: 2026 Benchmarks & Formula")

Investing in stocks instead of risk-free government bonds means accepting uncertainty in exchange for the potential for higher returns. Understanding how investors are compensated for that additional risk is essential in modern finance, particularly when estimating required returns, valuing companies, and making capital allocation decisions. In 2026, changing interest rate expectations, inflation concerns, and evolving market sentiment continue to influence how investors assess risk and reward. As a result, analysts can’t rely solely on historical averages or simple assumptions. A thorough understanding of market conditions, forward-looking expectations, and sensitivity analysis is necessary to produce realistic and defensible valuation outcomes.

What Is the Market Risk Premium?

The market risk premium definition is the additional return investors require for taking that risk. In simple terms, it’s the reward for leaving the safety of risk free assets and entering the stock market. Market risk premium is central to CAPM, cost of equity, required return, and valuation work.

Deconstructing the Market Risk Premium Formula

The basic market risk premium calculation looks simple.

MRP = Expected Market Return − Risk Free Rate.

Expected market return is the return investors expect from the overall stock market. In the United States, analysts often use the S&P 500 as a proxy for the broad market. Risk free rate is the return available from an investment considered nearly free of default risk. In U.S. valuation work, many analysts use the 10 year Treasury yield because it reflects a long term benchmark and matches the longer horizon of many equity investments.

For example, if investors expect the stock market to return 9% and the risk free rate is 4%, the market risk premium is 5%. That 5% represents the extra compensation investors demand for choosing equities over safer bonds.

How MRP Fits Into CAPM

Market risk premium becomes especially important inside CAPM, the Capital Asset Pricing Model.

CAPM estimates cost of equity using this structure:

Cost of Equity = Risk Free Rate + Beta x Market Risk Premium.

Beta measures how sensitive a company’s stock is to the broader market. A beta of 1 means the stock moves roughly with the market. A beta of 1.5 means the stock is more volatile. A beta below 1 means the stock is less volatile.

This is why MRP matters so much. It doesn’t affect every company equally. It gets multiplied by beta. A defensive utility company with beta of 0.7 won’t be as sensitive to an MRP change as a high growth technology company with beta of 1.6.

2026 Benchmarks: What Number Should You Actually Use?

There isn’t one perfect market risk premium for every model. Different analysts use different methods depending on the purpose of the valuation.

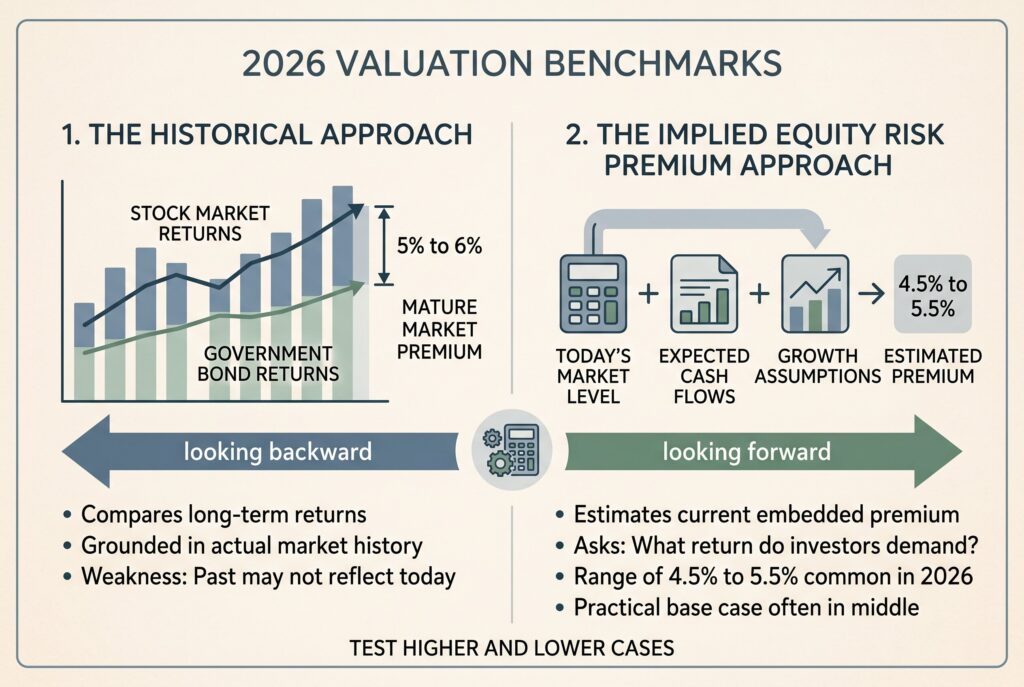

1. The Historical Approach

The historical method looks backward. It compares long term stock market returns with long term government bond returns. Over many decades, this often produces a mature market premium somewhere around 5% to 6%. The advantage is that it’s grounded in actual market history. The weakness is that history doesn’t always reflect today’s valuation environment. If rates, inflation, profit margins, or investor expectations shift, the past may not be the best guide.

2. The Implied Equity Risk Premium Approach

The implied equity risk premium looks forward. Instead of relying only on past returns, it estimates the premium embedded in current market prices.

