When investors measure short term liquidity, they often start with the current ratio or quick ratio. But the cash ratio is the strictest test of financial safety. So, what is the cash ratio? It measures whether a company can pay current liabilities using only cash and cash equivalents. It doesn’t count inventory, accounts receivable, prepaid expenses, or other assets that may take time to convert into cash. The cash ratio formula is simple, but the interpretation isn’t. A low score may be normal for a retailer with fast daily cash inflows, while a high score may signal strong financial health or inefficient idle resources.

Deconstructing the Cash Ratio Formula

The cash ratio formula is:

Cash Ratio = Cash and Cash Equivalents Current LiabilitiesThis is one of the cleanest formulas in financial analysis because it uses only two balance sheet items. Cash and cash equivalents include money in bank accounts, cash on hand, money market funds, treasury bills, and highly liquid short term investments that can be converted into cash almost immediately.

Current liabilities include obligations due within 12 months. These may include accounts payable, short term debt, accrued expenses, taxes payable, current lease liabilities, and the current portion of long term debt.

A basic cash ratio calculation might look like this:

A company has $500,000 in cash and cash equivalents.

It has $1,000,000 in current liabilities.

Cash Ratio = $500,000 / $1,000,000.

Cash Ratio = 0.50.

That means the company has 50 cents in immediate cash for every $1 of short term obligations.

Why the Cash Ratio Is So Conservative

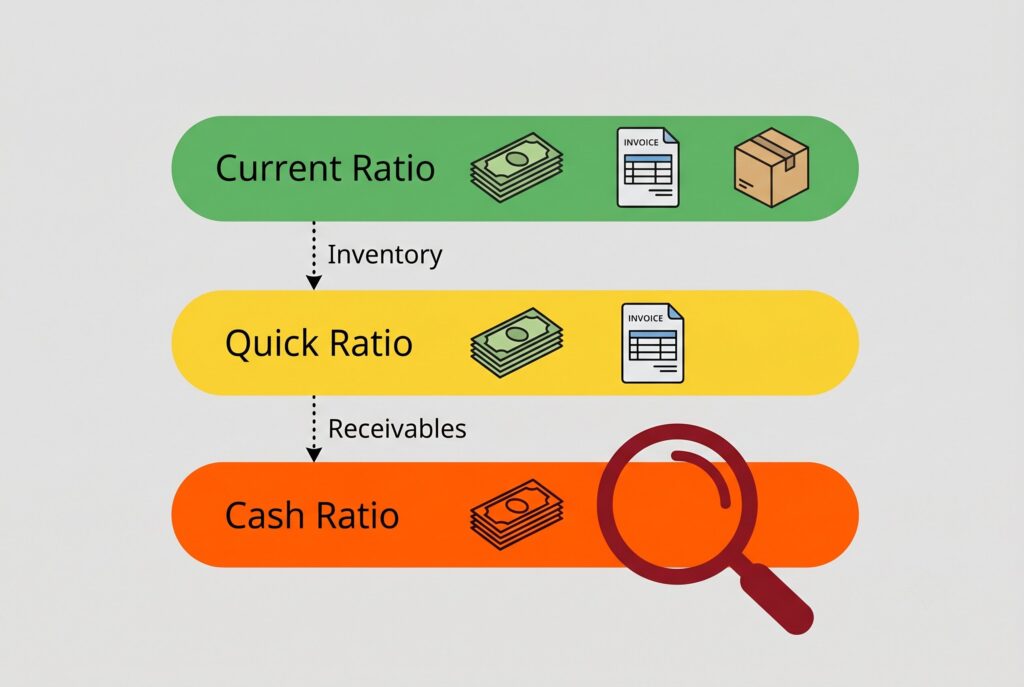

The cash ratio is more conservative than the current ratio and quick ratio.

- The current ratio includes all current assets, including inventory and receivables. That can be misleading because inventory may not sell quickly, and customers may delay payment.

- The quick ratio removes inventory but still includes accounts receivable. That makes it stricter than the current ratio, but it still assumes customers will pay on time.

