Can checking accounts generate interest? In some cases, yes, but many standard checking accounts either pay nothing or offer rates so low that they make little difference. A stronger alternative is a high yield checking account. With this type of account, your everyday balance can earn a more noticeable return while you continue to use it for daily needs like paying bills, making transfers, using a debit card, or receiving direct deposits. This approach offers a practical way to make better use of idle cash while keeping your money fully accessible.

Can You Earn Interest on a Checking Account?

Yes, you can earn interest on a checking account, but it depends on the account type. Standard checking accounts at large traditional banks often pay 0.01% APY or nothing at all. That means your balance may sit there all year without producing meaningful earnings.

To actually earn more, you usually need an upgraded interest-bearing account, often called a high yield checking account or high interest checking account. These accounts are designed for people who want everyday access to their money while still earning a competitive Annual Percentage Yield, or APY. The key is simple: not all checking accounts are built to earn. You need to choose one that clearly advertises interest or APY.

What is a High Yield Checking Account?

A high yield checking account is an everyday spending account that pays a higher APY than a normal checking account. It works like a regular checking account, but with one major advantage: your balance can earn interest. You can usually use a high yield checking account for debit card purchases, ATM withdrawals, direct deposit, online bill pay, mobile banking, transfers, and checks. In other words, it doesn’t force you to give up everyday access.

A high interest checking account is basically the same idea. The name may vary by bank or credit union, but the goal is the same: help your checking balance earn more while staying liquid. This makes high yield checking useful for money you plan to spend soon, such as rent, groceries, utilities, subscriptions, gas, and other monthly expenses. Instead of letting that cash sit in a zero-interest account, you can earn something while keeping it ready to use.

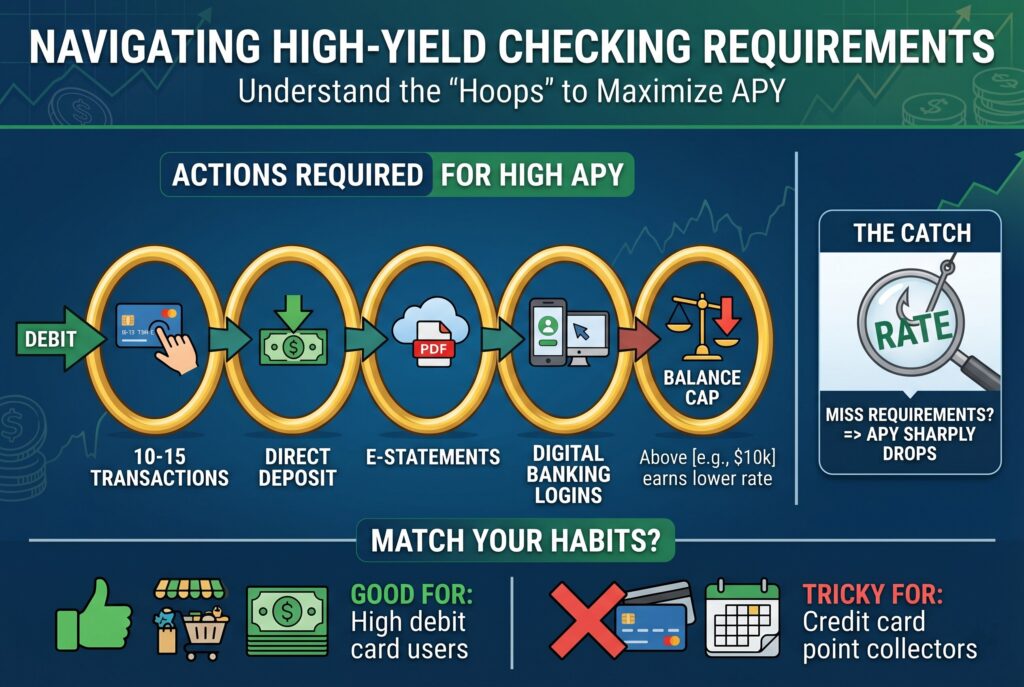

The Catch: Understanding the Hoops and Requirements

High yield checking sounds simple, but there’s usually a catch. Banks and credit unions often require specific monthly actions before you qualify for the highest APY. Common requirements include making 10 to 15 debit card purchases per month, setting up a qualifying direct deposit, enrolling in e-statements, using online or mobile banking, or keeping your balance below a certain cap.

That last point matters. Some accounts advertise a very high APY, but only on the first portion of your balance. For example, the high rate may apply only up to $10,000 or $15,000. Any money above that amount may earn a much lower rate.

You should also check what happens if you miss the requirements. Some high yield checking accounts drop your APY sharply for that month if you don’t meet the rules. So before opening one, ask yourself whether the required activity matches your real spending habits. If you already use your debit card often and receive direct deposit, the hoops may be easy. If you mainly use credit cards for rewards, the debit card requirement may become annoying.

See Your Earnings: High-Yield Checking Calculator

High-Yield Checking Calculator

Compare your current checking account with a high-yield checking account. Enter your average balance, current APY, new APY, balance cap, and whether you expect to meet the qualification rules.