This method starts with today’s market level, expected future cash flows, growth assumptions, and the risk free rate. It asks a practical question: what return are investors demanding based on what they’re paying for stocks today?

In a higher rate environment, implied premiums can move quickly because both bond yields and equity valuations change. For 2026 valuation work, many analysts use a mature market MRP range around 4.5% to 5.5%, then test higher and lower cases. A practical base case for developed markets is often near the middle of that range, but it should never be copied blindly.

The Valuation Impact: Why a 1% Shift Matters

A small change in market risk premium can create a large change in valuation. Suppose you’re valuing a software company with a beta of 1.5. If the risk free rate is 4% and MRP is 5%, the cost of equity is:

4% + 1.5 × 5% = 11.5%

If MRP rises to 6%, the cost of equity becomes:

4% + (1.5 × 6%) = 13%

That single point increase in MRP raises the cost of equity by 1.5 % points. In a DCF model, that can reduce the present value of future cash flows dramatically. The impact is especially severe for growth companies whose cash flows arrive far in the future. This is why serious valuation work shouldn’t rely on one static MRP assumption. It should include sensitivity analysis.

Historical vs Implied Risk Premium

The debate between historical vs implied risk premium is really a debate between comfort and relevance. Historical data feels stable because it uses long time periods. But it’s backward looking. Implied data feels more current because it reflects today’s market pricing. But it’s more sensitive to assumptions about growth, margins, and future cash flows.

Neither method is perfect. A strong analyst often uses both. Historical MRP gives a reality check. Implied MRP gives current market context. If the two are far apart, that gap itself is useful information. It may suggest that markets are unusually optimistic, unusually fearful, or pricing in a major macro shift.

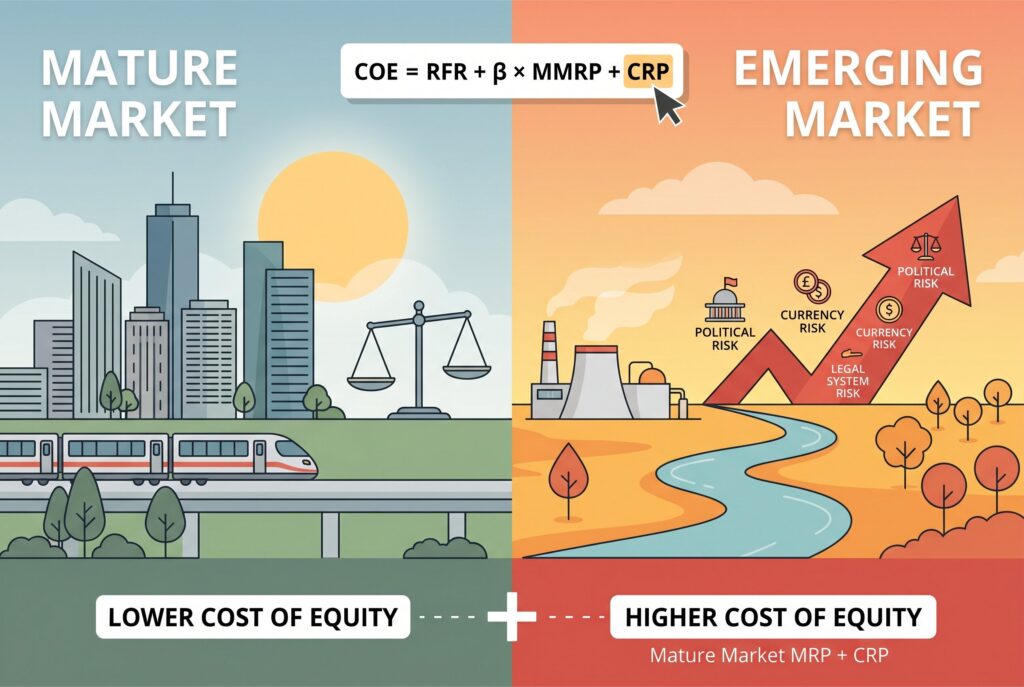

Global Investing: Adding Country Risk Premium

If you’re valuing a company outside a mature developed market, mature market MRP usually isn’t enough. Emerging markets may carry additional political risk, currency risk, liquidity risk, inflation risk, and legal system risk.

That is where the country risk premium becomes important. A global cost of equity formula may look like this:

Cost of Equity = Risk Free Rate + Beta x Mature Market MRP + Country Risk Premium.

For example, a company operating in a politically unstable market should usually have a higher required return than a similar company operating only in the United States. Ignoring this adjustment can overvalue international businesses.

Conclusion

Market risk premium is simple in formula but complex in practice. It’s the extra return investors demand for choosing stocks over safer assets, and it’s one of the most important inputs in CAPM, cost of equity, required return, and valuation.

In 2026, analysts shouldn’t treat MRP as a fixed textbook constant. They should compare historical and implied approaches, check the risk free rate, consider beta, add country risk when needed, and test valuation sensitivity. A thoughtful MRP assumption can make the difference between a disciplined valuation and a dangerously optimistic model.