You just finished filing your taxes, then a strange tax form appears in your mailbox in May. It says Form 5498, and suddenly you wonder if you missed something important.

Take a breath. In most cases, IRS Form 5498 isn’t a problem. It’s an informational retirement account form that reports IRA activity to you and the IRS. Your financial institution sends it because it tracks IRA contributions, rollovers, Roth conversions, recharacterizations, and the account’s fair market value.

Form 5498, officially called IRA Contribution Information, reports money going into an IRA and certain account values. You usually don’t need to file Form 5498 with your tax return because your IRA custodian already sends it to the IRS.

Why Did I Receive the 5498 Tax Form in May?

The 5498 tax form often arrives later than W-2s, 1099s, or brokerage tax forms because IRA contribution timing is different. You can usually make prior-year IRA contributions up to the tax filing deadline, which is why custodians may not finalize Form 5498 until after April. IRS instructions show 2026 Form 5498 can report 2026 traditional IRA contributions made through April 15, 2027.

So if you receive tax form 5498 after filing, that doesn’t automatically mean your return is wrong. Review it for accuracy, keep it with your tax records, and only take action if the numbers conflict with what you reported.

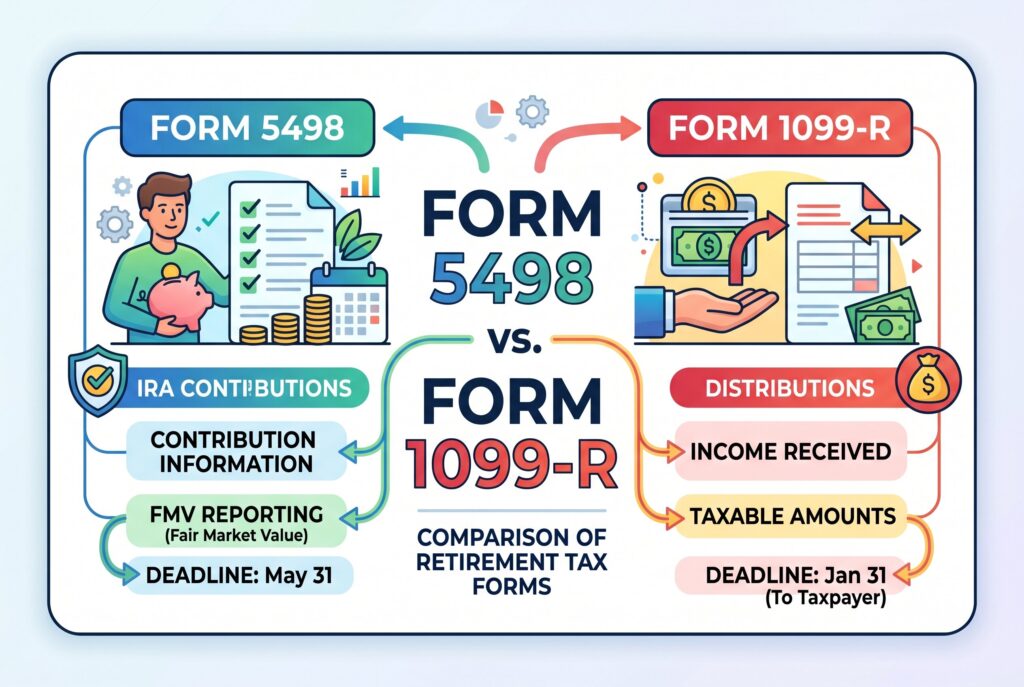

Form 5498 vs Form 1099-R: What’s the Difference?

The easiest way to understand Form 5498 vs 1099-R is this: Form 5498 reports money going into an IRA, while Form 1099-R reports money coming out.

Form 5498 may report IRA contributions, rollover contributions, Roth conversion amounts, recharacterizations, and fair market value. Form 1099-R reports distributions, withdrawals, pension payments, IRA distributions, and other retirement account payments that may need to appear on your tax return. The IRS explains that IRA contributions are reported on Form 5498, while distributions are reported on Form 1099-R.

Box by Box Breakdown: How to Read Your 5498 Form

- Box 1 usually shows traditional IRA contributions. This matters if you made deductible or nondeductible IRA contributions.

- Box 2 reports rollover contributions, such as money moved from an employer retirement plan into an IRA.

- Box 3 reports Roth IRA conversions. This is important for backdoor Roth or traditional to Roth conversion tracking.

- Box 4 reports recharacterized contributions, meaning a contribution was changed from one IRA type to another.

- Box 5 shows the fair market value of the IRA. This can matter for required minimum distributions and account reporting.

