Family car insurance sounds like a single special policy, but in most cases, it’s really a practical way to organize several drivers, several cars, or both under one household insurance setup. A family may use multi car insurance, a multi vehicle policy, named driver insurance, additional driver insurance, or temporary cover depending on who drives, how often they drive, and where the vehicles are kept.

The quick verdict is simple. If your household has two or more vehicles, or multiple legal drivers living at the same address, combining coverage can make your insurance easier to manage and may unlock a multi car insurance discount. In many cases, insurance savings can range from about 10% to 25% of the household’s annual premium, especially when you combine a multi car policy with other bundled insurance policies such as homeowners or renters insurance. The goal is to insure the right person on the right car, avoid legal mistakes, protect your no claims history where possible, and keep your family’s cash flow steady when repair costs, teen driver insurance, and rising premiums put pressure on the budget.

What Is Family Car Insurance and Who Qualifies?

Family car insurance is a general term used for insurance arrangements that cover multiple drivers, multiple vehicles, or both within the same household. It can work for married couples, parents with teenage drivers, households with adult children, and in some cases even unrelated adults who share an address. Most insurers require vehicles to be primarily kept at the same residence to qualify for multi-car insurance. This requirement exists because location plays a major role in determining insurance risk. Vehicles parked in lower-risk neighborhoods or secured garages may receive different rates than those regularly parked in busy urban areas.

Family coverage is especially common among married couples because they often share vehicles and financial responsibilities. However, marriage is not always required. Eligibility typically depends on residency, vehicle ownership, and accurate disclosure of all household drivers. If you plan to add family members to a policy, provide complete and accurate information about who drives each vehicle, how often they drive, and where they live. Misrepresenting driver information can create serious problems if a claim occurs.

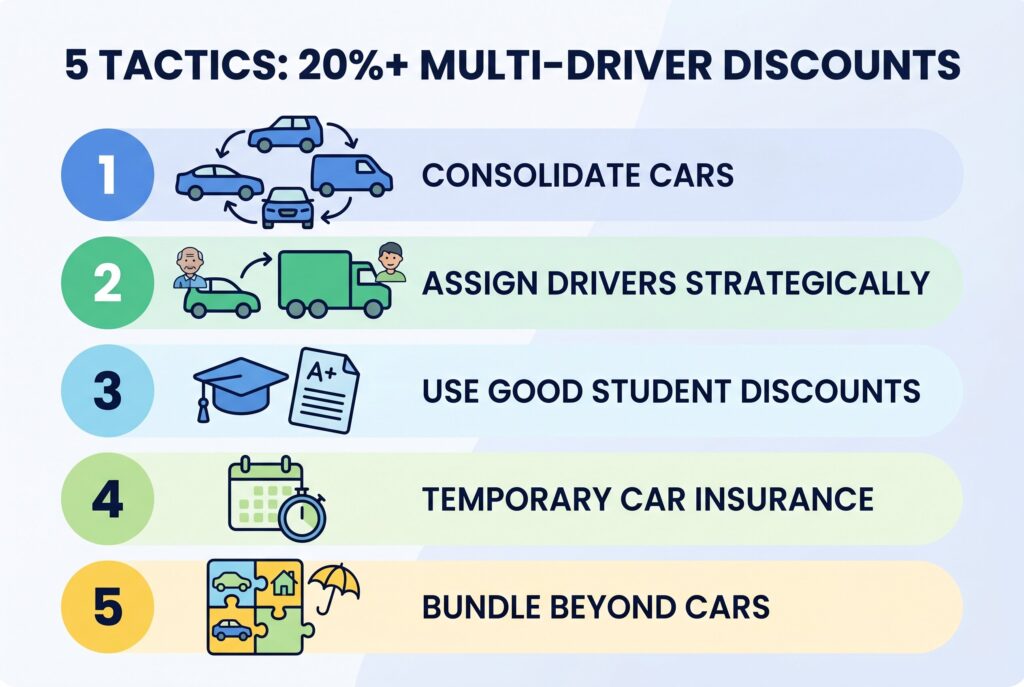

5 Tactics to Unlock 20%+ Multi Driver Discounts

1. Consolidate Cars Into One Multi Car Policy

One of the easiest ways to reduce insurance costs is to combine household vehicles under a single multi-car policy. Rather than managing separate policies for each vehicle, families can place multiple cars on one account and potentially qualify for a multi-car discount.

