Planning for retirement can feel overwhelming, especially when everyday expenses compete with long-term goals. But building a strong retirement fund doesn’t require perfect timing or a high income from the start. What matters most is beginning with a practical plan, contributing consistently, and using the right strategies to let your money grow over time. The earlier you start, the more flexibility you usually have. Still, even if you’re starting later, thoughtful decisions can make a meaningful difference.

A solid retirement strategy helps do more than build savings. It can create future retirement income, reduce financial stress, and give you more control over how you want to live later in life.

Why Retirement Planning Matters Earlier Than Most People Think

Many people associate retirement planning with middle age or the years just before leaving work. In reality, retirement saving works best when it begins long before retirement feels close. That’s because time plays a major role in growth. The longer money stays invested, the more opportunity it has to benefit from compound growth.

Starting early also makes the process more manageable. Smaller contributions made consistently over many years may be easier to sustain than trying to save aggressively later. Even modest progress matters when it’s supported by good habits and a long time horizon.

That said, late starters shouldn’t assume they’ve missed their chance. Retirement planning is still worthwhile at any stage. The strategy may need to be more focused, but consistent saving and smart account choices can still improve long-term outcomes.

Understand What a Retirement Fund Is Meant to Do

A retirement fund is more than a savings account for the future. Its purpose is to help replace income once regular work slows down or stops. That means it needs to support spending over many years, not just cover a short transition.

For most households, retirement income will likely come from multiple sources. These may include workplace retirement plans, individual retirement accounts, personal savings, investment accounts, and Social Security. The goal is to build enough financial support so your future lifestyle doesn’t depend on one source alone. Having a large amount of savings alone isn’t enough for retirement. What truly matters is establishing stable income sources, preserving purchasing power, and ensuring your funds last throughout your retirement years.

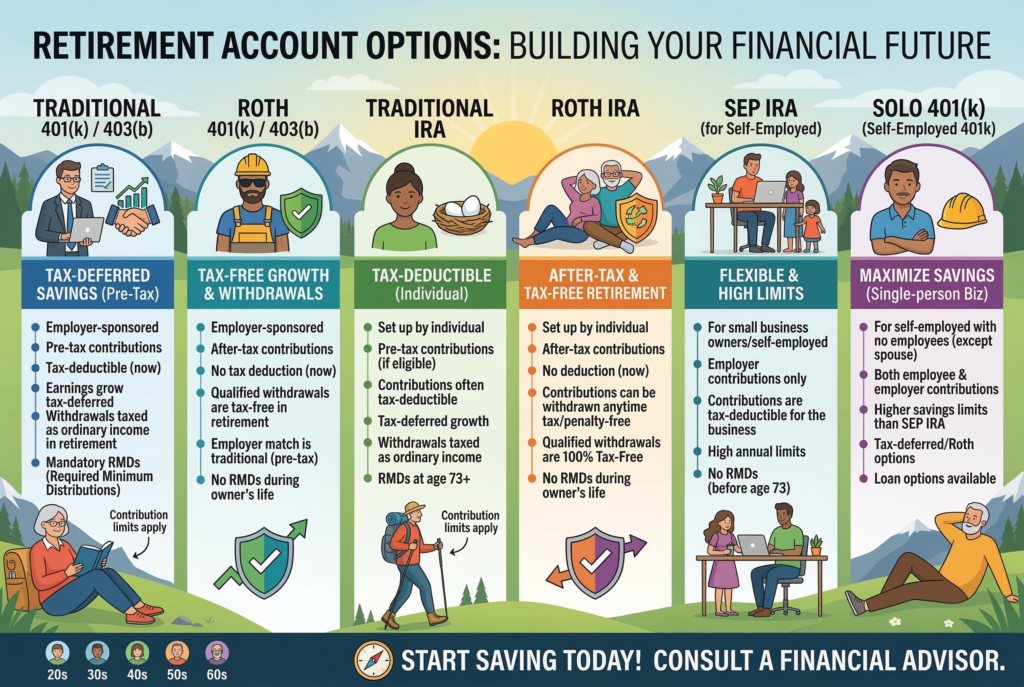

Start With the Retirement Account Options Available to You

One of the smartest first steps is understanding which retirement accounts you can use. In the United States, many workers begin with an employer-sponsored plan such as a 401(k). These plans can make saving easier because contributions are often automatic through payroll deductions.

If your employer offers a match, that’s especially important. Matching contributions are one of the most valuable retirement benefits available because they increase your savings without requiring extra effort beyond your own contribution. If your budget allows it, contributing enough to get the full match is often a strong starting point.

Outside workplace plans, IRAs can also play an important role. Traditional and Roth IRAs each offer different tax advantages. The right choice depends on your current income, tax expectations, and retirement goals. Some people use both a workplace plan and an IRA to diversify their tax treatment and increase total retirement savings.

Build the Habit Before You Focus on the Perfect Amount

A lot of people delay saving because they feel they can’t contribute enough to matter. That mindset can be costly. A smaller, steady contribution is usually better than waiting for the perfect time or the perfect amount. Retirement saving works best when it becomes automatic. Once contributions are built into your monthly system, you’re less likely to skip them or treat retirement as optional. In the long run, that consistency can create far more progress than occasional large deposits made without a long-term pattern. This is where automation helps. Payroll deductions, scheduled transfers, and annual increases can all support better results without requiring constant decision-making.

