When it comes to financing major purchases or investments, loans are often a key part of the equation. Whether you’re buying a home, funding education, or managing business growth, understanding the different types of loans available is crucial for making an informed decision. With so many loan options out there, it’s easy to feel overwhelmed. However, choosing the right type of loan can make all the difference in achieving your financial goals and managing your debt effectively.

In this article, we’ll take a detailed look at the most common types of loans, explain their benefits and drawbacks, and help you understand which option best suits your needs.

What Are the Different Types of Loans?

Loans come in many forms, each designed to serve specific financial purposes. Understanding each type of loan will give you the clarity you need to choose the best option for your situation. Below are the most common loan types that individuals and businesses typically consider.

Personal Loans

A personal loan is an unsecured loan, meaning you don’t need to provide collateral to secure it. Personal loans are typically used for personal expenses such as medical bills, home improvements, or debt consolidation. Since personal loans are unsecured, they generally come with higher interest rates than secured loans. They’re ideal for individuals who need to borrow a set amount of money quickly, without risking valuable assets like a home or car.

However, keep in mind that the interest rates on personal loans can be significantly higher, especially if you have a low credit score. The repayment term is usually fixed, and the loan must be paid off over a set period, typically from 1 to 5 years.

Home Loans (Mortgages)

A mortgage loan is specifically used to purchase a home, and it is one of the most significant loans most people will ever take out. Mortgages are secured loans, meaning the home you are buying serves as collateral. The amount you can borrow, as well as the interest rate, is typically determined by the value of the home, your credit score, and your ability to repay the loan.

Mortgages can have fixed or adjustable interest rates. A fixed-rate mortgage offers the stability of a consistent interest rate over the life of the loan, making it easier to budget your monthly payments. In contrast, an adjustable-rate mortgage (ARM) typically starts with a lower interest rate that can fluctuate over time, potentially saving you money upfront, but with the risk of higher payments in the future.

Mortgages typically come with long repayment terms, such as 15 years or 30 years, which help lower your monthly payments but mean that you will pay more interest over the life of the loan.

Auto Loans

If you need to finance the purchase of a vehicle, an auto loan may be the best option. These loans are secured loans, with the vehicle serving as collateral. Auto loans usually offer lower interest rates than personal loans because the lender can seize the car if the borrower defaults.

The terms for auto loans vary, but they typically range from 3 to 7 years, with the loan amount, interest rate, and repayment period dependent on the price of the car, your credit score, and the lender’s policies. Keep in mind that although auto loans offer the advantage of lower interest rates, the vehicle’s depreciation means that you may owe more than the car is worth if you’re not careful with your financing options.

Student Loans

For those seeking higher education, student loans are often a necessary part of financing tuition and related costs. There are two main types of student loans: federal loans and private loans.

Federal student loans offer fixed interest rates and income-driven repayment options, making them a better choice for many students. Private loans, offered by banks or credit unions, typically come with higher interest rates and fewer flexible repayment options, but they may be necessary if federal loans don’t cover all of your education costs.

Federal student loans offer the benefit of deferred payments while you’re in school, and repayment often doesn’t start until after graduation. Some federal loans even offer loan forgiveness after a certain number of years, depending on your profession (for example, teaching or public service jobs).