Each vehicle can still have customized coverage based on its value and usage. For example, a newer SUV may carry comprehensive and collision coverage, while an older vehicle may only need basic liability protection. This flexibility allows families to balance protection and affordability while benefiting from household discounts. Depending on the insurer, multi-car discounts can reduce premiums by approximately 5% to 25%. The greatest savings are often available to households with multiple vehicles registered and garaged at the same address.

2. Assign Drivers Strategically

Adding a teen driver can significantly increase household insurance costs. One way to manage those costs is by accurately matching drivers with the vehicles they use most often. For example, if a teenager primarily drives an older compact car to school and work, they should be listed as the primary driver of that vehicle. Assigning them to a newer or more expensive vehicle they rarely use could unnecessarily increase premiums. The goal isn’t to manipulate the policy but to ensure it accurately reflects real driving habits. Proper driver assignment can help control costs while keeping coverage valid and avoiding complications during the claims process.

3. Use the Good Student Discount

Many insurers offer discounts for students who demonstrate strong academic performance. If a teen or college-aged driver maintains a qualifying GPA, often around a B average or higher, the household may be eligible for additional savings. Because young drivers typically carry higher insurance costs, even a modest student discount can help offset part of the premium increase. Families should keep transcripts, report cards, or enrollment documentation available when requesting this discount.

4. Consider Temporary Cover for Occasional Drivers

Not every family member needs to be permanently listed on a policy. If a college student returns home for a holiday break or a visiting relative needs short-term access to a vehicle, temporary car insurance may be a practical solution. Temporary coverage can sometimes help preserve the primary policyholder’s claims history because it operates separately from the annual policy. However, it generally works best for short-term situations. If someone drives the vehicle regularly throughout the year, a named driver arrangement or permanent policy addition is usually more appropriate. For occasional borrowing, holiday visits, or temporary driving needs, short-term coverage may provide flexibility without requiring permanent policy changes.

5. Bundle Beyond Cars

Families often overlook additional savings opportunities outside of auto insurance. Bundling car insurance with homeowners, renters, RV, motorcycle, or umbrella policies can sometimes unlock larger discounts and simplify household finances.

Bundling may reduce the number of bills, streamline renewals, and improve overall policy management. However, families should always compare the final combined cost against separate quotes. A bundled package only delivers value when both the coverage and pricing remain competitive. In many cases, bundling multiple insurance products can reduce overall insurance expenses by 10% to 25%.

The Legal Red Line: The Danger of Fronting

Fronting occurs when a parent or experienced driver is listed as the primary driver of a vehicle that is actually used most often by a younger or higher-risk driver. Families sometimes do this in an attempt to reduce premiums, but insurers consider it a form of insurance fraud.

If an accident occurs, insurers may investigate who regularly drives the vehicle, where it is parked, commuting patterns, annual mileage, and other usage details. If they discover that the declared primary driver isn’t the person who actually uses the vehicle most often, they may deny the claim, cancel the policy, or classify the household as higher risk. The financial consequences can be severe. A denied claim could leave a family responsible for repair costs, medical expenses, legal fees, and liability damages that far exceed any short-term insurance savings.

Conclusion

Family car insurance works best when it reflects real life. The right setup might be multi car insurance for a household with several vehicles, named driver insurance for a spouse or child who regularly uses one car, learner driver insurance for practice, or temporary cover for a student home on break.

The smartest families don’t just chase the cheapest quote. They review who drives each vehicle, compare deductibles, ask about a good student discount, avoid fronting, and look for a multi car insurance discount that doesn’t weaken coverage. When done correctly, family auto insurance can reduce stress, unlock insurance savings, and keep everyone protected on the road in 2026.

Related Articles

How Long Does It Take To Get Car Insurance? Drive Off Today in 2026

Can I Cancel My Car Insurance At Any Time? 2026 Refund Rules