- Box 10 reports Roth IRA contributions. Box 11 indicates whether an RMD may be required for the following year.

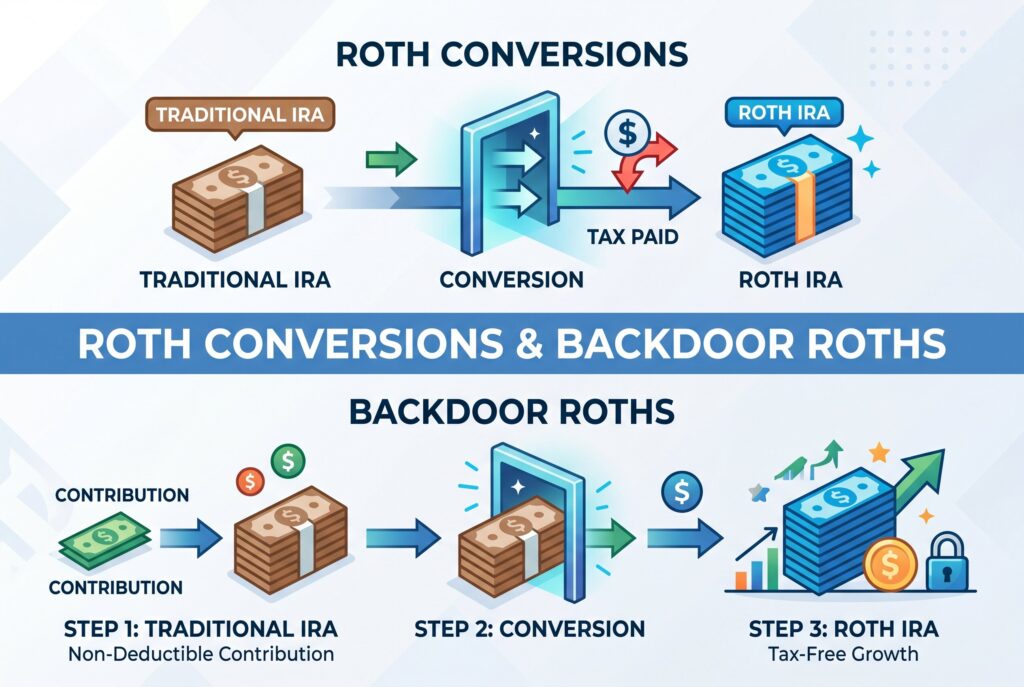

Special 2026 Scenarios: Roth Conversions and Backdoor Roths

A Roth conversion can generate more than one form. You may receive Form 1099-R for the distribution from the traditional IRA, then Form 5498 showing the conversion amount that went into the Roth IRA.

For a backdoor Roth IRA, this paperwork often confuses people. The 1099-R shows money leaving the traditional IRA. Form 5498 helps confirm that the money entered the Roth IRA as a conversion. If you made nondeductible traditional IRA contributions, you may also need Form 8606 with your tax return.

What to Do If You Spot a Mistake

If your 5498 form shows the wrong IRA contribution amount, rollover amount, or Roth conversion amount, contact your IRA custodian first. Don’t ignore the issue, because the IRS receives a copy too. For 2026, the IRA contribution limit increased to $7,500, with a catch-up limit of $8,600 for people age 50 or older. If your form shows an excess contribution, you may need to correct it. Excess IRA contributions can trigger a 6% excise tax if not fixed properly, so ask the custodian or tax professional how to remove or reclassify the excess.

Frequently Asked Questions

Does a 401(k) generate a Form 5498?

Usually no. Form 5498 is for IRAs, including traditional, Roth, SEP, and SIMPLE IRAs. A 401(k) tax form situation is usually handled through your W-2 for contributions and Form 1099-R for distributions.

What if I lost my Form 5498?

Log in to your brokerage or custodian account and download a copy. You can also request a replacement.

Do I need to file Form 5498 for an inherited IRA?

Usually you don’t attach it to your return, but you should keep it. Inherited IRA reporting can affect RMD tracking and account records.

Conclusion

Form 5498 looks intimidating, but most taxpayers only need to review it and store it safely. It’s mainly proof of IRA contributions, rollovers, conversions, and fair market value. Use it to confirm your records, especially if you made a Roth conversion, backdoor Roth IRA contribution, rollover, or nondeductible IRA contribution. If everything matches, file it away with your tax documents. If something looks wrong, contact your custodian before assuming you need to amend your return.

Related Articles

IRS Form 1040 Explained: What It Is, Who Must File, and How to Complete It Correctly