Use Asset Allocation to Balance Growth and Risk

A retirement fund needs growth, but it also needs a level of risk you can realistically handle. That’s where asset allocation matters. Asset allocation refers to how your portfolio is divided among investments such as stocks, bonds, and cash equivalents.

In general, younger savers often have more time to recover from market downturns, so they may choose a more growth-focused mix. As retirement gets closer, many investors gradually shift toward a more balanced or conservative approach to reduce volatility.

The right allocation depends on your time horizon, risk tolerance, and overall financial picture. A portfolio that is too aggressive may create stress and poor decisions during market declines. A portfolio that is too conservative may not grow enough to support long-term retirement needs. The goal is balance, not extreme positioning.

Increase Contributions Gradually as Income Grows

One of the most effective retirement strategies is increasing contributions over time. Many people start with a manageable percentage of income, then raise it gradually when they receive a raise, bonus, or job change.

This approach works well because it improves savings without always requiring a dramatic lifestyle cut. Even a one percent increase each year can make a noticeable difference over the long run. When income rises, it’s easy for spending to expand automatically. Directing part of each pay increase toward your retirement savings helps turn income growth into lasting financial progress rather than temporary convenience.

Don’t Ignore Fees and Investment Quality

Retirement investing is a long-term process, which means small costs can have a larger impact than they seem at first. Account fees, fund expense ratios, and poor investment options can all reduce long-term growth. That doesn’t mean you need to monitor every detail obsessively. It does mean you should review your retirement accounts periodically. Look at the investment choices, understand whether you’re using diversified funds, and pay attention to whether fees are reasonable.

For many people, broad diversified funds or target-date funds offer a practical way to keep retirement investing simple. The point isn’t complexity. It’s making sure the structure of your account supports long-term compounding rather than quietly working against it.

Plan for Retirement Income, Not Just Retirement Savings

Saving for retirement is only part of the picture. You also need to think about how those savings may turn into retirement income later. This shift matters because a large account balance alone doesn’t guarantee lasting security.

In retirement, withdrawals need to be managed thoughtfully. Spending too aggressively early can increase the risk of running short later, especially if markets perform poorly during the first years of retirement. On the other hand, being too conservative can lead to unnecessary stress and underuse of resources. This is why it helps to think ahead about future income sources, expected expenses, healthcare costs, housing decisions, and how flexible your lifestyle may be. Retirement planning is strongest when it connects the savings phase to the income phase.

Protect Retirement Progress by Managing Debt and Cash Flow

Retirement savings usually grow more effectively when your everyday finances are stable. High-interest debt, inconsistent budgeting, and a lack of emergency savings can all interfere with long-term contributions.

For example, if every financial surprise ends up on a credit card, retirement savings may constantly get pushed aside. Building a basic emergency fund and controlling expensive debt can make retirement contributions much easier to sustain. This is one reason retirement planning should be viewed as part of a broader financial system. Saving for the future becomes more realistic when your present cash flow is manageable and your short-term finances are under control.

Keep Retirement Goals Flexible as Life Changes

A retirement plan shouldn’t be static. Income, family responsibilities, housing costs, health needs, and career paths all change over time. That means your retirement approach should be reviewed and adjusted periodically.

A good review may include checking contribution rates, portfolio allocation, beneficiary designations, and whether your projected retirement lifestyle still matches your current plan. You don’t need to overhaul everything every year. But regular check-ins help you stay aligned with reality instead of relying on assumptions from years ago.

Flexibility also matters emotionally. Some people choose phased retirement, part-time work, or a later retirement age to reduce pressure on savings. Others may downsize housing or relocate to improve long-term affordability. These decisions can affect how much you need to save and how much income your retirement fund must eventually provide.

Understand the Role of Inflation in Long-Term Planning

One of the biggest challenges in retirement planning is inflation. The cost of housing, healthcare, food, and daily living will likely be higher in the future than it is today. That means retirement savings need to do more than grow. They need to maintain purchasing power.

This is why long-term investing matters. Keeping too much retirement money in low-growth vehicles for decades may feel safe in the short run, but it can reduce future buying power. A balanced investment strategy helps address that risk by giving your money a chance to grow faster than inflation over time. Inflation also reinforces the value of reviewing retirement goals regularly. The income you expect to need at retirement may shift as the economy and your lifestyle change.

Avoid the Mistake of Trying to Time the Market

A common retirement mistake is waiting for the perfect investing moment. Some people delay contributions because markets feel too high, while others stop investing during downturns because they feel uncertain.

For long-term retirement planning, consistency is usually more helpful than prediction. Contributing regularly through different market conditions can reduce the pressure of trying to guess the right time to invest. It also helps build discipline, which is one of the most valuable traits in long-term financial planning. Markets will move up and down. A retirement strategy should be designed to keep functioning through those cycles rather than reacting emotionally to each one.

Conclusion

Building a strong retirement fund starts with a simple idea: save consistently, invest thoughtfully, and keep your long-term goals in view. Whether you begin through a 401(k), an IRA, or a combination of both, the habits you build today can shape the quality of your future retirement income. Time, consistency, diversification, and regular review all matter more than chasing perfect conditions.

Retirement planning doesn’t need to be flawless to be effective. It needs to be practical and sustainable. When you start saving early if possible, increase contributions as your finances improve, and connect your savings strategy to future income needs, you create a stronger foundation for long-term financial security and greater peace of mind.