The cash ratio removes both inventory and receivables. It asks one harsh question: if bills came due today, how much could the company pay using cash already available?

That is why lenders, investors, and CFOs use it as a stress test rather than a complete measure of business strength.

Industry Context: Real Cash Ratio Examples

The Cash Ratio should always be evaluated within the context of an industry. There is no single “good” Cash Ratio that applies to every business.

For example, a large technology company such as Apple may maintain substantial cash reserves to support global operations, strategic investments, and financial flexibility. In contrast, a retailer such as Walmart often operates with a much lower cash balance because cash is collected from customers every day while payments to suppliers may be deferred through trade credit.

As a result, comparing the Cash Ratio of Apple directly with Walmart can lead to misleading conclusions because the two companies operate under fundamentally different business models.

The table below uses real balance sheet data from 2026 filings and applies the same formula to each company:

| Company | Industry | Reporting Period | Cash & Cash Equivalents | Current Liabilities | Cash Ratio |

| Apple (AAPL) | Technology | Mar. 28, 2026 | $45.572B | $134.641B | 0.34 |

| Walmart (WMT) | Retail | Jan. 31, 2026 | $10.727B | $107.469B | 0.10 |

| Caterpillar (CAT) | Manufacturing | Mar. 31, 2026 | $4.072B | $35.902B | 0.11 |

Apple has the highest Cash Ratio in this comparison, reflecting a stronger immediate cash buffer relative to short term obligations. This is common for large technology companies with significant cash reserves and flexible capital structures.

Walmart has a much lower Cash Ratio, but that does not automatically signal weakness. Retailers often operate with lower cash balances because they collect cash from customers quickly and rely heavily on supplier payment terms, inventory turnover, and predictable operating cash flow.

Caterpillar provides a clearer manufacturing example. Its Cash Ratio is close to Walmart’s, but the business model is very different. Manufacturing companies often carry larger inventory, production costs, equipment needs, and receivables, so liquidity pressure can increase if sales slow or customers take longer to pay.

Therefore, the Cash Ratio should never be interpreted in isolation. The key is to evaluate it within the company’s industry, business model, and peer group to reach a meaningful conclusion.

https://stockanalysis.com/stocks/cat/financials/balance-sheet

https://stock.walmart.com/financial-information/balance-sheet

https://stockanalysis.com/stocks/aapl/financials/balance-sheet

What Is a Good Cash Ratio?

There isn’t one universal benchmark.

- A cash ratio below 0.50 can be normal for businesses with predictable cash inflows, strong supplier credit, and fast operating cycles.

- A ratio near 1.00 means the company has enough cash to cover current liabilities without relying on inventory sales or customer collections.

- A ratio above 1.00 means cash exceeds short term obligations. That sounds safe, but it may raise another question: is management holding too much idle cash?

In some situations, a high cash ratio is smart. A company facing recession risk, lawsuit exposure, supply chain disruption, or debt refinancing may need a large liquidity buffer.

In other situations, excessive cash may mean missed opportunities. The company could use that money for dividends, share buybacks, debt reduction, acquisitions, research and development, or expansion.

