The 2026 FSA contribution limits are higher, giving employees and families more room to set aside pre-tax money for healthcare, childcare, and commuting costs. For anyone preparing for open enrollment, the key question isn’t only “What’s the FSA max 2026?” It’s also how to use these limits wisely without overfunding an account or leaving money behind.

Interactive Tool: The 2026 FSA Tax Savings Estimator

A good FSA decision starts with a simple estimate. Add up your predictable expenses: prescriptions, doctor visits, dental work, glasses, contacts, therapy copays, or planned procedures. Then multiply your expected FSA election by your combined tax rate.

For example, if you contribute $2,000 and your combined tax rate is around 25%, your estimated savings could be about $500. That’s why understanding how does FSA work can make a real difference. The money isn’t a bonus, but the tax savings can feel like one.

2026 FSA Tax Savings Estimator

Use this estimator to plan a flexible spending account election. Add predictable expenses such as prescriptions, doctor visits, dental work, glasses, contacts, therapy copays, or planned procedures. Then enter your expected FSA election and combined tax rate to estimate tax savings.

Predictable Healthcare Expenses

FSA Election and Tax Rate

Total Predictable Expenses = Prescriptions + Doctor Visits + Dental Work + Vision + Therapy Copays + Planned Procedures

Estimated Tax Savings = FSA Election × Combined Tax Rate

Potential Overfunded Amount = FSA Election − Total Predictable Expenses, if positive

After-Tax Cost of Covered Expenses = FSA Election − Estimated Tax Savings

Note: This calculator is for educational planning only. FSA rules, eligible expenses, carryover amounts, grace periods, contribution limits, and use-it-or-lose-it rules may vary by employer plan.

The Complete 2026 Benefit Limits Table

| Account Type | 2026 Contribution Limit | Carryover Rule |

| Health FSA | $3,400 per employee | Up to $680, if allowed |

| Limited-Purpose FSA | $3,400 per employee | Up to $680, if allowed |

| Dependent Care FSA | $5,000 per household | No carryover |

| Commuter/Transit | $340 per month | Usually rolls month to month |

Understanding the Health FSA: The $3,400 Maximum

A Health FSA helps pay for eligible medical, dental, and vision expenses with pre-tax dollars. The 2026 health FSA contribution limit is $3,400, but your employer can set a lower plan limit.

One feature many employees overlook is the uniform coverage rule. If you elect $3,400 for 2026, the full amount is generally available on the first day of the plan year, even though payroll deductions happen gradually. That can be useful if you expect a major expense early in the year, such as orthodontics, Lasik, or a planned surgery.

People often ask what is FSA and HSA because both accounts offer tax advantages. The simplest difference between FSA and HSA is ownership and eligibility. An FSA is employer-owned and usually tied to your job. An HSA is individually owned and requires enrollment in a qualified high-deductible health plan. In the HSA vs FSA decision, the “best” option depends on your health plan, expected expenses, and whether you want long-term savings flexibility.

Dependent Care FSA: Rules for Families

A Dependent Care FSA, or DCFSA, is designed for care that allows you and your spouse, if married, to work or look for work. Eligible expenses may include daycare, preschool, before- and after-school care, day camps, nanny care, and adult dependent care.

The key rule is that the $5,000 limit applies per household, not per parent. Two spouses can’t each contribute $5,000 for the same household. If you’re married filing separately, the limit is $2,500.

DCFSA money also works differently from a Health FSA. You generally can’t access the full annual election on January 1. Funds become available as payroll deductions are deposited. That means families should plan contributions around real childcare costs and timing.

The Use It or Lose It Rule & 2026 Exceptions

The biggest hesitation around FSAs is the use-it-or-lose-it rule. In simple terms, unused money may be forfeited after the plan year unless your employer offers an exception.

There are two common exceptions. The first is a grace period, which may give you up to 2.5 extra months to spend prior-year funds. For 2026 funds, that could extend spending through March 15, 2027. The second is carryover, which lets you move up to $680 into the next plan year. Your employer can offer a grace period or carryover, but not both. Some plans offer neither. That’s why employees should check the plan documents before choosing an election amount.

