rent, utilities, insurance, and routine maintenance. CapEx means capital expenditures. These are long-term investments that create value over multiple years. Examples include buying a building, purchasing a delivery van, upgrading major equipment, or investing in a large internal system.

The key difference is timing. OpEx is expensed quickly. CapEx is capitalized and depreciated over time. For tax planning, this distinction matters. A monthly software subscription may reduce taxable income immediately, while a major equipment purchase may need to be deducted gradually through depreciation.

3 Ways to Reduce Operating Costs

1. Run Subscription Audits

Many businesses waste money on unused SaaS tools, duplicate platforms, and old subscriptions nobody remembers approving. Review every recurring payment quarterly. Cancel tools that aren’t used, consolidate overlapping systems, and assign one owner to every subscription.

2. Improve Real-Time Spend Visibility

Expense reports often reveal problems too late. Corporate cards with spending limits, approval rules, and category controls can prevent waste before it happens. Real-time visibility also helps managers see which operating costs are rising before they damage margins.

3. Renegotiate Vendor Contracts

Inflation can push vendors to raise prices quietly. Review contracts for software, insurance, logistics, telecom, and professional services. For essential vendors, longer contracts may unlock better rates. For non-essential vendors, competitive quotes can create negotiating leverage.

Conclusion

Operating expenses aren’t just accounting labels. They show how much it costs to run the business, support customers, manage teams, and create future growth. Cutting operating costs can improve profit, but cutting the wrong costs can damage sales, service quality, or innovation.

The best approach is balance. Classify OpEx, SG&A, COGS, depreciation expense, and CapEx correctly. Track operating margin regularly. Reduce waste, but protect spending that supports durable growth. When operating expenses are managed well, they become a clear signal of operational health.