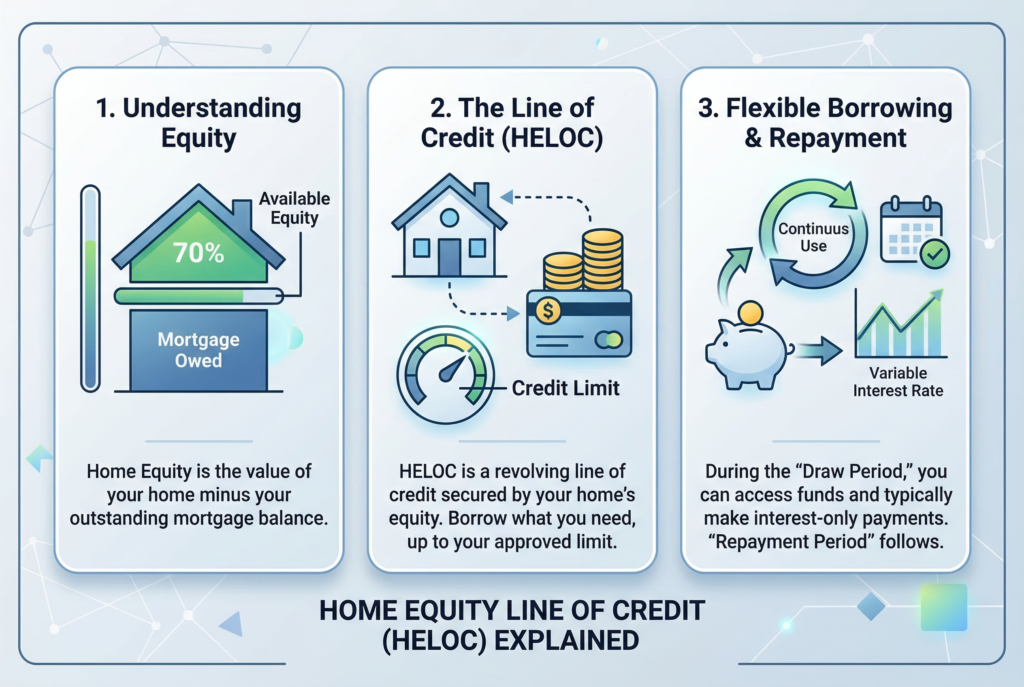

Home Equity Loans

If you own a home and have built up equity, a home equity loan can be a useful option for accessing funds. A home equity loan is a secured loan, where the value of your home serves as collateral. The interest rates for home equity loans are typically lower than those for personal loans, but the downside is that if you default on the loan, you risk losing your home.

Home equity loans are often used for large expenses, such as home renovations or consolidating high-interest debt. They usually come with fixed interest rates and fixed repayment terms, typically ranging from 5 to 15 years. Another popular alternative is a Home Equity Line of Credit (HELOC), which offers a revolving line of credit based on your home’s equity.

Payday Loans

Payday loans are short-term, high-interest loans typically used for emergency expenses. They’re unsecured loans, and you’re required to repay the loan in full, plus interest, by your next payday. Due to the high interest rates and the quick repayment terms, payday loans can be very costly and should be used with caution. They’re often considered a last-resort option due to the high fees and the potential for falling into a cycle of debt.

Payday loans are available without a credit check and can be accessed quickly, but because of the fees and short repayment window, they often end up costing much more than expected.

Debt Consolidation Loans

If you have multiple high-interest debts, a debt consolidation loan can simplify your finances by combining them into one monthly payment. This type of loan is designed to help you pay off existing debts, such as credit card balances, with a new loan that has a lower interest rate. Debt consolidation loans can either be unsecured or secured by collateral, such as your home.

This option can reduce the stress of managing multiple payments and lower your overall interest rate, but be mindful of the terms. Extending the loan term can lower monthly payments but increase the total interest paid over time.

Small Business Loans

Small business loans provide capital for entrepreneurs looking to start or grow their businesses. These loans may be secured or unsecured and come in various forms, including SBA loans, term loans, or lines of credit. The terms for small business loans can vary widely, and the amount you can borrow depends on factors such as your business plan, cash flow, and creditworthiness.

Small business loans are essential for entrepreneurs who need to cover operating expenses, buy equipment, or fund other major investments, but be aware of the lengthy application process and documentation required.

Choosing the Right Loan for Your Needs

Choosing the right loan is about aligning your financial needs with the best loan type. Consider the interest rates, repayment terms, and collateral requirements of each loan. For example, if you need to borrow money for a home, a mortgage will be the right option, while a personal loan might be more appropriate for smaller, unsecured needs.

- If you’re seeking lower monthly payments, a longer loan term may suit you, but if you want to save on interest and pay off the loan quickly, a shorter term may be better.

- If you’re a business owner or entrepreneur, a small business loan or SBA loan could provide the funding you need to grow your business without putting personal assets at risk.

Conclusion: Make an Informed Loan Decision

Understanding the different types of loans available to you can help make your borrowing experience much easier and more affordable. Whether you need a personal loan, a mortgage, or a business loan, choosing the right loan term, interest rate, and repayment plan is key to managing your finances effectively.

By considering your needs, comparing loan options, and understanding the potential risks and benefits of each type of loan, you can confidently make a decision that aligns with your financial goals. With the right loan in place, you can achieve your financial aspirations, whether it’s buying a home, funding your business, or consolidating debt.