Commuter Benefits: The New $340 Monthly Limit

The commuter benefits limit 2026 is $340 per month for transit and $340 per month for qualified parking. These are separate monthly limits, which can help employees who use public transportation, parking garages, commuter rail, buses, or vanpools.

This benefit is especially useful for hybrid workers because elections may be easier to adjust month to month than healthcare FSA elections. Instead of choosing the annual maximum automatically, employees should estimate actual commuting days. A person going to the office twice a week may need far less than someone commuting five days a week.

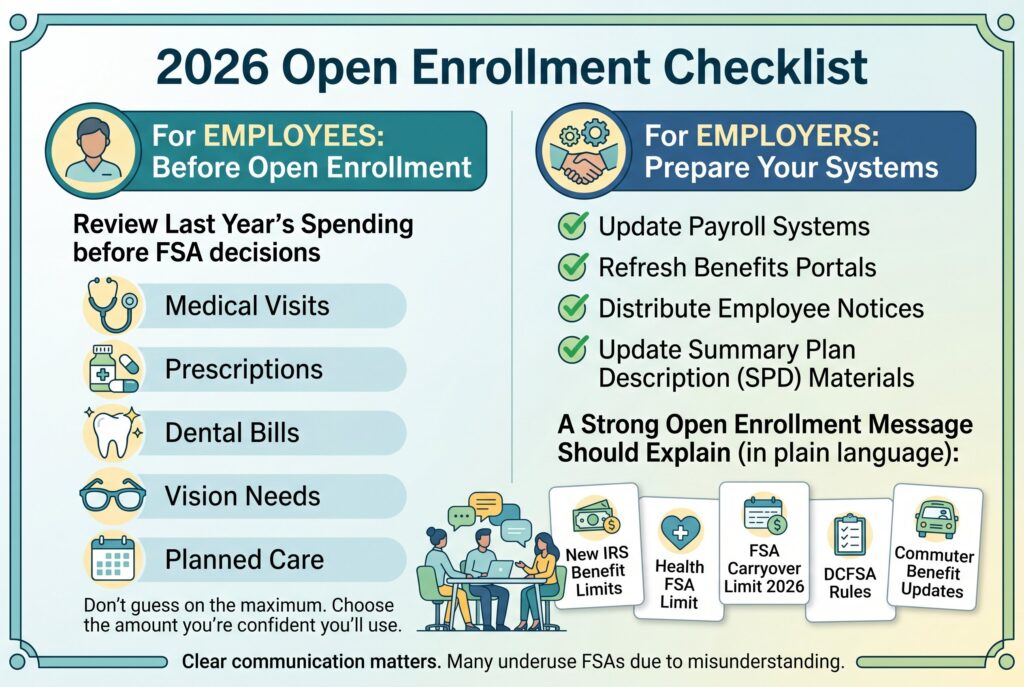

2026 Open Enrollment Checklist for Employers & Employees

Employees should review last year’s spending before open enrollment FSA decisions. Look at medical visits, prescriptions, dental bills, vision needs, and planned care. Don’t guess based only on the maximum. The smartest election is usually the amount you’re confident you’ll use.

Employers should update payroll systems, benefits portals, employee notices, and Summary Plan Description materials before open enrollment begins. Clear communication matters. Many employees underuse FSAs because they don’t understand eligible expenses, deadlines, or the carryover rule. A strong open enrollment message should explain the new IRS benefit limits, the health FSA limit, the FSA carryover limit 2026, DCFSA rules, and commuter benefit updates in plain language.

Conclusion

The 2026 FSA limits create a real opportunity to reduce taxes on predictable expenses. A Health FSA can make medical costs easier to manage. A Dependent Care FSA can help families offset childcare costs. Commuter benefits can soften the cost of returning to the office. The best move is simple: estimate carefully, check whether your employer offers carryover or a grace period, and choose an amount that fits your life. An FSA isn’t about spending more. It’s about paying smarter.