Current Earnings = Average Balance × Current APY

High-Yield Earnings = Eligible Balance × High-Yield APY + Balance Above Cap × Fallback APY

Extra Earnings = High-Yield Earnings − Current Earnings

A high-yield checking calculator should help you compare a normal checking account with a high yield checking account. You would enter your average balance, the APY on your current account, and the APY on the new account.

For example, suppose you keep an average balance of $8,000 in checking. If your current account pays 0.01% APY, you’ll earn almost nothing. If a high yield checking account pays 3.00% APY on that balance, your annual earnings could be around $240 before taxes. That isn’t life-changing money, but it’s still money you may be leaving behind. The calculator should also include balance caps and qualification rules, because the highest advertised APY isn’t always the rate you’ll actually earn.

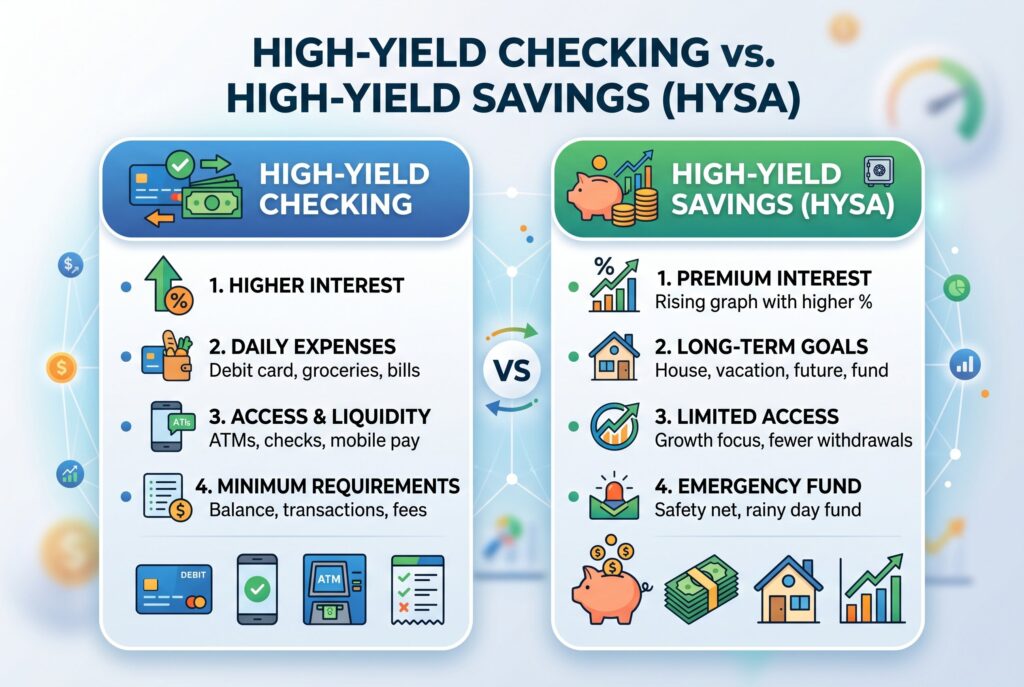

High-Yield Checking vs. High-Yield Savings HYSA

High-yield checking and high-yield savings accounts both help your money earn interest, but they serve different purposes. High-yield checking is best for money you need to spend this month. It’s useful for rent, groceries, utilities, subscriptions, and daily transactions. It offers more payment flexibility, but it may require debit card usage or direct deposit to unlock the best rate.

A high-yield savings account, or HYSA, is better for emergency funds, short-term savings goals, travel funds, or money you don’t need to touch every day. It often has fewer spending features, but it may offer strong APY with fewer monthly transaction hoops.

The best strategy may be to use both. Keep spending money in high yield checking and savings money in a HYSA. That way, your everyday cash stays accessible while your larger reserves continue earning interest.

How to Find the Best High Yield Checking Accounts

To find the best high yield checking accounts, don’t only look at the highest APY. A flashy rate may come with strict rules, low balance caps, or fees that reduce your real earnings. Start with monthly fees. A good account should have no monthly maintenance fee or an easy way to waive it. Paying $10 a month in fees can erase much of the interest you earn.

Next, compare APY and balance caps. A high APY is helpful only if it applies to the amount you actually keep in checking. If the rate drops after a small balance limit, calculate your real blended return. Then review ATM access. Look for accounts with a broad ATM network or reimbursement for out-of-network ATM fees.

Finally, check qualification requirements. The best account is one you can actually use. If you won’t make enough debit card purchases or direct deposits, the advertised rate doesn’t matter.

Conclusion

Checking accounts can earn interest, but the account type matters. A standard checking account usually won’t do much for your money. A high yield checking account can turn everyday cash into a small but steady source of passive earnings.

Before switching, compare APY, fees, balance caps, ATM access, and monthly requirements. The right account should fit your habits, not force you into a complicated routine. When used wisely, high yield checking helps your everyday money stay flexible, accessible, and productive.