Diagnosing a Low Cash Ratio

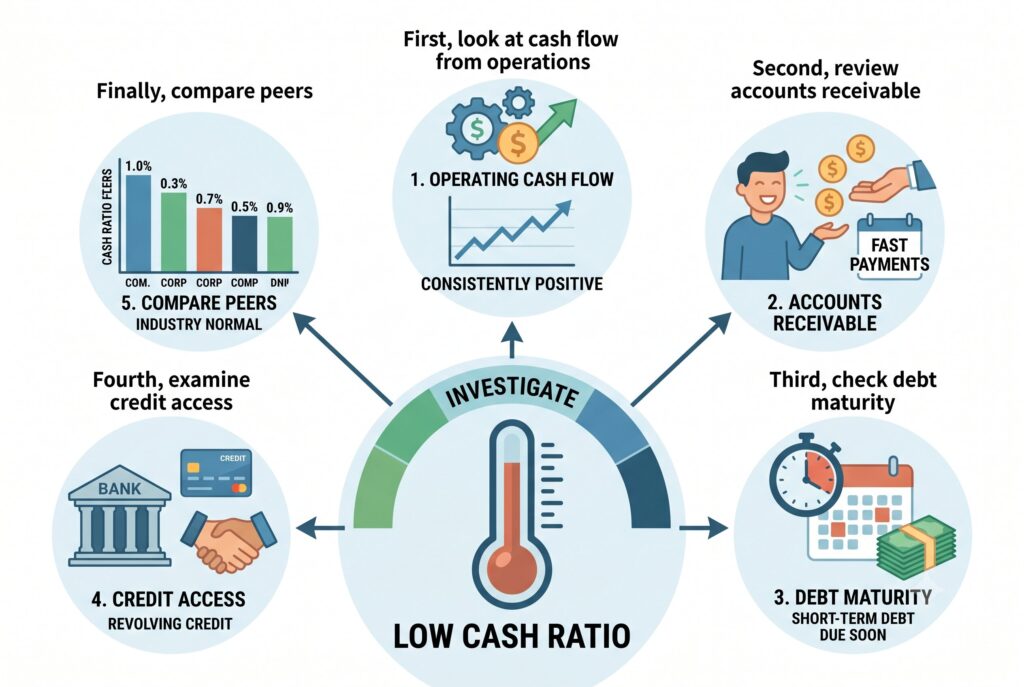

A low cash ratio isn’t automatically bad, but it deserves investigation.

- First, look at cash flow from operations. If the company consistently generates positive operating cash flow, a low cash ratio may be manageable.

- Second, review accounts receivable. If customers pay quickly, the company may not need to keep large cash balances.

- Third, check debt maturity. A company with major short term debt due soon needs more cash than a company with flexible payment schedules.

- Fourth, examine credit access. A strong revolving credit facility can support liquidity, but it’s not the same as cash already on the balance sheet.

- Finally, compare peers. A 0.20 cash ratio may be weak in one industry and normal in another.

Diagnosing a High Cash Ratio

A high cash ratio can be comforting, but it’s not always efficient. Cash usually earns lower returns than productive assets. If a company keeps too much cash idle, shareholders may question whether management is being overly cautious.

A high ratio may also signal that management lacks attractive investment opportunities. In mature industries, this can be a warning that growth is slowing. However, context still matters. Companies in volatile sectors may deliberately hold cash to survive downturns. Startups may hold cash after fundraising to support future development. Cyclical businesses may keep large reserves before a downturn. The key question isn’t simply whether the ratio is high. It’s whether the cash has a strategic purpose.

How CFOs Improve the Cash Ratio

If the ratio is too low, management can improve liquidity in several ways. They can accelerate accounts receivable collection by tightening credit terms, sending invoices faster, offering early payment discounts, or improving collections workflows.

They can reduce excess inventory so cash isn’t trapped in slow moving stock. They can renegotiate supplier payment terms to protect short term cash. They can refinance short term debt into longer maturities. They can reduce unnecessary spending, pause nonessential capital expenditures, or sell unused assets.

But raising the cash ratio shouldn’t become the only goal. A company that hoards cash while starving growth may look safer in the short run and weaker in the long run.

Conclusion

The cash ratio is one of the most conservative liquidity ratios because it measures only immediate cash resources against current liabilities. It strips away optimistic assumptions about collecting receivables or selling inventory.

That makes it useful for stress testing financial health. But the number alone doesn’t tell the full story. A low cash ratio may be acceptable for a retailer with fast cash conversion. A high ratio may be either a sign of strength or a sign of idle resources.

The smartest analysis combines the cash ratio calculation with cash flow trends, working capital management, debt maturity, industry benchmarks, and business model context. Liquidity isn’t only about how much cash a company holds. It’s about whether the company can meet short term obligations without weakening its future.